- Eid holidays weigh on import scrap market activity

- Opportunistic sentiment keeps container freight elevated

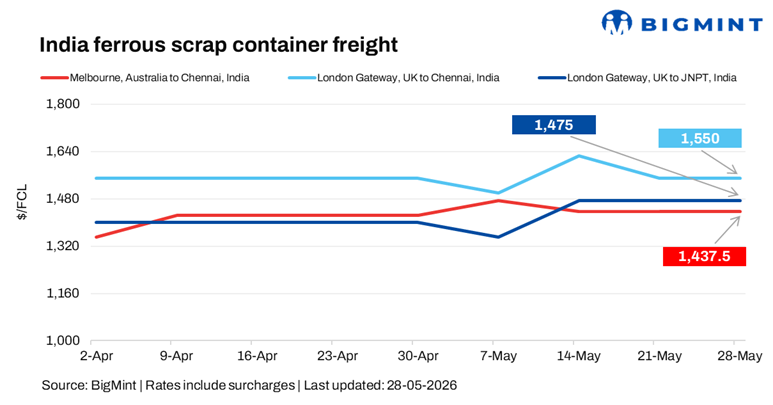

India-bound ferrous scrap container freights remained flat in the week ended 28 May across regions amid subdued trading activity and cautious sentiment. Limited movement persisted due to weak demand, poor import viability, and slower bookings during Eid holidays, while shipping lines maintained rate discipline despite muted cargo flow.

According to market participants, current freight pricing appears to be driven more by favorable market conditions and opportunistic sentiment rather than actual increases in operating costs.

A trader noted, “Container freight rates from Australia and the UK to India remain elevated despite minimal disruptions. The rise is disproportionate to moderate increases in bunker and bulk freight costs, with limited geopolitical impact as vessels largely bunker at Singapore.”

Additionally, concerns were raised over shipping lines increasingly avoiding long-term service contracts and instead capitalizing on spot market conditions. This has added pressure on shippers, particularly those dealing in low-value cargoes such as minerals and agricultural products, who are facing elevated freight costs and reduced pricing stability.

An Australian based shipbroker informed, “Container freight rates are likely to stay stable over the next two weeks amid subdued sentiment and weak trading. Slow activity across key markets due to Eid holidays, along with pressure in Thailand from rising supply and falling rebar prices, continues to weigh on demand.”

Route-wise update

Market highlights

- CFI surge amid ongoing geopolitical uncertainty: The Containerized Freight Index surged by 77 points w-o-w to 2,218 points on 22 May, amid firm market sentiment driven by carrier-led rate push initiatives, selective capacity management, and ongoing geopolitical uncertainty impacting global shipping routes. Additional support came from vessel rerouting, and tighter effective capacity due to blank sailings and operational disruptions across key trade lanes.

- Bunker prices ease amid softer fuel trends: Bunker prices decreased w-o-w by $63/tonne (t) to $766/t on 28 May, reflecting softer fuel market sentiment amid easing crude oil prices and relatively subdued global shipping demand.

- Imported scrap trade remains subdued amid Eid slowdown: The imported scrap market remained subdued amid Eid holidays, weak steel demand, and limited bookings across South Asia, while Turkiye’s deep-sea scrap trade stayed largely inactive ahead of market reopening after 1 June.

Outlook

In the near term, ferrous scrap vessel freight rates to India are expected to remain largely stable with a slight softening bias in the near term, as subdued scrap demand and cautious buying limit fresh fixtures. Ample vessel availability and the lingering impact of the Eid al-Adha slowdown continue to weigh on activity, while easing bunker prices offer limited support and are unlikely to drive any upside.

Leave a Reply