- EGA’s largest smelter hit; output and logistics under pressure

- LME likely to remain volatile amid rising supply concerns

The global aluminium market faces renewed uncertainty after Emirates Global Aluminium confirmed significant damage at its Al Taweelah production complex following missile and drone strikes linked to Iran.

The facility, located in Abu Dhabi, is EGA’s largest aluminium production site and includes both a smelter and an alumina refinery. The company reported that several employees were injured in the attack at the Khalifa Economic Zone, though none of the injuries are life-threatening.

EGA has initiated an assessment of the damage, with management stating that ensuring employee safety remains the top priority.

Operational impact and capacity at risk

The Al Taweelah smelter produced around 1.6 million tonnes (mnt) of cast metal in 2025, while the adjacent alumina refinery produced about 2.4 mnt of alumina, a key raw material for aluminium production.

Any disruption at this integrated complex could affect both upstream and downstream supply chains. EGA also operates another smelter at Jebel Ali in Dubai. The company indicated that it has material already in transit and stocks at overseas locations, which may help cushion immediate supply disruptions.

To manage logistics challenges, EGA has reportedly begun rerouting aluminium exports and raw material imports through the port of Sohar.

GCC supply role under pressure

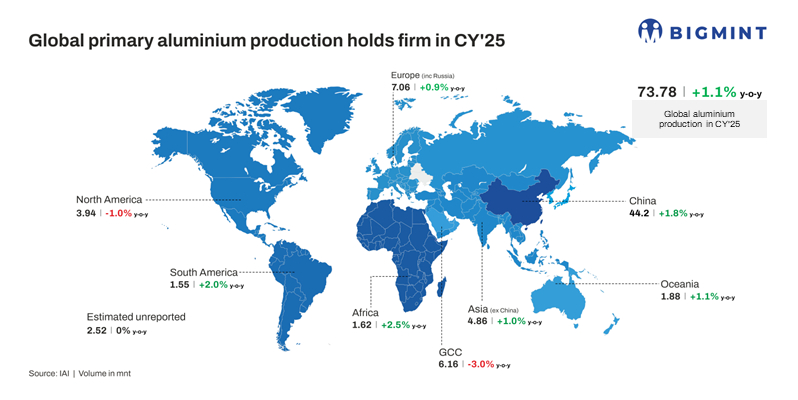

The Gulf Cooperation Council (GCC) accounts for around 8% of global primary aluminium output, underscoring its critical role in global supply.

Global primary aluminium production stood at 73.78 mnt in 2025, largely stable y-o-y, while GCC output declined by 3% y-o-y to 6.16 mnt.

Notably, the global seaborne primary aluminium market is estimated to range between 20-25 mnt, with 1.6-1.8 mnt, or about 8%, contributed by EGA, underscoring its significant role in international aluminium trade.

The latest disruption comes at a time when other major regional producers, including Aluminium Bahrain (Alba) and Qatalum, have already reduced output. Reports of force majeure in parts of the GCC, driven by ongoing geopolitical tensions, have further tightened supply conditions and added uncertainty to the market.

Logistics constraints add pressure

Supply concerns are further increased by disruptions in the Strait of Hormuz, a key route for global energy and commodity trade. Movement restrictions in this region have affected both raw material supplies and finished metal shipments, leading to delays and higher freight costs.

Price trend and market outlook

Aluminium prices on the London Metal Exchange (LME) remained volatile through March. Prices briefly crossed $3,500/t during 13-15 March 2026 before correcting to around $3,240-3,280/t towards the month-end.

The damage at EGA’s Al Taweelah facility–one of the largest smelters in the region–has added uncertainty to the market and is likely to keep prices supported. Ongoing geopolitical tensions in the Middle East continue to influence sentiment and trade flows.

If disruptions at EGA persist or regional tensions escalate, prices may move higher. At the same time, reduced output across the GCC could tighten supply and support physical premiums. Any further disruption in the Strait of Hormuz remains a key risk, with the potential to impact global trade flows.

Overall, aluminium prices are expected to stay volatile, with a firm undertone driven by supply-side concerns.

Leave a Reply