- Scrap demand weak, post-Eid activity remains slow

- Billet supply tightens amid logistics disruptions

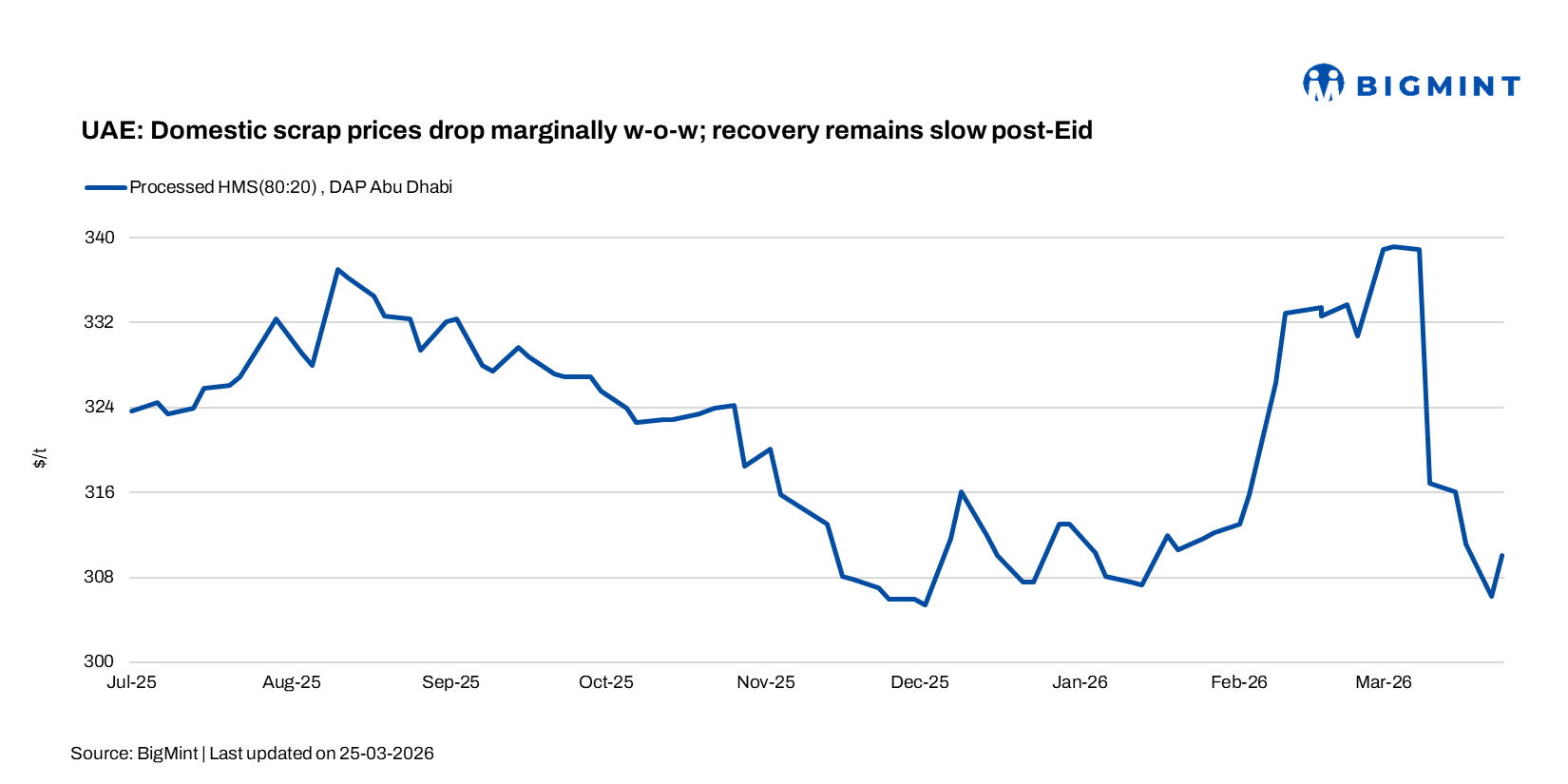

The UAE scrap market remained largely quiet post-Eid, with limited fresh activity. An Abu Dhabi-based mill source said, “We are currently completing old bookings, with bids around AED 1,120/t ($305/t) for sheared HMS and AED 1,200/t ($327/t) for shredded (DAP Abu Dhabi), but no new price indications are available in the market yet.”

The domestic scrap index declined by AED 4/t ($1/t) w-o-w to AED 1,139/t ($310/t) on 25 March, with reduced mill procurement and weak spot activity post-Eid holidays.

An Abu Dhabi-based trader echoed a similar sentiment, noting that “most participants are still receiving previously booked cargoes, while the market remains in wait-and-watch mode for fresh bookings.”

Indicative levels were heard at around AED 1,140/t ($311/t) for processed HMS and AED 1,210/t ($330/t) for shredded (DAP Abu Dhabi), he added.

Meanwhile, a Karachi-based buyer reported receiving an export offer for UAE-origin HMS (400 t) at $445/t CFR Qasim, with shipment already loaded and ETA around the last week of March. The source added that elevated prices are partly driven by upto $2,000/container freight amid war-related risks, increasing overall landed costs.

UAE billet supply is tightening as re-rollers rely on existing inventories while fresh inflows remain limited due to ongoing shipping disruptions. Most mills are currently consuming stocks, with inventories expected to deplete by mid-April. Alternative routes via Oman are being explored, but longer transit times and additional costs of around $30/t are limiting feasibility.

Market participants indicated that mills may consider maintenance shutdowns if supply does not improve. Tight availability is expected to support billet and rebar prices in the short term.

UAE authorities have urged market participants to avoid unjustified price hikes in key construction materials, including steel and cement, in a bid to stabilise the market amid rising costs and supply disruptions. However, industry participants expect limited impact, with private mills likely to continue adjusting prices in line with higher raw material and logistics costs. While government-linked producers may hold prices steady, others are expected to push for increases, citing tight supply and elevated input costs. Market direction remains uncertain, with mills delaying price announcements, though upward pressure is likely to persist in the near term.

Outlook

Scrap demand in the UAE is expected to remain subdued as mills continue to rely on existing inventories post-Eid. However, ongoing Middle East tensions are likely to keep freight and bunker costs elevated, supporting higher import offers and limiting downside.

At the same time, disruptions to regional trade flows and restricted billet inflows may tighten supply further, prompting mills to manage production or consider maintenance. While regulatory efforts may cap aggressive price hikes, underlying cost pressures are expected to keep steel prices firm, with clearer direction emerging as logistics conditions stabilise.

Leave a Reply