- Traders fulfil earlier bookings amid lack of inquiries

- Expectations of drop in steel prices cap scrap demand

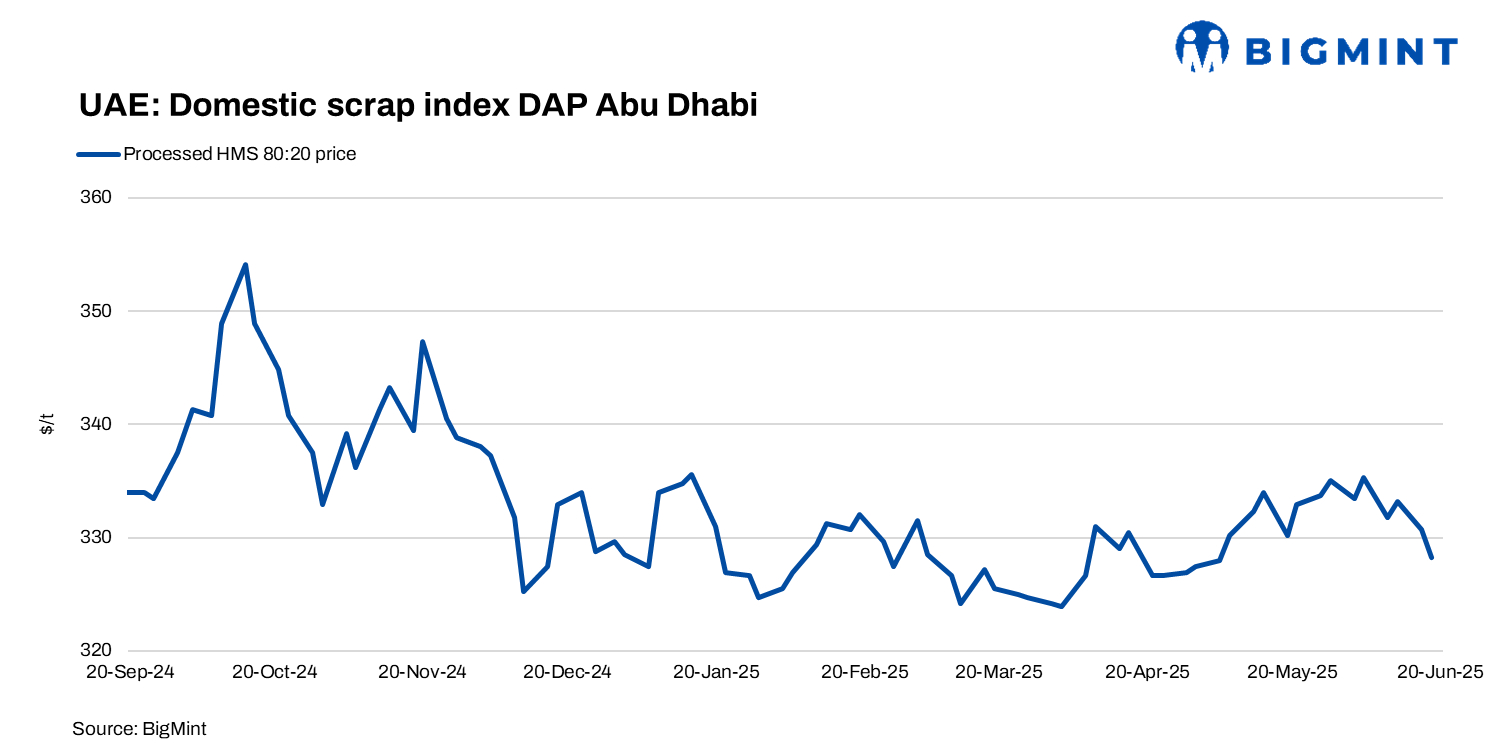

BigMint’s UAE domestic processed HMS index dropped by AED 18/tonne (t) ($5/t) w-o-w to AED 1,206/t ($328/t) amid nearby geopolitical unrest, followed by dull inquiries by mills.

HMS 80:20 remained steady at AED 1,150-1,160/t ($313-316/t), while fabrication stood at AED 1,240-1,250/t ($338-340/t). Rebar end-cuts traded between AED 1,280-1,300/t ($348-354/t), LMS was heard at AED 850-855/t ($231-233/t), and processed HMS was at AED 1,200-1,210/t ($327-330/t) DAP Abu Dhabi. Shredded saw limited interest, with offers at AED 1,255-1,265/t ($342-344/t) DAP Abu Dhabi.

A Dubai-based scrap supplier noted, “Mills are clearly trying to push prices down, citing regional tensions.” As they expect the local steel prices to decline in the near term, they have been calling for price cuts for raw materials.

“We are currently fulfilling earlier bookings and have not received any fresh inquiries from mills,” a major trading house source stated.

Export market

UAE-origin shredded was heard at $375-380/t CFR Qasim, with offers rising to above $385/t in the last couple of days. HMS-PNS mix (UAE origin) was offered at $365-370/t CFR Qasim, with expectations earlier at around $362-366/t. Around 1,000 t of UAE-origin HMS and PNS mix was recently sold at $360-365/t CFR Chattogram, whereas 250 t of Yemen-origin HMS and bundles were offered at $335/t CFR west coast India.

HMS (80:20) spread

The average spread between HMS 80:20 from Europe and the UAE’s processed HMS 80:20 widened w-o-w to approximately $10-12/t CFR Nhava Sheva. Prices of imported HMS on the west coast of India stood at $340-342/t CFR, while the UAE’s processed HMS tags were at $325-328/t DAP Abu Dhabi.

UAE HDG prices hold firm

Hot-dip galvanised (HDG) coil prices in the UAE remained steady w-o-w, with domestic offers for 1 mm Z275 coils for July-August shipment ranging within $700-800/t, either on a delivered or exw basis, depending on the supplier.

While local producers maintained stable prices to secure consistent order flow, global mills showed caution. Indian suppliers kept offers high and deprioritised GCC markets, whereas Chinese mills remained competitive and active.

Market participants remained cautious amid geopolitical tensions, supply route risks, and fluctuating raw material costs. The near-term HDG price trend will largely depend on shifts in international supply and the UAE’s downstream demand.

Outlook

The UAE’s scrap market may stay soft as mills delay bookings and push for lower prices amid Middle East tensions. Export offers remain firm, but trade is limited. Finished steel prices are stable, yet market sentiment stays cautious due to global uncertainties and muted demand.

Leave a Reply