- Weak industrial demand leads to need-based buying

- Indonesian HBA index shows mixed trends for mid-Jun

Indonesian thermal coal prices continued their downward trajectory across Indian ports this week, weighed down by weak industrial demand, improved domestic coal availability, and increased vessel arrivals. The slowdown in sectors such as steel, textiles, cement, and chemicals curbed active buying, with most procurement limited to need-based or speculative purchases. Indonesian indexed prices also faced pressure.

For the power sector, domestic coal remained the primary source, reducing the urgency for imports. With freights fluctuating and sentiment weak, traders were hesitant, further contributing to price stagnation.

Sharp declines recorded across major grades

According to BigMint’s assessment on 20 June 2025, Indonesian coal prices recorded notable w-o-w drops across major Indian ports. The widely traded 5000 GAR grade fell by INR 250/tonne (t) to INR 7,450/t at Kandla and INR 7,350/t at Vizag. Similarly, the 4200 GAR grade dropped by INR 250/t to INR 5,800/t at Kandla and INR 5,700/t at Vizag. The lower 3400 GAR grade slipped by INR 200/t to INR 4,300/t at Navlakhi Port.

These price reductions of INR 200-250/t reflect softening global benchmarks and tepid domestic buying, both of which led to consistent downward pressure on market valuations.

Portside thermal coal inventories rise

Thermal coal stockpiles at Indian ports increased by 4.3% in week 24 of CY’25 to 16 million tonnes (mnt) from 15.35 mnt in the previous week. This growth was driven by higher vessel arrivals, notably at Goa Port, where key players such as Adani Enterprises and JSW Steel unloaded cargoes.

Coal inventories at power plants edge up

At the same time, coal inventories at power plants also edged up. As of 19 June, total coal stocks stood at 61.38 mnt, up from 60.96 mnt the previous week. These levels are sufficient to support approximately 21 days of power generation under standard operations. However, stock distribution remained uneven, with several plants, particularly those relying solely on domestic or imported coal, reporting critically low reserves and logistical bottlenecks.

Global benchmarks under pressure as demand falters

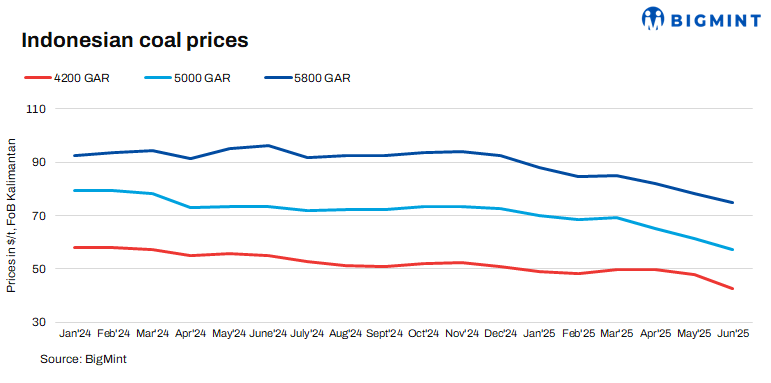

Internationally, Indonesian benchmark prices continued to decline this week due to oversupply concerns and fading demand from major importers such as China and India. The 5800 GAR grade dropped by $1.21/t w-o-w to $72.98/t, while 4200 GAR fell by $1.36/t to $40.64/t. The 3400 GAR dipped $1.21/t w-o-w to $30.22/t.

Further reinforcing the bearish sentiment, Indonesia has adjusted its benchmark prices for the second half of June 2025. The high-CV (6,322 GAR) grade dropped $2.36/t to $98.61/t, the lowest level since March. The mid-CV (5,300 GAR) grade also fell sharply by $1.95/t w-o-w to $75.64/t. Interestingly, low-CV grades posted marginal gains:

- HBA-II (4,100 GAR) rose $0.17/t w-o-w to $50.25/t.

- HBA-III (3,400 GAR) increased $0.67/t w-o-w to $36.14/t.

These gains reflected steady demand from budget-conscious domestic and regional utilities, signalling a shift towards cost-effective, lower-grade coal options.

Outlook: Bearish momentum expected to continue

Market participants do not foresee a near-term rebound. Chinese demand remains negligible as domestic coal production rises, and oversupply continues to cloud the international market. Freight volatility and weak fundamentals are expected to keep Indonesian coal prices under pressure at Indian ports well into the coming weeks.

Leave a Reply