- Seasonal supply tightening offers price support

- Turkish domestic scrap prices rise 6-8% in last 2 months

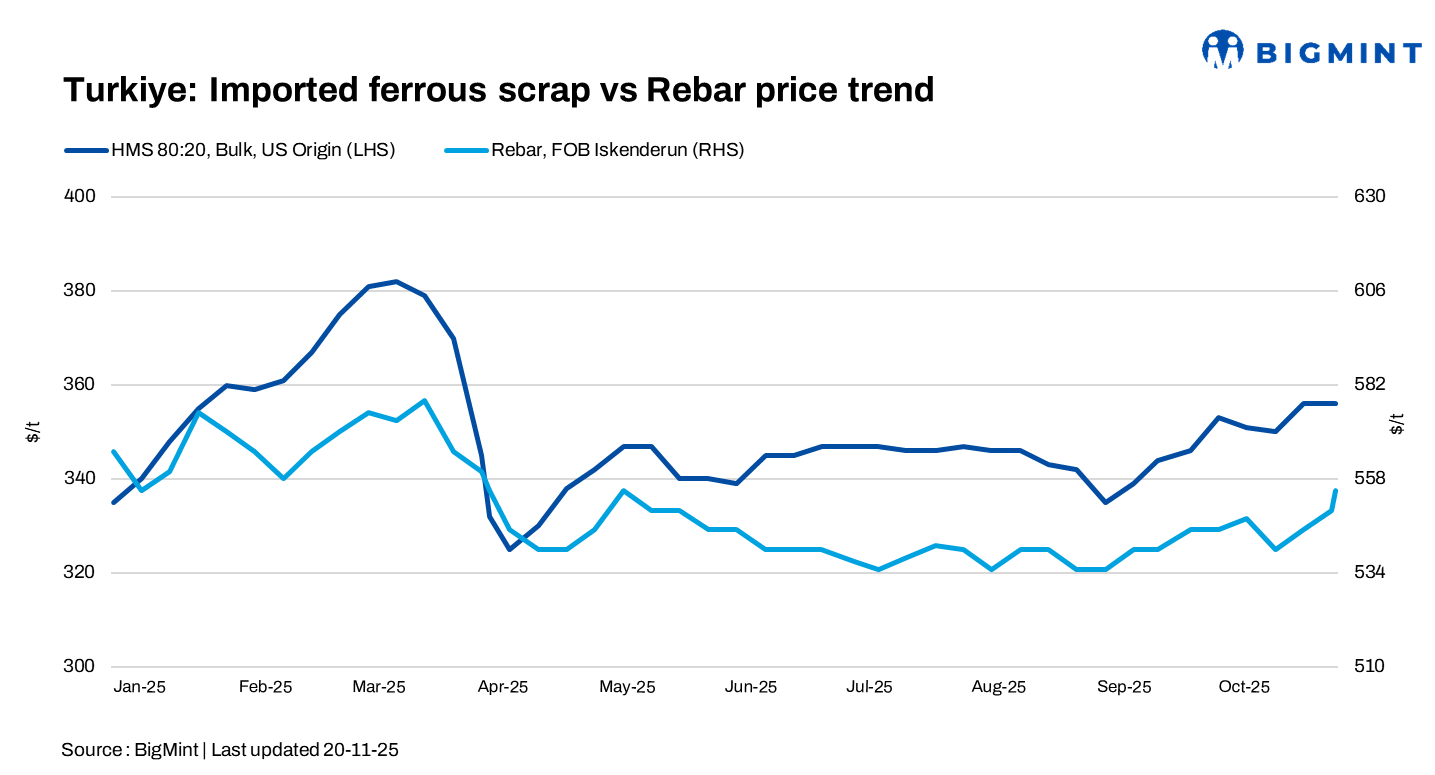

Imported deep-sea scrap prices in Turkiye held stable w-o-w, with rising rebar prices reinforcing expectations of a possible near-term uptick in values. Seasonal tightening in supply could add further upward pressure, while firm US collection costs and bullish freight rates continue to support current offer levels.

Around four to five imported scrap deals were concluded in the past seven days.

Price assessments

- US-origin bulk HMS 80:20 was assessed at $356/t CFR Turkiye, stable w-o-w.

- Bulk HMS 80:20 from the US East Coast stood at $323/t FOB, down by $2/t w-o-w.

The scrap-to-rebar spread stayed around $200-205/t, with rebar offers at $555-560/t FOB.

Market scenario

A market participant said he expected a slightly quieter market, with Turkish mills expected to delay fresh bookings until later in the month as they prepare to secure cargoes for January shipments.

Elsewhere, participants kept a close eye on rising billet prices in Asia, which some Turkish mills viewed as unworkable. Scrap was seen holding a relative advantage, as Chinese billet prices continued to trend higher.

A market participant said US-origin HMS in bulk continued to be transacted at around $355-356/t CFR, while offers remained above $360/t from US suppliers and European prices stayed firm, with bids for high-grade EU-origin scrap at $354/t CFR and offers around $355/t CFR.

Domestic market update

As per market insiders, Turkiye’s domestic scrap prices continued to rise amid lower import volumes, climbing nearly 6-8% in last two months.

Major steel mills continued raising scrap procurement prices, with Kardemir pushing DKP scrap to TRY 15,400/t ($363/t) after four increases since late September, while Erdemir lifted its DKP purchase price to TRY 15,055/t ($355/t).

Mills have been steadily lifting rebar prices on the back of stronger-than-usual year-end sales, helping maintain positive sentiment in the scrap market.

Outlook

Market participants noted that the surge in construction and infrastructure investments has impacted iron and steel production and that the increased demand for domestic scrap has also driven up prices. Market sentiment remains cautiously optimistic, with firm rebar demand and supported collection costs expected to underpin scrap values in the near term.

Leave a Reply