- Active export deals heard in seaborne market

- China demand soft on high port stocks, weak steel margins

Indian iron ore export prices remained largely firm this week, with active trade sentiment reported in the seaborne markets. Market participants reported that some export deals were concluded for December laycan cargoes, with buyers responding positively to slightly lower price levels. Despite muted sentiments in the global steel market, exporters noted an uptick in trade volumes, although prices continued to hover in the same range.

Prices, deals

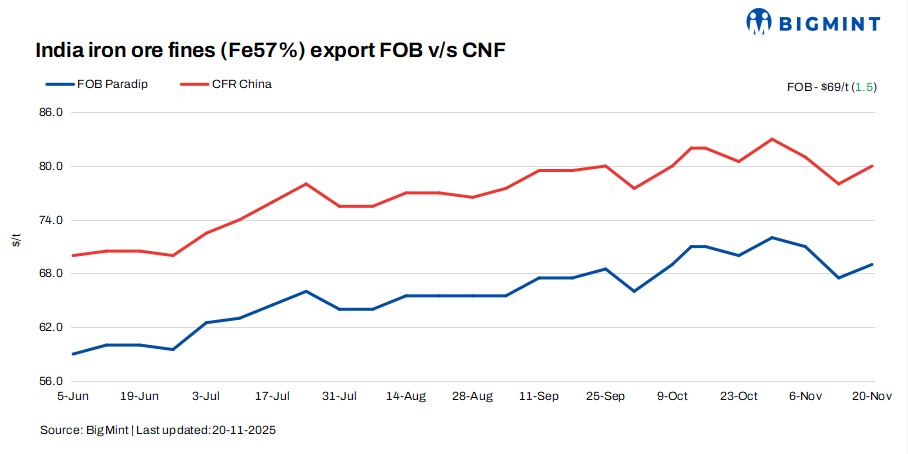

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices rose by $1.5/tonne (t) w-o-w to $69/t FOB east coast on 20 November. Meanwhile, the index stood at $80/t CFR China.

Bigmint reported approximately 500,000 t of export deals during this publishing period, primarily for December laycan. Most of these deals were recorded from the eastern part of the country, with only a few transactions reported from the southwest coast.

Currently, miners are actively offering iron ore in the export market; however, the prices they are offering have not aligned with buyers’ bids. As a result, some negotiations are still ongoing.

Market scenario

A major exporter said, “We are seeing some pickup in inquiries, but buyers are still hesitant to commit at higher levels. Most deals happen only when sellers agree to negotiate slightly. Some panic selling was also seen in the market.”

Multiple trading sources confirmed that major exporters are actively selling their cargoes amid expectations of a widening discount for January shipments. Low-grade iron ore discounts also remained steady in the 15-17% range, with several cargoes reportedly offered in the market.

Another market participant noted, “The discount hasn’t moved much, but sellers are more open to discussions now considering the uncertain outlook for early next year.”

Some exporters, however, are choosing to hold material in anticipation of improved bids. “We are waiting for a clearer trend from China. If port stocks ease or steel margins improve, bids may strengthen,” an international trader noted.

On the demand front, China’s appetite for Indian fines continues to remain subdued due to higher port inventories and compressed steel mill margins. This has kept the overall sentiment cautious.

Meanwhile, results from the recent OMC auction indicated aggressive bidding for fines, which is likely to push sourcing costs higher for exporters. The rise in input costs could further squeeze margins unless export realisations improve.

Chinese spot prices soften w-o-w: The benchmark iron ore fines index remained stable w-o-w at $105/t CFR China on 19 November. Prices eased midweek as downstream fundamentals remained weak. Medium-grade differentials narrowed on ample supply and limited spot buying, while demand for high-grade fines was muted amid weak mill margins. Portstock prices were range-bound on moderate liquidity, and with mills buying only as needed, a near-term rebound appears unlikely.

DCE iron ore futures drop: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Jan 2026 contract closed at RMB 788.5/t ($112/t) on 20 November, surged RMB 16/t ($2/t) w-o-w.

Rationale

- Four (4) major deals for Fe 57% were recorded during this publishing window, which were taken for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received fourteen (14) indicative prices in the current publishing window, and nine (9) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventories at major Chinese ports were recorded at 139.62 mnt on 20 November, remaining stable w-o-w, as per data published by SteelHome.

Outlook

Indian fines export prices to stay volatile in the coming days, with more negotiable deals likely as sellers adjust to shifting demand dynamics.

Leave a Reply