- Deep-sea bulk arrivals down 15% on selective sourcing

- Supplies ample, mills conservative about restocking

Turkiye’s ferrous scrap imports softened in July-September 2025 (Q3CY’25) on muted steel demand and cautious procurement, with both quarterly and annual comparisons showing a contraction in volumes.

Import trends

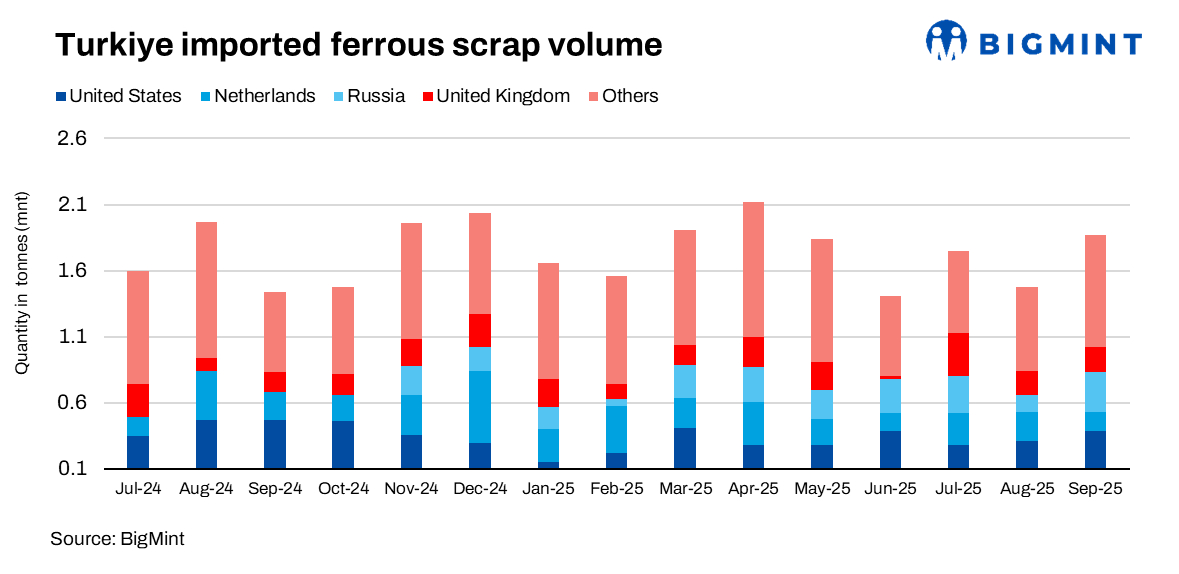

Turkiye imported 4.58 million tonnes (mnt) of ferrous scrap in Q3, registering a 2% decline q-o-q from 4.67 mnt in Q2. On a y-o-y basis, imports dropped 8% against 4.94 mnt in Q3CY’24.

The weakness was more pronounced in deep-sea bulk arrivals, which slipped 15% q-o-q to 3.51 mnt from 4.12 mnt in Q2CY’25, and fell 7% y-o-y from 3.79 mnt in Q3CY’24.

BigMint’s vessel-tracker data shows 55-60 deep-sea bulk vessels scheduled to berth over the quarter, indicating restrained buying and conservative restocking strategies.

Quarterly price average

- US-origin HMS 80:20 CFR Turkiye averaged $344/t in Q3CY’25, down 1% from $346/t in Q2CY’25.

- HMS 80:20 FOB East Coast US averaged $315/t in Q3CY’25, down 3% from $324/t in Q2CY’25.

- Rotterdam HMS 80:20 bulk FOB Europe averaged $314/t in Q3CY’25, down 2% from $322/t in Q2CY’25.

Country-wise imports

The US remained the largest supplier in Q3CY’25, accounting for 21% of Turkiye total scrap imports despite overall decline in the import volumes.

- US: Imports inched up by 3% q-o-q to 0.98 mnt in Q3 compared to 0.95

- UK: Imports rose 49% to 0.7 compared to 0.5 mnt in Q2.

- Netherlands: Imports slightly declined by 9% to 0.6, down from 0.7 mnt q-o-q.

Scrap demand remained range-bound in Q3, with mills exercising selective buying on weak finished steel sales and subdued domestic activity. August bookings fell short of expectations, and buyers stayed on the sidelines, citing slow rebar and wire rod sales. Supply overhang from ample European cargoes and muted import interest kept prices under pressure, while seasonal restocking and export prospects provided only limited support.

Key updates

- Turkiye’s crude steel production rose to 9.76 mt in Q3, up 8% from 9.04 mt in Q2.

- The Turkish lira weakened 5%, averaging TRY 41 in Q3 versus TRY 39 in Q2.

- Billet imports jumped 36% to 2.13 mnt in Q3 from 1.57 mnt in Q2.

- HRC imports increased 1% to 1.2 mnt in Q3 from 1.19 mnt in Q2

- Rebar imports dropped 24% to 0.13 mnt in Q3 from 0.17 mnt in Q2.

Outlook

Steady billet interest and seasonal restocking could support limited price improvement, helping prevent deeper declines, while suppliers are expected to resist sharp cuts. Overall sentiment suggests a firm but controlled upside, with some additional bookings expected for late November, even though many suppliers may find little room to raise their collection costs.

Leave a Reply