- US, European suppliers continue to dominate Turkish scrap imports

- Rise in billet imports limit aggressive scrap bookings

- Rising freight, energy costs pressure Turkish mill margins

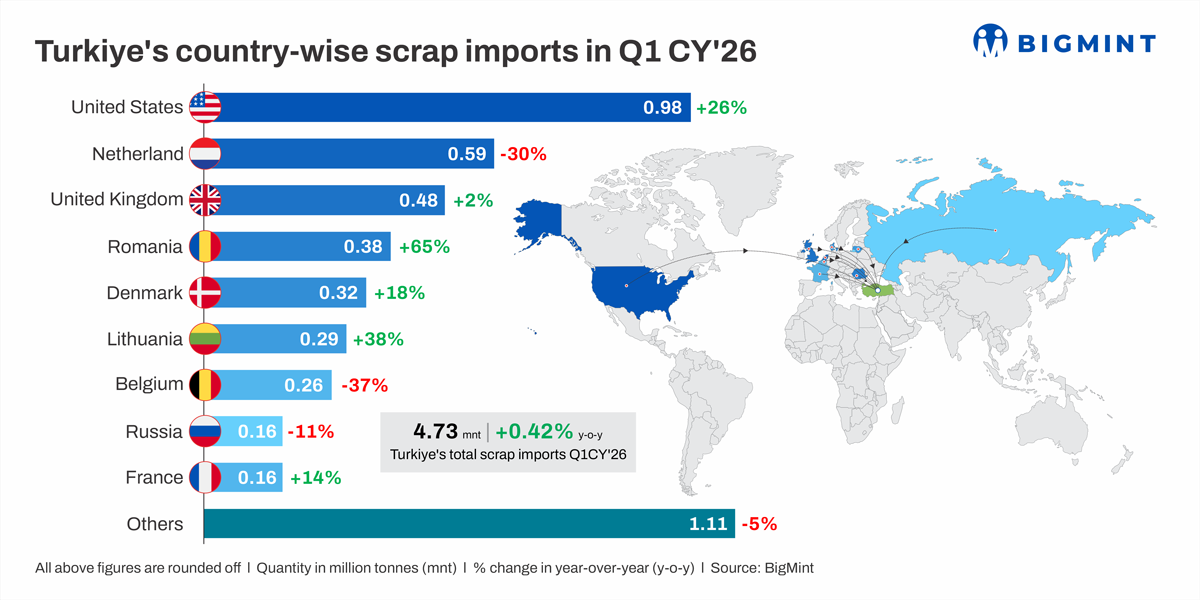

Morning Brief: Turkiye’s ferrous scrap imports remained broadly stable during Q1 CY2026 despite weaker March arrivals, elevated freight costs, compressed steel margins, and continued geopolitical uncertainty. According to BigMint analysis, Turkiye imported around 4.73 mnt of ferrous scrap during January-March 2026, up marginally by 0.4% y-o-y from 4.71 mnt in the corresponding period last year.

However, imports declined slightly by 1% to 4.73 mnt q-o-q from Q4 CY2025 levels (4.77 mnt), reflecting cautious procurement activity among mills amid tight liquidity conditions and elevated financing costs.

March imports alone declined to around 1.62 mnt due to slower booking activity during Ramadan and uncertainty surrounding export demand amid escalating Middle East tensions. Market participants noted that Turkish mills remained cautious in raw material procurement as volatile steel demand and restrictive monetary policies continued limiting working capital flexibility.

Higher freight keeps scrap prices elevated

Imported ferrous scrap prices remained elevated during Q1 CY’26. HMS 80:20 prices into Turkiye averaged around $378/t CFR, up 6% y-o-y. Meanwhile, US-origin HMS 80:20 prices increased by 4% y-o-y to $349/t CFR, while Rotterdam-origin HMS 80:20 prices rose by 4% to $345/t CFR.

Additionally, US-origin shredded scrap FOB prices averaged $369/t in Q1 CY’26 compared with $356/t in Q1 CY’25, reflecting an increase of around 4% y-o-y.

The ongoing Middle East conflict, particularly disruptions linked to the Strait of Hormuz, sharply increased bunker fuel prices, freight rates, and war-risk insurance premiums during the quarter. Freight rates from the US East Coast and Baltic region to Turkiye were heard around $50-60/t, while Rotterdam-Aliaga freight rates remained elevated at around $25-35/t. High energy prices and narrowing steel margins continued to limit aggressive scrap buying by the Turkish electric-arc furnace (EAF) mills.

US strengthens position in Turkish market

The USA significantly expanded its presence in Turkiye’s scrap market during Q1, with the US emerging as the country’s single-largest scrap supplier. US-origin scrap imports surged by 26% y-o-y to nearly 1 mnt during the quarter, supported by relatively competitive cargo availability and weaker buying activity from traditional Asian consumers such as Bangladesh.

Market participants noted that US-origin cargoes remained one of the most reliable deep-sea supply sources despite elevated freight costs. However, Turkish mills turned increasingly cautious during March as weak finished steel demand and sufficient earlier bookings reduced fresh cargo requirement.

Europe remains dominant supplier

Europe remained Turkiye’s largest scrap sourcing region during Q1, supplying around 2.5-3 mnt of total imports (nearly 60%). However, shipments from several European suppliers declined y-o-y due to winter-related collection disruptions, weaker dock inflows, tight scrap availability, and higher logistics costs. A stronger euro against the US dollar also raised the landed cost of European-origin cargoes for Turkish buyers.

Within Europe, Romania-origin scrap imports rose sharply by 65% y-o-y to around 0.38 mnt, while Denmark-origin shipments increased by 18%, supported by diversified sourcing strategies among Turkish mills. In contrast, imports from the UK, Netherlands, and Belgium declined significantly due to lower export availability and cautious booking activity.

Steel production rises

Turkish crude steel production increased by 5.3% y-o-y to around 9.74 mnt in Q1 CY’26, supported by stronger domestic demand and improved flat steel production. In March alone, output rose by 6% y-o-y to 3.3 mnt. However, production declined q-o-q from 10.05 mnt recorded in Q4 CY’25, which kept the imported scrap demand equation largely balanced compared to the previous quarter.

Domestic scrap generation also remained stable during the quarter, increasing marginally by 0.3% y-o-y to 2.91 mnt, while total scrap consumption rose by 0.39% to 7.64 mnt. The marginal increase in both domestic generation and scrap consumption supported steady raw material procurement by Turkish mills despite cautious market conditions.

Billet competition pressures scrap demand

Despite improving steel output, Turkish mills remained cautious in scrap procurement due to narrowing steel margins and intense competition from billet flowing in from Asia and the CIS region. Chinese billet offers near $455-460/t CFR Turkiye, continued to pressure imported scrap demand, making semi-finished steel imports comparatively attractive for mills.

As a result, Turkiye’s billet imports increased by 4.4% y-o-y during Q1 CY2026, while pig iron imports surged by 51% y-o-y amid stronger demand for alternative metallics. At the same time, billet exports improved due to reduced Iranian steel output and stronger semis demand from MENA buyers.

Outlook

Turkish imported scrap demand is expected to remain cautious during Q2 of this year as mills continue facing pressure from weak domestic construction activity, volatile export markets, rising financing costs, and geopolitical uncertainty. Turkish mills are expected to maintain controlled procurement strategies while closely monitoring freight movements, steel margins, and semis pricing trends.

Seasonal tightness in European scrap collection and elevated freight costs are likely to continue supporting imported scrap prices in the upcoming days. At the same time, billet arrivals from Russia, Asia, and the MENA region are expected to remain firm as previously booked cargoes continue reaching Turkish ports. However, fresh billet bookings may gradually slow if long steel demand remains inconsistent and global semi-finished prices weaken further.

Market participants expect imported HMS 80:20 prices to remain largely firm during Q2 CY2026. However, any further escalation in Middle East tensions or additional disruptions around the Strait of Hormuz could sharply increase freight premiums, bunker fuel costs, and insurance rates again, potentially pushing imported scrap prices higher across the region. Geopolitical risks, freight economics, and competition from semis are expected to remain the key factors shaping Turkiye’s raw material trade flows during the coming quarter.

Leave a Reply