- Consumption rises 9% y-o-y, outpacing GDP growth

- Adani, Ultratech record 12-13% sales growth in FY’26

India’s cement consumption grew by around 9% y-o-y to nearly 490 million tonnes (mnt) in FY’26, compared to 453 mnt in FY’25, significantly outpacing country’s GDP growth of around 7.4% during the same period.

The stronger growth highlights robust infrastructure activity, rising housing demand, increased government capex, and accelerating construction momentum across roads, railways, urban infrastructure and industrial projects, indicating healthy long-term demand fundamentals for the Indian cement sector.

The industry operated with capacity utilisation of around 74-76% in FY’26, rising from 70-72% in FY’25, supported by robust demand growth, higher infrastructure spending and better operating leverage across major cement companies.

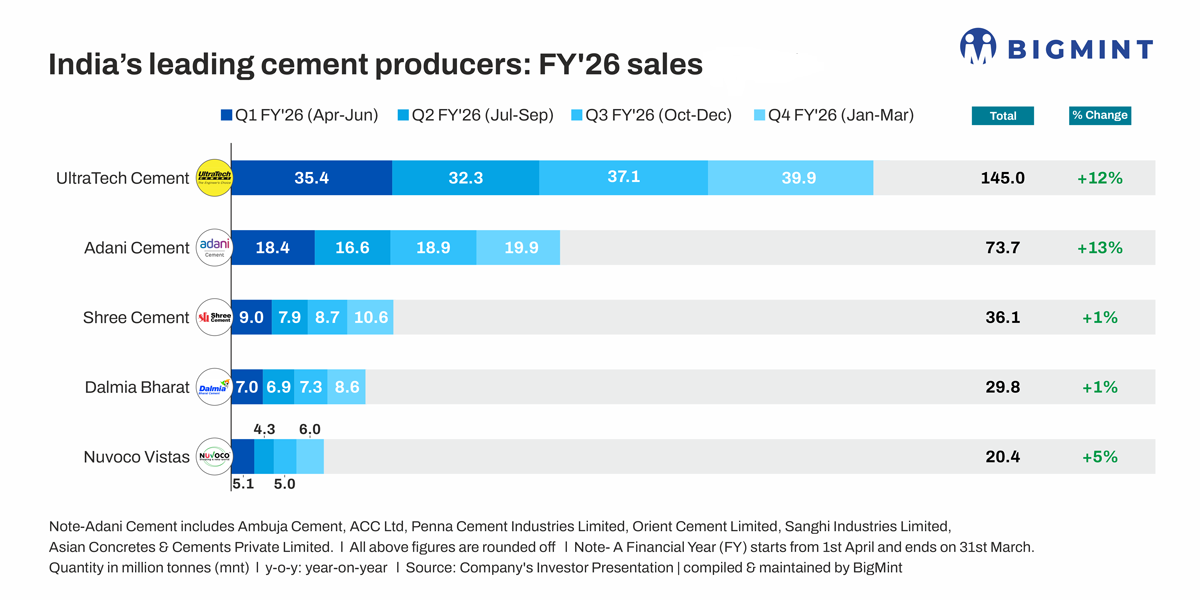

Company-wise performance

1. UltraTech Cement delivered a strong performance in FY’26 and Q4FY’26, supported by robust volume growth, improved operating efficiency, and continued capacity expansion.

Sales volumes rose 12% y-o-y to 145 mnt in FY’26, up from 129.7 mnt in FY’25. In Q4FY’26, volumes increased 7.6% q-o-q to 39.9 mnt from 37.1 mnt in Q3. Capacity utilisation improved to 89% in Q4FY’26, driven by healthy demand from housing, infrastructure, and commercial construction segments.

EBITDA per tonne increased 15% y-o-y to INR 1,130/t in FY’26, compared with INR 983/t in FY’25. The improvement was driven by better cement realisations, higher operating leverage from increased utilisation, lower fuel and logistics costs, rising share of premium products, and sustained cost optimisation across plants.

The company has now crossed 200 mnt/year of installed capacity in India following the commissioning of three grinding units with a combined capacity of 8.7 mnt/year, reinforcing its position as the world’s largest cement producer outside China in terms of capacity and sales volume.

The company invested around INR 9,600 crore in capex during FY’26 towards expansion and operational upgrades and has committed over INR 16,000 crore over the next three years to expand capacity beyond 240 mnt/year, further strengthening its long-term growth trajectory.

2. Adani Cement reported its highest-ever annual cement sales volume of 73.7 mnt in FY’26, up 13% y-o-y from 65.2 mnt in FY’25, supported by strong demand from housing, infrastructure, and commercial construction sectors.

Quarterly sales volumes increased 5% q-o-q to 19.9 mnt in Q4FY’26 against 18.9 mnt in Q3FY’26, while capacity utilisation improved to 79% in Q4 and 70% for the full fiscal year.

EBITDA per tonne rose 12% y-o-y to INR 887/t in FY’26 from INR 789/t in FY’25, aided by higher sales volumes, operational efficiencies, strategic capacity additions, and improved premium product mix. Selective pricing also supported margin expansion.

The company expanded total cement capacity to 109 mnt/year during FY’26 through the commissioning of a 10.7 mnt/year grinding capacity across Marwar, Farakka, Sankrail, Sindri, and Krishnapatnam, along with the addition of 7 mnt/year of clinker capacity at Jodhpur and Bhatapara.

Adani Cement continues expanding through new grinding units across multiple locations and a 4 mnt/year clinker unit at Maratha. The company has guided capex of around INR 8,000-9,000 crore for FY’27, primarily towards ongoing capacity expansion, clinker integration, logistics infrastructure, and efficiency improvement projects. Post commissioning, total cement capacity is expected to reach 119 mnt/year by H1FY’27.

3. Shree Cement reported stable operational performance in FY’26, with sales volumes rising 1% y-o-y to 36.1 mnt, while Q4FY’26 volumes rebounded strongly by 21% q-o-q to 10.56 mnt, reflecting improving demand momentum and higher utilisation levels.

EBITDA per tonne increased 9% y-o-y to INR 1,165/t in FY’26, supported by better cost efficiencies, fuel optimisation, and improved operating leverage.

During the quarter, the company commissioned its integrated Kodla plant in Karnataka, adding 3.65 mnt/year clinker and 3.5 mnt/year cement capacity, taking total installed capacity to 69.3 mnt/year.

Shree Cement is also undertaking further capex through a new integrated cement plant in Meghalaya and international expansion via a newly incorporated subsidiary in Mauritius.

4. Dalmia Bharat reported steady operational performance in FY’26, with sales volumes rising 1% y-o-y to 29.8 mnt, while Q4FY’26 volumes witnessed a strong 18% q-o-q rebound to 8.6 mnt, reflecting improving demand conditions and higher market traction.

EBITDA per tonne increased sharply by 25% y-o-y to INR 1,028/t in FY’26 and rose 11% q-o-q in Q4FY’26 to INR 1,025/t, supported by better realisations, lower fuel costs, operational efficiencies, and improved utilisation.

The company continues to pursue aggressive expansion plans, including the recent acquisition of 5.2 mnt/year cement assets from Jaiprakash Associates, which will increase total cement capacity to 54.7 mnt/year. Ongoing expansion projects at Belgaum, Pune, and Kadapa are expected to further enhance capacity to 61.5 mnt/year by Q3FY’28. The company remains focused on long-term brownfield expansion, cost leadership, and sustainability-led capex initiatives across its operations.

5. Nuvoco Vistas Corp. reported strong operational performance in FY’26, with sales volumes rising 5% y-o-y to 20.4 mnt, while Q4FY’26 volumes increased 5% q-o-q to 6 mnt, supported by healthy cement demand from December 2025 and improved market penetration.

The company’s EBITDA per tonne surged 28% y-o-y to INR 905/t in FY’26 and improved further to INR 979/t in Q4FY’26, driven by better realisations, operating leverage, fuel cost moderation, and ongoing efficiency initiatives.

The company continues to pursue an aggressive expansion strategy, targeting a total cement capacity of 35 mnt/year by FY’28 through the operationalisation of Vadraj Cement assets and a planned 4 mnt/year expansion in East India. The Vadraj clinker and grinding units are expected to be commissioned in phases starting from Q3FY’27.

For FY’27, the company’s capex is estimated at INR 1,000-1,100 crore, focused on Vadraj project execution, eastern India grinding expansion, logistics infrastructure, and bulk terminal development at Sachana, Gujarat. The company has also approved a 1.5 mnt/year bulk cement terminal with dedicated railway siding in Gujarat to strengthen western market penetration.

Outlook

India’s cement industry remains optimistic for FY’27, driven by strong infrastructure, housing, and public capex-led demand. Demand growth is expected at 6-8%, while EBITDA per tonne is likely to remain healthy, supported by stable fuel costs and operational efficiencies. The sector also continues to witness significant brownfield and greenfield capacity expansion across key regions.

*Note- Adani Cement includes Ambuja Cement, ACC Ltd, Penna Cement Industries Limited, Orient Cement Limited, Sanghi Industries Limited, Asian Concretes & Cements Private Limited.

Leave a Reply