- Red Sea crisis diverts cargo from Asia to Turkiye

- Scrap prices fall to two-yr lows, look attractive

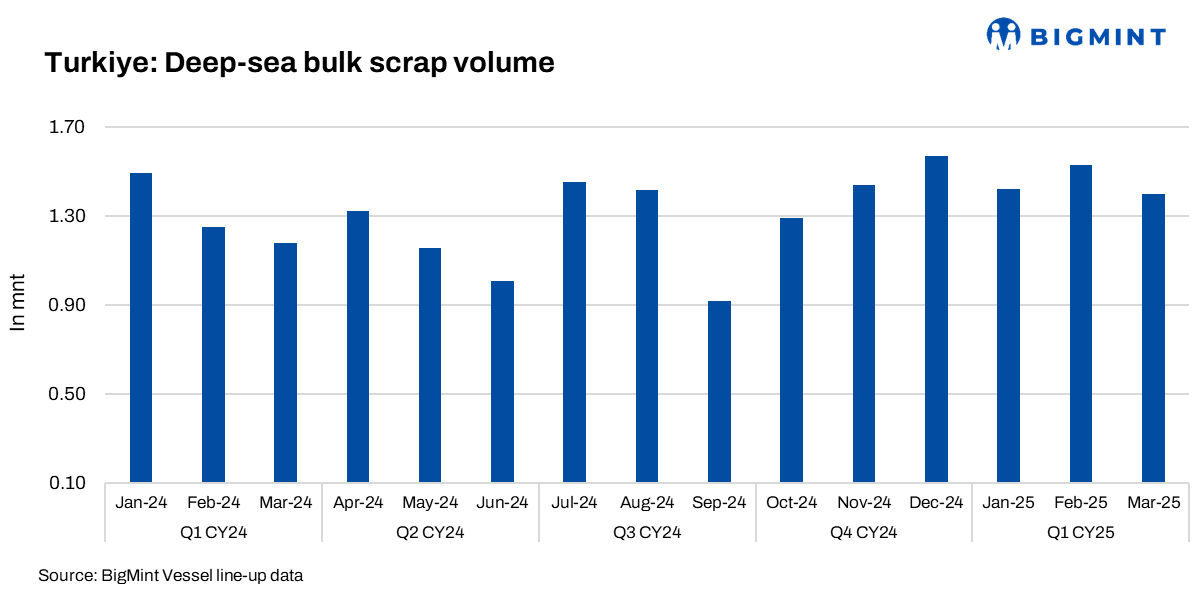

Turkiye’s deep-sea bulk scrap volume in Q1CY’25 witnessed a rise of 15% y-o-y to 4.53 million tonnes (mnt) compared to 3.93 mnt in Q1CY’24. However, March 2025 saw a decline in bulk vessel movements to 1.4 mnt, down 8% m-o-m from 1.53 mnt in February 2025.

According to BigMint’s vessel line-up data, In Q1CY’25, Turkiye handled around 100 deep-sea bulk vessels, with total shipments reaching approximately 200 when including short-sea movements.

Factors behind rise in bulk vessel movement

Redirection of bulk cargoes to Turkiye: The surge in Turkiye’s ferrous scrap imports during Q1CY’25 was largely fuelled by a redirection of cargoes from traditional Asian buyers. As the Red Sea crisis escalated, buyers in Asian countries like Bangladesh and India grew hesitant to book US and EU-origin scrap due to elevated freight costs and shipping disruptions. This led to a build-up of available volumes in Europe and the US, which were swiftly redirected to Turkiye. Benefiting from this diversion, Turkish mills capitalised on the increased availability and competitive pricing, significantly boosting import volumes during the quarter.

Quarterly price average

- US-origin HMS 80:20 CFR Turkiye: Averaged $357/t in Q1CY’25, down $50/t from $407/t in Q1CY’24.

- US-origin HMS 80:20 FOB East Coast US: Averaged $336/t in Q1CY’25, down $46/t from $382/t in Q1CY’24.

- Rotterdam HMS 80:20 bulk FOB Europe: Average prices declined to $331/t in Q1 CY’25 from $375/t in Q1 CY’24, marking a drop of $44/t.

Billet imports rise: Turkiye’s billet imports in Q1 2025 totalled 1.81 mnt, up from 1.64 mnt in Q1 2024, marking an increase of 0.17 mnt or 10% y-o-y.

Scrap price fall to 2-year lows; recover in Q1

Turkiye’s deep-sea ferrous scrap market saw a gradual recovery after hitting two-year lows in January 2025. Prices initially dropped to $335/t CFR due to sluggish steel demand and high scrap availability. A rebound began as mills resumed bookings for February-March shipments, backed by tighter supply and improving sentiments in China and the US.

By the quarter-end, US-origin HMS 80:20 rose to $375-385/t CFR and mills struggled with squeezed margins, currency depreciation, and low rebar demand during Ramadan, keeping procurement cautious.

Key updates

Turkiye’s crude steel production in Q1CY’25 stood at 9.1 mnt, witnessing a 4% drop y-o-y as compared to 9.5 mnt in Q1CY’24.

The Turkish lira, on the other hand, witnessed a drop of 14% with the average value dropping to TRY 36.6 as compared to TRY 32.05 in Q1 CY’24.

Outlook

Outlook

Market participants remain divided on the near-term outlook. While some expect a slow recovery in scrap prices supported by tight supply and improving billet trends, others remain cautious amid weak long steel demand and margin pressure.

US and EU sellers are holding firm on elevated price expectations due to limited availability, but Turkish buyers are expected to proceed cautiously until demand clarity improves. Any price gains in the coming weeks are likely to be gradual and closely tied to developments in rebar exports, construction activity, and overall macro-economic stability.

Turkish mills are unlikely to accept higher offers in the immediate term, especially with rebar demand still subdued post-Ramadan.

Leave a Reply