- Pakistan scrap imports subdued amid weak buying

- Bangladesh scrap trade slow, prices under pressure

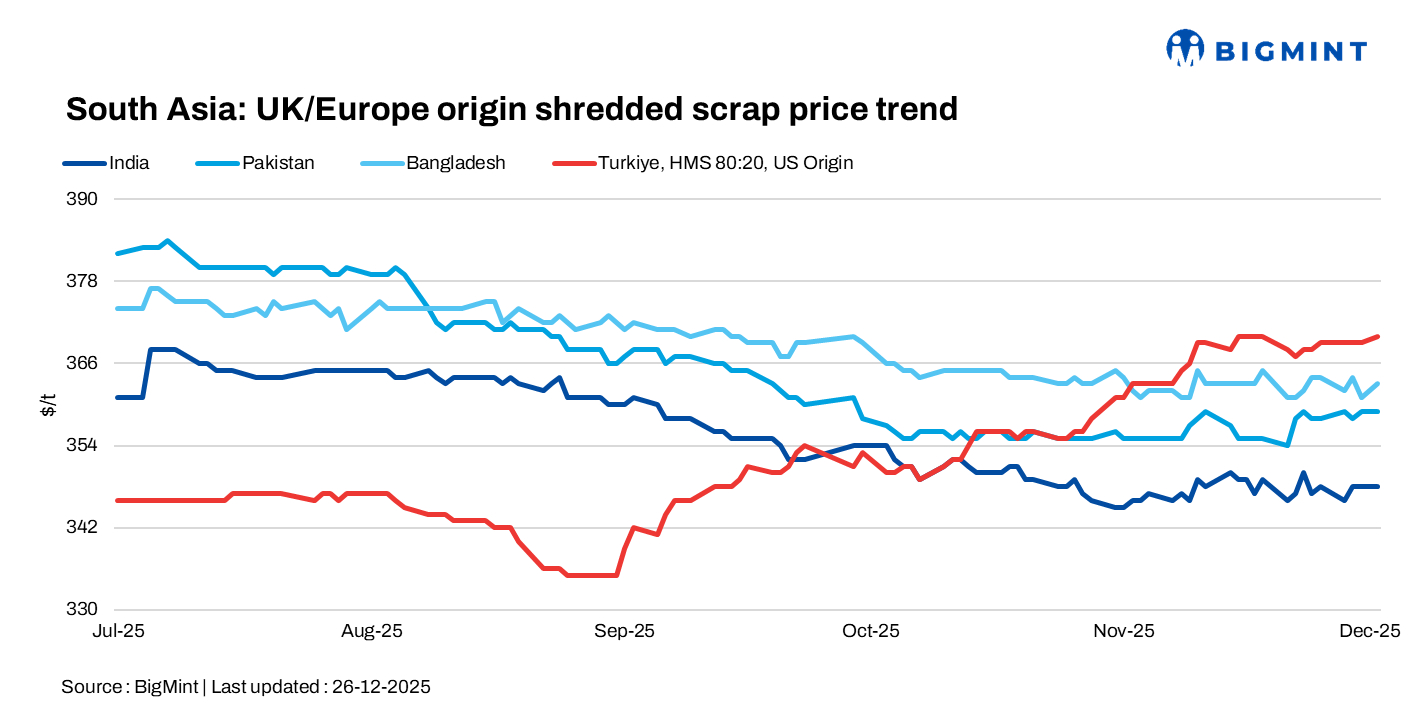

South Asia’s imported scrap markets remained largely subdued on 26 December, amid year-end slowdowns, with limited buying interest in Pakistan and Bangladesh, stable pricing in Turkiye, and cautious sentiment prevailing as mills assessed currency pressures and near-term steel demand.

India: Indian imported containerized shredded scrap prices remained steady ahead of the holiday season, as buying interest in the import market stayed limited despite a gradual uptick in domestic finished steel prices. Offers from Australia to India were reported at $315-318/t for HMS 80:20, $325-326/t for HMS 1, $335-340/t for shredded scrap, and $345-350/t for PNS, while indicative levels for EU-origin material stood at $345-350/t CFR Nhava Sheva for shredded scrap and $316-320/t for HMS 80:20.

Pakistan: Pakistan’s imported scrap market remained subdued, with prices assessed at $355-358/t for imported material. Shredded scrap offers were heard around $360/t, but buying interest stayed weak due to year-end slowdowns, forcing buyers to either accept unfavourable exchange rates or delay payments, which continued to restrict fresh transactions.

Bangladesh: The imported scrap market in Bangladesh witnessed slow movement during the day, with Australia-to-Bangladesh offers reported at $325-330/t for HMS 80:20, $335-340/t for HMS 1, $358-360/t for shredded scrap, and $362-365/t for PNS. Fresh shredded scrap offers from Australia were heard slightly higher at $360-362/t CFR, while PNS offers from Singapore and Hong Kong were quoted at $360-366/t CFR. Meanwhile, local melting scrap and ship scrap prices softened to BDT 45,000-48,000/t ($368-393/t), keeping buyers cautious and limiting fresh bookings.

Turkiye: Deep-sea imported scrap prices remained stable on December 26, with market participants reporting increased deal activity as mills secured cargoes ahead of the Christmas holiday period. Several sources remained bullish, noting that Turkish steelmakers continued to require material for late January and early February shipments, although overall market activity was expected to slow as the Christmas holidays approached, while US-origin scrap levels were heard around $370/t.

Leave a Reply