- India’s recycling activity dips amid weak fundamentals.

- Gadani competitiveness falls without HKC-approved yards.

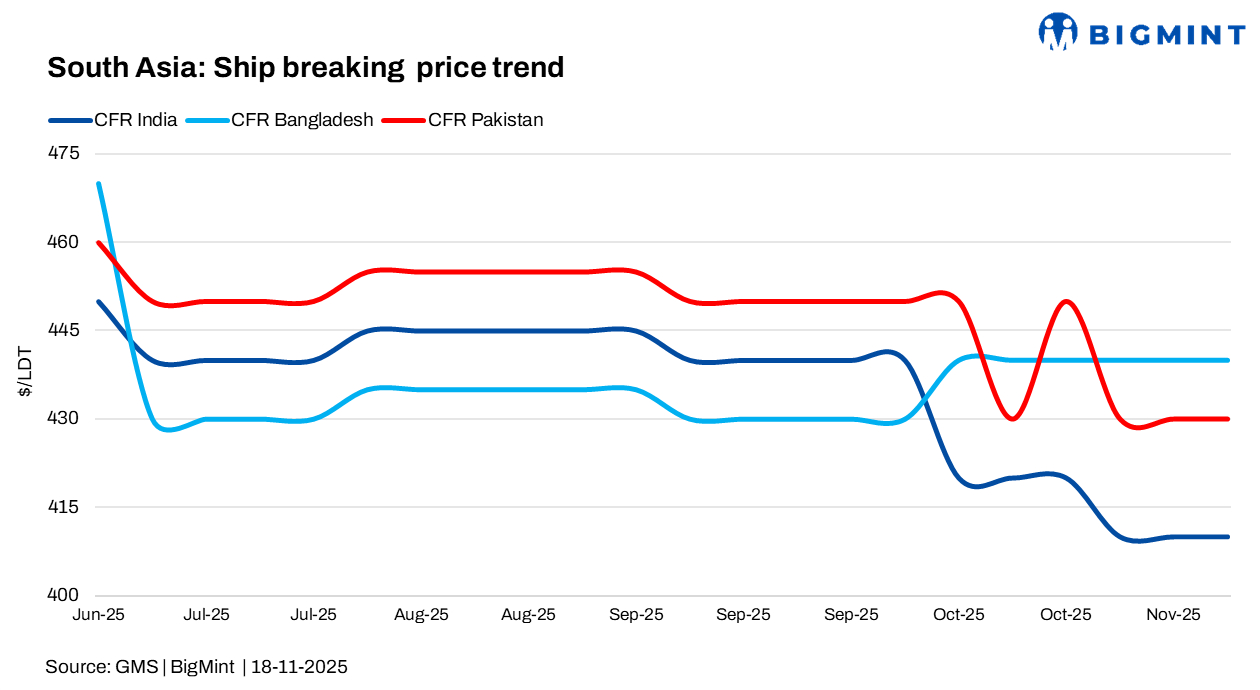

Alang, Chattogram, and Gadani all saw weak sentiment despite steady LDT arrivals, with India and Pakistan pressured by low prices and soft demand, while Bangladesh recorded higher vessel inflow but remained constrained by economic and political challenges.

India: Alang market stays weak as supply slumps and sentiment declines

Alang’s price competitiveness has dipped, softening market activity, though it remains the most reliable HKC-compliant recycling hub. Limited demand, few offers, and a sharp fall in vessel supply continue to pressure prices.

Smaller units that avoided Gadani are still heading to Alang, but fundamentals remain weak, steel plate prices only slightly up by $4/t, and smaller dry units struggling to reach $400/t. With 2026 expected to mirror 2025’s challenges, industry sentiment stays subdued.

Bangladesh: Vessel arrivals improve, but demand remains weak

Chattogram received around seven vessels totaling nearly 66,000 LDT this week, supported by privately held units finally entering the market. However, overall demand remains weak, and Bangladesh has seen very limited ship arrivals since June despite firmer offers.

High tariffs, monsoons, inflation, a falling Taka, and rising political violence continue to pressure the market. With steel plate prices slipping and elections nearing, Bangladesh’s ship-recycling outlook for late 2025 remains subdued despite the brief uptick in tonnage.

Gadani: Market Remains Under Pressure

Pakistan’s ship-recycling market continues to weaken as yard upgrades still haven’t produced an HKC-approved facility. Weak bids, rising inflation, cheaper Iranian steel, falling plate prices below $600/t, and a softer PKR around $283/t are hurting sentiment. Gadani’s competitiveness is low, with even small vessels stuck at anchorage for weeks.

With no new arrivals and ongoing HKC hurdles, Pakistan risks further decline unless yard improvements and tariff support accelerate. The situation remains bleak, especially considering only 16 vessels were delivered in all of 2023-a stark contrast to the higher arrivals seen across other regional markets this week.

Tonnage received last week

Leave a Reply