- Alang’s falling prices attributed to weak steel demand

- Bangladesh hit by NOC issues, Pak introduces IHM rules

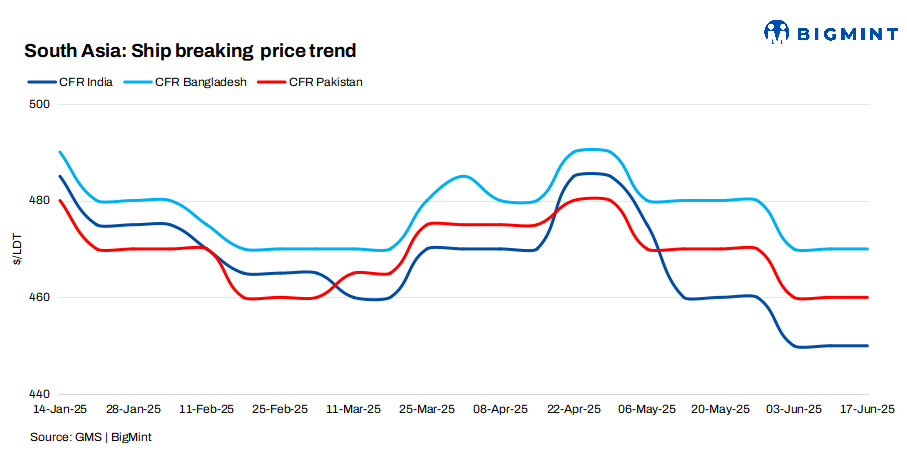

South Asia’s ship-breaking markets remain under pressure as prices fall and tonnage supply tightens. Alang stays busiest despite weak margins, while Pakistan introduces Inventory of Hazardous Materials (IHM) rules and Bangladesh sees low arrivals despite progress on compliance with the Hong Kong International Convention for the Safe and Environmentally Sound Recycling of Ships, 2009 (HKC) norms.

Alang stays active despite margin squeeze

India’s shipbreaking market remains the weakest in the subcontinent, with bulkers now being offered at as low as $400/light displacement tonnage (LDT) levels. The continued price decline is driven by falling domestic steel prices and fears of cheaper Chinese exports entering the market following the recent 50% steel export tariffs.

Steel plate prices in India have dropped by nearly $30/t over the past month. Despite low pricing, Alang remains the most active yard, as Bangladesh has stepped back from bidding and Pakistan continues to lack HKC compliance. As a result, Alang received around 55,000 LDT across 7 vessels this week, though shrinking margins remain a concern.

According to market participants, “The ship-breaking sector in India is under severe strain. There are no profits, maintenance costs remain high, and most deals are at breakeven or in loss. Even at $450/LDT, recyclers are incurring losses of INR 1,000-2,000/t. However, some continue to invest, anticipating future supply shortages if geopolitical tensions (war) escalate. While Alang may benefit from HKC compliance, the core challenge is the lack of tonnage, as ship-owners are unwilling to sell. Demand remains strong, but availability is poor, and the outlook for the next six months is bleak.”

Gadani introduces IHM rule ahead of HKC enforcement

The Pakistan market is making slow progress toward HKC compliance, with a new rule requiring Inventory of Hazardous Materials (IHM) certificates for beaching. However, weak infrastructure and limited yard upgrades are holding back competitiveness, despite prices offered being higher than India’s.

Local fundamentals remain weak. Steel prices stayed flat at $615/t. The new budget proposed a 5% customs duty on re-rollable scrap, alongside stricter limits on the permissible percentage of non-mutilated material per lot. While IMF support and growing HKC awareness are positives, ship owners still prefer India’s certified yards. Without faster local HKC certifications, Pakistan may continue to miss tonnage.

Chattogram slows despite HKC progress

Bangladesh’s ship recycling sector is advancing with HKC upgrades, as more yards move toward compliance. However, vessel imports remain stalled due to continued NOC restrictions, with only one small RoRo vessel reported offshore in the last two weeks. Some non-HKC yard deals await clearance once certifications are granted.

Steel plate prices fell by $7-8/t to $546-548/t. The Taka weakened slightly, and Eid holidays have further slowed activity. Weak demand and monsoon disruptions have redirected tonnage to India. Still, this lull is helping Bangladeshi yards finalize key HKC upgrades, though price and demand remain under pressure.

Last week, Gadani Port received 20,562 LDT compared with 10,176 LDT in the previous week.

Alang Port received 53,521 LDT compared with 31,457 LDT in the previous week.

Chattogram Port received 2,985 LDT compared with 11,842 LDT in the previous week.

![]()

Leave a Reply