- Pak, Bangladesh buyers cautious ahead of Eid

- Turkiye eyes lower prices on amply EU supply

The South Asian imported scrap market showed cautious activity across key countries as regional steel demand remained subdued and logistical challenges persisted. India grappled with weak finished steel demand and stiff competition from alternatives like sponge iron, while Pakistan faced high freight costs and slow downstream buying ahead of Eid.

Bangladesh’s market was weighed down by financial constraints and seasonal slowdown, with mills focusing on inventory management.

Meanwhile, Turkiye’s import prices held steady amid mixed buyer-seller expectations and ample European supply.

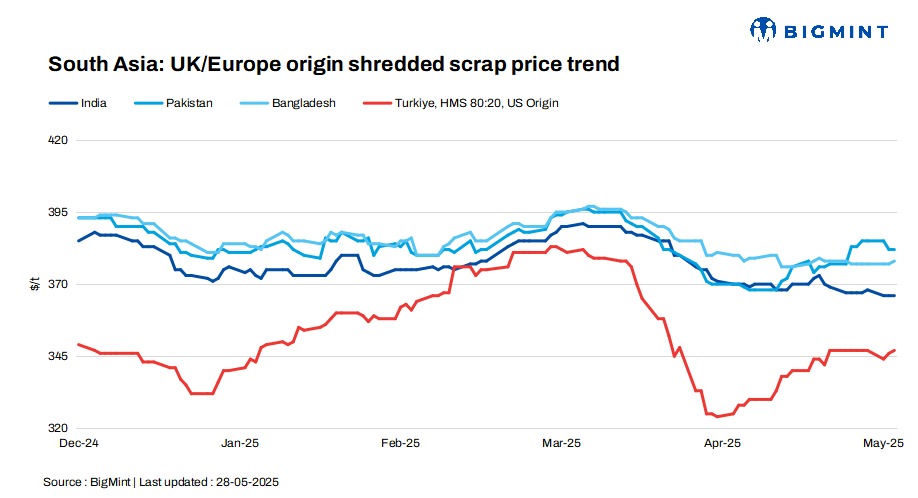

D-o-d, UK-origin shredded scrap offers held steady in India and Pakistan, while edging up by $1/t in Bangladesh. US-origin bulk HMS 80:20 offers to Turkiye inched up by $1/t d-o-d.

Market overview

India: India’s imported scrap market remained lacklustre due to weak finished steel demand, tight margins, and growing preference for sponge iron and pellets. Mills leaned towards short-transit cargoes given the uncertainty over the coming two months and the onset of the monsoon.

Shredded scrap offers from Australia to Chennai were heard at $370-375/t CFR, while bids hovered at $365-366/t. HMS 80:20 was offered at $355-360/t CFR Chennai, with buyer bids near $350/t. On the west coast, HMS from Kuwait and Bahrain was offered at $365-367/t, but buyers limited their interest to $360/t.

A trader noted, “The market is not supportive, import viability is low, sponge intake is rising, and availability is tightening.”

Pakistan: Pakistan’s imported scrap market remained quiet amid high freight costs, weak steel demand, and the approaching Eid holidays. Mills maintained low inventories as downstream demand stayed sluggish. Shredded offers from the UK/EU ranged at $384-388/t CFR Port Qasim, but most bids hovered at around $380-382/t, with a few small deals concluded at $382-385/t.

UAE-origin shredded was offered at $390-392/t and HMS at $370–375/t, though interest remained limited.

Domestic rebar prices stood at PKR 235,000-238,000/t ($832-843/t), while local scrap traded at PKR 135,000-140,000/t ($478-496/t). Despite slight price hikes by some major mills, overall sentiment remained cautious with low booking activity ahead of the holidays.

Bangladesh: Bangladesh’s imported scrap market remained sluggish amid LC issues, high freight rates, and a seasonal slowdown ahead of Eid and the national budget. Mills avoided bulk bookings, focusing on inventory management. Limited containerised trades were reported — PNS at $380-385/t CFR and shredded at $370-378/t CFR. Domestic scrap prices stood at BDT 53,000-55,000/t ($435-452/t), while rebar dropped to BDT 82,000-83,000/t in Dhaka and BDT 84,000-86,000/t in Chattogram, down BDT 3,000-4,000/t from early May. With weak construction activity and the Eid holidays approaching, market sentiment is expected to stay soft through mid-June.

Turkiye: The Turkish imported scrap market stayed range-bound with a slight upward movement driven by an EU-origin deal at $343/t CFR. US-origin bulk HMS 80:20 was assessed at $347/t CFR, up $1/t d-o-d. Mills continued to seek lower prices due to ample European supply, but sellers remained firm, limiting any downward correction. Most tradable values for US/Baltic material hovered at around $346–$347/mt CFR, with US offers largely absent. While mills anticipated a price softening, some sellers still targeted levels near $350/t CFR. This divergence in expectations kept market sentiment mixed and negotiations at a standstill.

Price assessments

India: UK-origin shredded indicatives were assessed at $366/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives stood at $382/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $378/t CFR Chattogram, up by $1/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $347/t CFR Turkiye, up by $1/t d-o-d.

Leave a Reply