- BHP, Rio Tinto actively seeking cargoes

- No fixtures on South Africa- China route

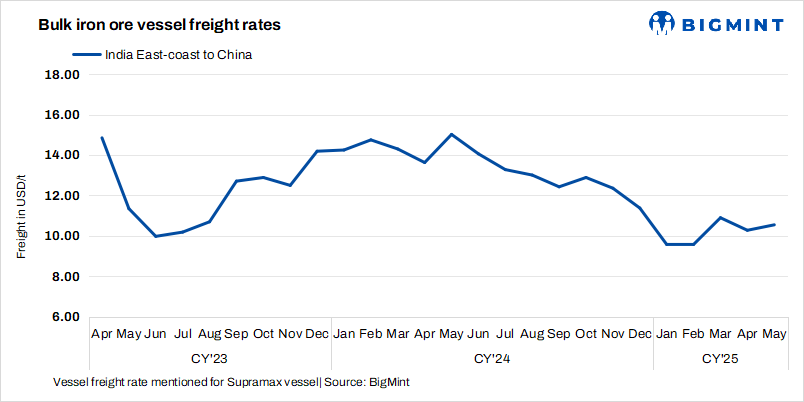

Despite subdued sentiment across the broader Supramax market, freight rates on the India-China route remained range-bound, supported by short-lived but concentrated cargo demand. A surge in iron ore and agricultural commodity shipments, driven by opportunistic buying from Chinese importers ahead of expected policy or seasonal shifts, created localised tightness in vessel availability. While not strong enough to trigger a sustained rally, this demand helped keep rates from sliding further.

Simultaneously, the onset of the monsoon season along India’s west coast disrupted port operations, slowing down vessel turnaround times and contributing to temporary supply-side constraints. These delays, coupled with port congestion, limited the prompt tonnage pool and helped keep freight rates within a narrow upward band. Broader market weakness persisted in the Indian Ocean and Pacific regions, but localised imbalances on the India-China leg prevented a significant rate correction.

Meanwhile, Capesize iron ore vessel freight rose primarily due to increased chartering interest from major mining companies in both the Pacific and Atlantic basins. In the Pacific, after a period of robust activity in the previous week, mining giants like BHP and Rio Tinto returned to the market, seeking multiple Capesize vessels for mid-June laycans from Western Australia to Qingdao. This fresh round of cargo inquiries, despite being relatively moderate, added marginal support to tonnage demand and propped up freight rates temporarily, even as broader trading activity slowed. The limited number of new ship offers from owners further tightened supply, helping maintain rate levels.

A cluster of charterers, entered the market simultaneously, seeking vessels for late June laycans. The overlap in demand for a narrow loading window created competitive pressure among charterers to secure tonnage, pushing rates higher.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.6/t, edging down by $0.2/t w-o-w. Market participants reported that a recent fixture for a mid-June loading was concluded at approximately $12/t, while additional fixtures were heard in the range of $8.5/t, indicating a wide spread influenced by specific cargo requirements and vessel availability.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $8.4/t on 28 May, rising by $0.7/t w-o-w. According to sources, major Australian miners Rio Tinto and BHP booked Capesize vessels from a Western Australian port to Qingdao at around $8.20-8.35/t. Shipment is scheduled for 7-16 June.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $18.7/t on 28 May, marginally up by $0.2/t w-o-w. As per sources, Vale booked a Capesize vessel from Tubarao to Qingdao at $18.60/t for the shipment period of 14-23 June.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao increased by $0.2/t w-o-w to $14.4/t on 28 May. Sources informed BigMint that limited vessel availability for mid-to-late June laycans also contributed to upward pressure. Additionally, charterers actively seeking tonnage signalled sustained demand, helping rates to hold firm.

Leave a Reply