- Bangladesh: Stable ranges with steady but cautious demand

- Turkiye: No offers heard; mills waiting amid weak rebar demand

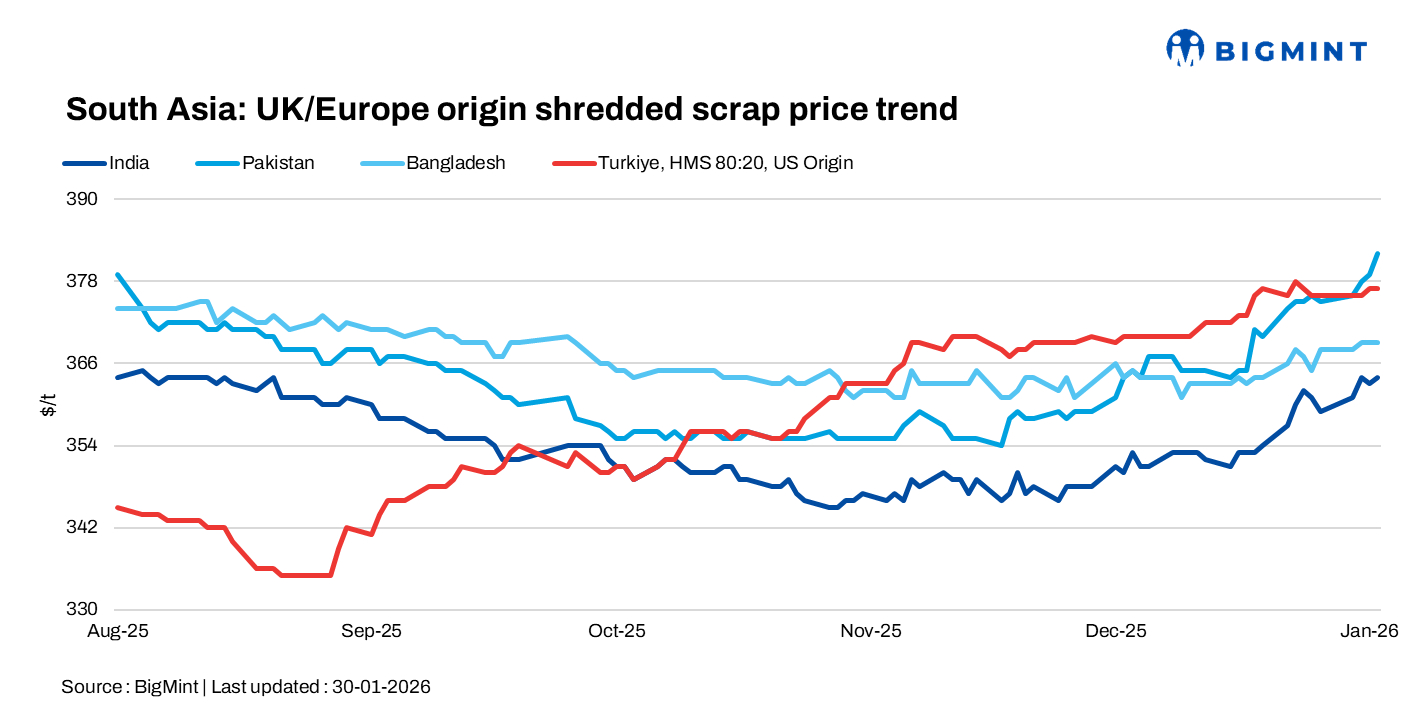

South Asia’s imported scrap market stayed subdued on 30 January, with India and Pakistan recording selective buying and Bangladesh registering steady price ranges. Turkiye remained supported by higher costs, though weak rebar demand kept mills cautious and overall trading sentiment muted.

Region-wise highlights

India: Imported containerised shredded offers were heard around 365 CFR Nhava Sheva, while bids hovered at 350-355, keeping trading largely stagnant as offer levels remained steady. Mill buying interest improved, but most activity stayed focused on domestic scrap and DRI as the rupee’s depreciation continued to weigh on imported bookings.

In the South, Australia-origin 22-ton loading HMS 80:20 was heard around 340 CFR Chennai, while Central America 40-ft HMS 80:20 was discussed near 325 CFR Chennai. Demand has begun to show some improvement, although only selective buyers are currently willing to accept the higher price indications.

Pakistan: Imported shredded scrap in Pakistan showed mixed indications, with UK/EU suppliers offering around 380 CFR, UAE material heard at 395-plus, and a Bahrain-origin parcel likely to settle near 390-plus. HMS buying remained steady, with workable levels in the 365-375 CFR range, keeping Pakistan attractive for suppliers. Overall imported sentiment hovered near 380 CFR as buyers selectively engaged at workable levels.

Bangladesh: Imported ferrous scrap prices in Bangladesh stayed largely stable, with Japanese H2 reported at 355-357 CFR Chattogram. Containerised Oceania-origin material also remained within its usual range, with HMS 80:20 at 345-350, HMS 1 at 355-360, and shredded at 365-370 CFR. In the downstream market, rebar brands were trading between BDT 75,000-80,000/t (about 614-655), reflecting a steady but cautious sentiment.

Turkiye: Deepsea imported scrap prices inched higher on 30 January, supported by a stronger euro, firm collection costs, and rising dry bulk freight rates. European suppliers faced breakeven levels in the high-370s CFR, while US yards stayed focused on the stronger domestic market, where February shredded settlements are expected to rise.

US-origin material was indicated around 380-382 CFR, EU scrap near 375, and Baltic cargoes at 377-378. However, Turkish mills continued to resist higher prices as weak rebar demand kept buying interest low, leaving mills in a wait-and-watch mode and avoiding expensive scrap.

Leave a Reply