- Surplus domestic scrap piles pressure on prices

- GST inspections disrupt trade flows, keep spot deals limited

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 100/tonne (t) d-o-d to INR 38,400/t DAP on 30 January 2026.However, the index decreased by INR 250/t w-o-w.

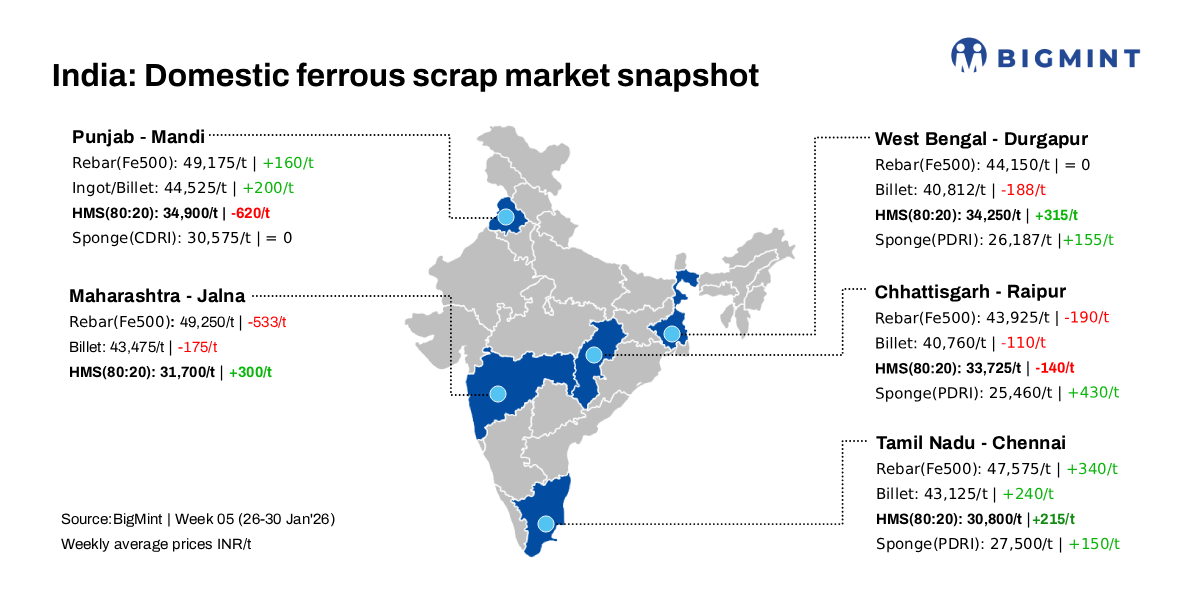

Steel market activity in Mandi Gobindgarh remained moderate, with scrap prices declining by INR 250-620/t. Scrap inquiries stayed limited as GST checks disrupted material movement and demand visibility remained weak. While suppliers attempted to hold offers firm, persistent bid-offer gaps across key markets reflected buyer resistance at higher levels. Imported scrap demand continued to remain muted, weighed down by the availability of cheaper domestic alternatives.

Over the past few weeks, scrap prices in Mandi Gobindgarh have declined sharply. The correction was primarily driven by excessive inflows of domestic scrap from neighbouring states, which flooded the market amid sluggish finished steel off-take. Mills adopted a strictly hand-to-mouth buying strategy, further pressuring local suppliers to revise offers downward to sustain volumes.

Finished steel cues offer mild support

Primary steel mills have recently raised finished steel prices, providing some directional support to sentiment. However, secondary steel producers largely remained on the sidelines, awaiting sustained improvement in demand before rebuilding scrap inventories.

A mill owner informed, “In the near term, scrap prices in Mandi Gobindgarh are likely to remain range-bound, with any recovery dependent on easing GST-related disruptions, moderation in scrap inflows, and firmer finished steel demand.”

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh remained stable d-o-d at INR 30,700/t (DAP). Prices remained flat w-o-w.

Steel-grade pig iron prices in Ludhiana rose by INR 100/t d-o-d to INR 40,500/t (DAP), while recording a w-o-w increase of INR 480/t.

Steel market dynamics

In the semi-finished steel segment, ingot prices in Mandi Gobindgarh fell by INR 100/t d-o-d to INR 44,600/t DAP, while prices across other major production hubs dropped by INR 100-550/t over the same period. On a w-o-w basis, ingot prices in Mandi rose by INR 200/t.

Rebar (Fe 500) prices in Mandi Gobindgarh fell by INR 100/t d-o-d to INR 49,200/t. On a w-o-w basis, prices marginally increased by INR 160/t.

Overview of Mumbai steel market

Rebar (Fe 500) prices on the Mumbai IF route increased by INR 200 to INR 50,700/t ex-works. Buying activity remained moderate throughout the day, as continuous upward movement in prices resulted in selective purchasing. Notably, mills did not face any significant selling pressure and maintained firm offers, reflecting confidence in prevailing price levels. Dispatches of previously booked material were smooth.

On the raw material side, HMS (80:20) scrap was assessed at INR 32,700/t DAP, with the scrap-billet conversion spread hovering around INR 11,000/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,900-6,300/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $335-$337/t, approximately INR 33,196/t (inclusive of freight). HMS (80:20) prices in Mumbai increased by INR 200/t d-o-d to INR 32,700/t DAP. Indicative prices of shredded from Europe stood at $$362-$364/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,050/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply