- India, Pakistan, Bangladesh: Weak demand, buyers selective, offers unworkable

- Turkiye: Scrap demand firmer, activity supported by tight supply

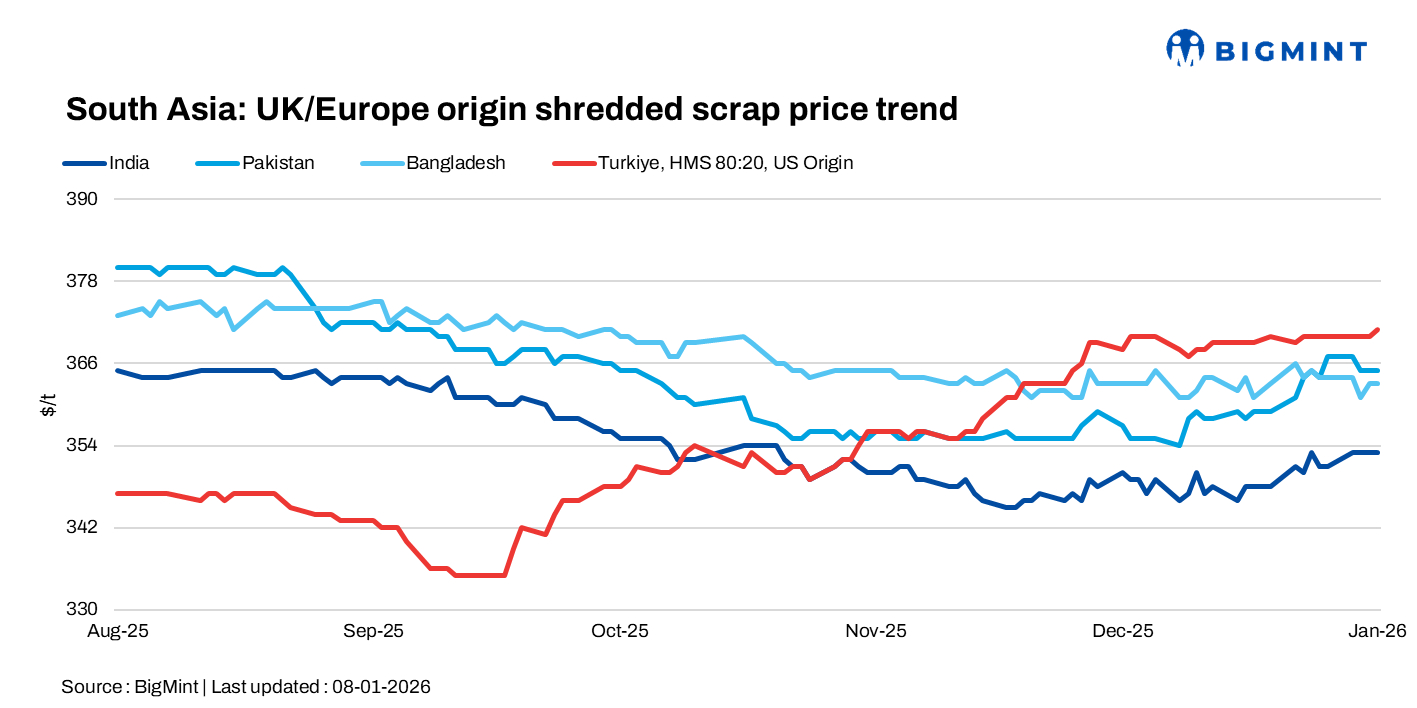

South Asia’s imported scrap markets remained subdued and highly selective, as high offer levels and weak downstream demand limited buying interest, while Turkiye stood out with relatively firmer activity supported by tight scrap availability despite seasonal demand challenges.

India: India’s imported containerised scrap market remained quiet, as improving steel demand failed to translate into buying interest due to largely unworkable offer levels. Indicative offers into Mundra and Nhava Sheva included EU-origin HMS 80:20 at $335-340/t CFR and UK-origin shredded at around $355/t CFR, with buyers remaining cautious and highly price-sensitive.

Prices for recent deals were heard at $335-340/t CFR west coast India for Somalia-origin HMS and around $310/t for Somalia-origin LMS. Meanwhile, PNS with Bluesteel mix (1% max impurity), in parcel sizes of 300-500 t on HMM line, was offered at around $370/t, subject to reconfirmation.

Pakistan: The market remained selective, with export offers staying high for Pakistan and India, while the imported scrap segment stayed muted as buyers showed limited appetite and focused only on workable levels of around $362-364/t CFR, even as weak import interest contrasted with elevated domestic scrap prices, which were indicated at around PKR 130,000/t ($463/t).

Bangladesh: The scrap import market remained weak, with buyers showing limited appetite and highly selective procurement. Japanese H2 was quoted at $345/t, while domestic rebar prices remained largely unchanged at around BDT 78,000/t ($638/t) in Chattogram and BDT 73,000-74,000/t ($597-605/t) in Dhaka.

Turkiye: Imported scrap market remained active, with two US-origin deals heard at $371-372/t CFR. Buying interest was supported by tight scrap availability, while mills continued sourcing from the US despite higher freight costs, as demand from India and Bangladesh has weakened in recent months.

Domestic steel sentiment stayed cautious. Rebar prices held steady at around $570/t ex-works and $555-560/t FOB, but winter conditions and expected delays in housing and infrastructure projects continued to slow construction activity. Despite weaker rebar sales, scrap sellers stayed confident on expectations of further price gains.

Leave a Reply