- Domestic premiums remain stable at $230-240/t

- China relocates Henan aluminium capacity to Inner Mongolia

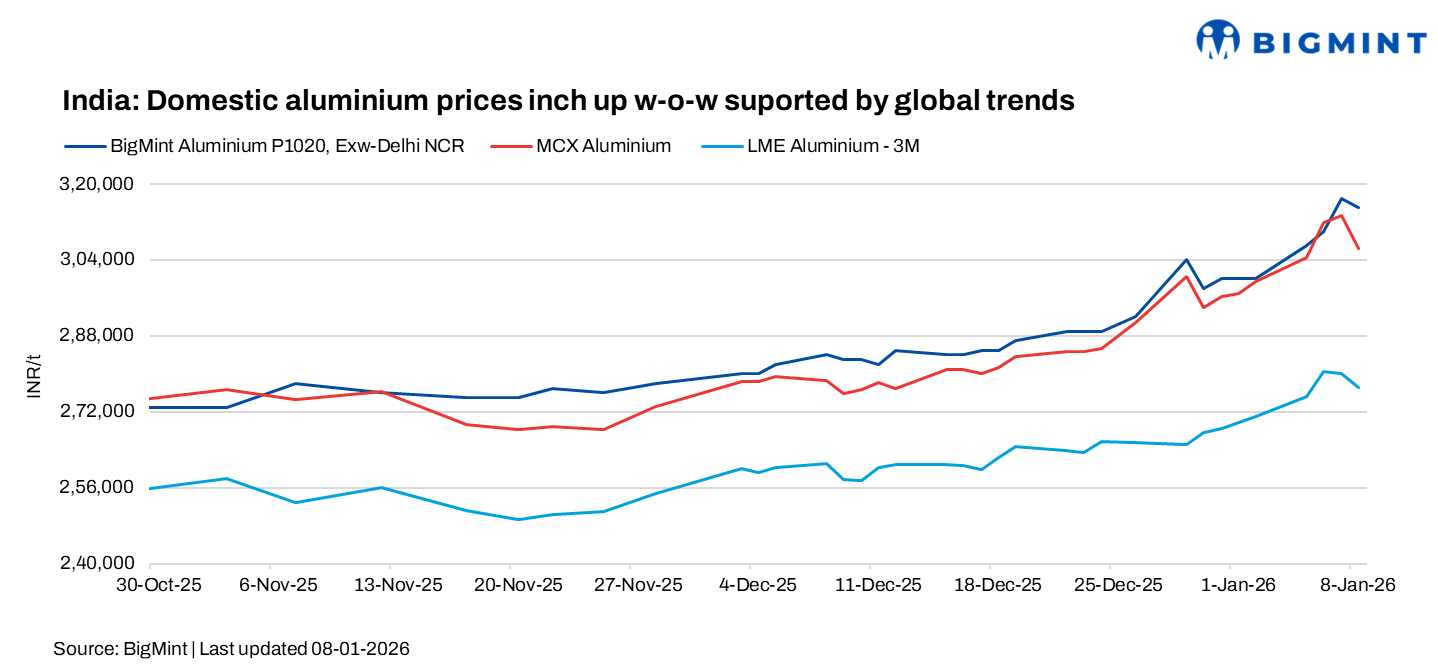

Domestic aluminium prices in India registered sharp w-o-w gains following upward price revisions by primary producers amid firm LME and MCX aluminium futures and persistent global supply concerns. The uptick in prices came despite comfortable domestic availability and only a modest improvement in downstream demand, underscoring the strong influence of global market cues on local prices.

According to BigMint’s assessment, domestic aluminium prices in Delhi increased by INR 15,000/t, or 5% w-o-w, to INR 315,000/t, while Mumbai prices rose by INR 10,000/t, or 3.3%, to INR 312,000/t as assessed on 8 January.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX continued to strengthen during the week, rising by INR 9,600/t, or 3%, from INR 296,900/t to INR 306,500/t. The upward move reflected firm underlying physical market conditions, supported by steady spot demand and higher regional prices rather than purely speculative activity.

LME aluminium three-month prices posted stronger gains, increasing by $116/t, or 3.9%, to $3,113/t, driven by persistent supply-side concerns and sustained buying interest. Ongoing smelter-related disruptions and broader global supply risks continued to reinforce a tight aluminium market outlook.

Meanwhile, LME warehouse stocks declined by 10,000 t, or 2% w-o-w, to 501,750 t, highlighting continued inventory drawdowns. The combination of falling exchange stocks, firm domestic spot trends, and elevated global prices helped keep MCX aluminium futures on a strong footing through the week.

Aluminium majors raise offers

The continued rise in domestic aluminium ingot prices was driven by multiple upward revisions from the primary producers during the week. BALCO raised its P1020 price in a series of hikes, moving from INR 316,500/t on 1 January to INR 321,250/t on 3 January, further to INR 325,000/t on 6 January, and finally to INR 332,000/t on 7 January.

Hindalco also implemented successive increases, revising its P1020 price from INR 316,750/t on 1 January to INR 319,250/t on 3 January, then to INR 323,250/t on 6 January and INR 330,000/t on 7 January, reflecting firm market confidence.

Meanwhile, NALCO initially held its P1020 price steady at INR 307,200/t on 1 January before sharply raising it to INR 320,000/t on 7 January, signalling a shift toward a stronger pricing stance amid improving market sentiment.

Market participants reported that domestic aluminium premiums in the Delhi NCR region held steady w-o-w at $230-240/t above LME cash, indicating stable market fundamentals. The recent rise in domestic prices was largely driven strong LME and MCX aluminium markets rather than a significant pickup in local demand, as supply conditions remained comfortable with one major primary producer holding ample inventories. Although overall demand continues to remain soft, participants observed a gradual improvement compared with the subdued levels seen over the past two to three months.

Additionally, global primary aluminium production reached 67.49 mnt in 11MCY’25, up 1.1% y-o-y, although November output declined 3.3% m-o-m to 6.09 mnt.

Global market enters into structural adjustment

China has approved the relocation of 240,000 t/year of primary aluminium smelting capacity from Henan to Inner Mongolia, underscoring a strategic shift toward regions with better access to low-cost renewable energy. The move involves shutting equivalent capacity in Henan and commissioning new high-efficiency 600 kA cells at Dongshan Aluminium’s Chifeng facility by August 2026. Enabled under China’s capacity replacement framework, the relocation is expected to lower carbon intensity and support longer-term structural changes in the country’s aluminium production landscape.

Meanwhile, in Europe, the aluminium market is expected to see limited disruption in early 2026 despite the Carbon Border Adjustment Mechanism entering its definitive phase in January. Ample pre-cleared inventories, deferred cost pass-through, and seasonally weak demand are likely to keep Q1 relatively calm. From April 2026, however, the depletion of legacy stocks and direct pricing of CBAM costs are expected to tighten supply conditions and lift regional premiums, shifting market focus from LME prices toward carbon-adjusted sourcing and giving low-carbon producers greater pricing power.

Outlook

Domestic aluminium prices are expected to remain firm, supported by strong LME and MCX prices, declining global inventories, and continued upward price revisions by the primary producers. While downstream demand in India is likely to improve only gradually, global supply-side risks, tighter exchange stocks, and structurally higher premiums — especially linked to low-carbon supply — should limit any meaningful downside.

Leave a Reply