- Turkish buyers silent as rebar a drag on demand

- Indian buyers pause fresh bookings amid monsoon

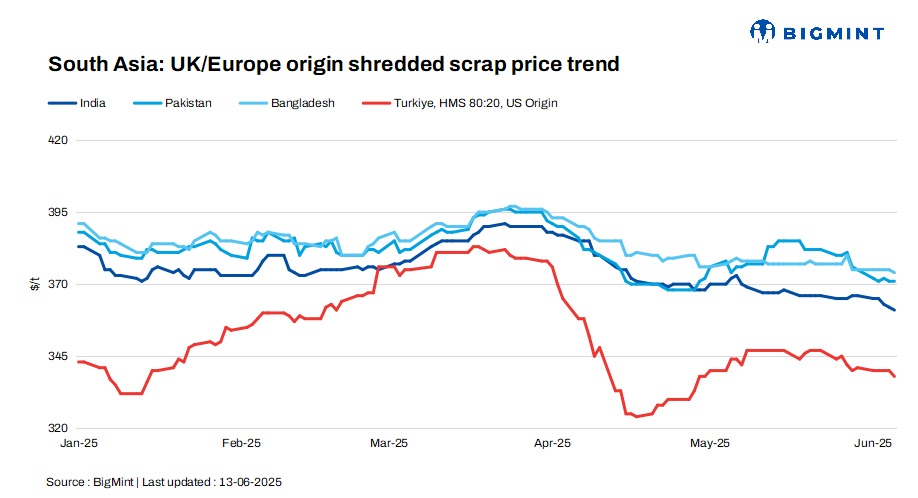

South Asia’s imported scrap market remained largely subdued this week, with activity slowing across India, Pakistan, and Bangladesh due to a mix of seasonal and economic pressures. In India, monsoon disruptions and weak construction demand dampened buying appetite, while Eid holidays and liquidity issues kept mills in Pakistan and Bangladesh on the sidelines. Turkiye also witnessed a quiet week, with buyers and sellers standing firm on price expectations amid weak downstream demand. Across all markets, limited trades, cautious sentiment, and a preference for cheaper domestic or alternative materials signalled a clear wait-and-watch approach as participants assessed market direction post-holidays and amid ongoing challenges.

Market overview

India: India’s imported scrap market remained quiet as weak construction demand and monsoon disruptions dampened buying interest.

Containerised shredded scrap was offered at $360-365/t CFR Nhava Sheva, but trades were scarce due to a wide bid-offer mismatch. Mills preferred cheaper domestic DRI and competitively priced Iranian HBI. African HMS 80:20 was available at $345-350/t CFR, though bids mostly stayed below $340/t CFR. Brazilian HMS 80:20 was offered at $330-333/t CFR and hand-loaded HMS stood at $360-365/t CFR, but even the higher quality material saw limited interest.

With falling steel prices and seasonal slowdown, buyers remained cautious, adopting a wait-and-watch stance and prioritising cost-effective alternatives.

Pakistan: Pakistan’s imported scrap market remained sluggish due to Eid holidays and weak domestic steel demand. Containerised shredded offers stood at $365-370/t CFR Port Qasim, but only limited trades were reported near $367-368/t as most mills avoided fresh bookings.

Bangladesh: Bangladesh’s imported scrap market stayed subdued amid Eid holidays, tight liquidity, and persistent LC issues. Shredded scrap offers hovered at $375-378/t CFR Chattogram, while HMS 80:20 was quoted at $355-360/t CFR, though no significant containerised bookings were reported. Activity in the ship recycling sector also remained limited, with only a handful of HKC-compliant yards operational.

Despite the slowdown, market participants remain cautiously optimistic, anticipating a revival in restocking once Eid celebrations conclude and monsoon-related hurdles start to recede.

Turkiye: Turkiye’s imported scrap market remained quiet, with prices stable as both buyers and sellers stayed cautious. US-origin bulk HMS 80:20 was assessed at $338/t CFR, with minimal trading interest. Mills showed reluctance to book July cargoes due to weak rebar demand and resisted paying higher prices.

A Baltic deal was heard at $337/t CFR, while an unconfirmed EU-origin booking was heard at $330/t CFR.

Sellers from the US and Europe held offers firm amid currency shifts and tight supply, keeping tradable values clustered around $336-345/t CFR. With limited activity, the market remained in a wait-and-watch mode.

Price assessments

India: UK-origin shredded indicatives were assessed at $361/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $371/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $374/t CFR Chattogram, down by $1/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $338/t CFR Turkiye, down by $2/t d-o-d.

Leave a Reply