- Indian buyers turn to more affordable alternatives

- Turkiye sees price gains on restocking optimism

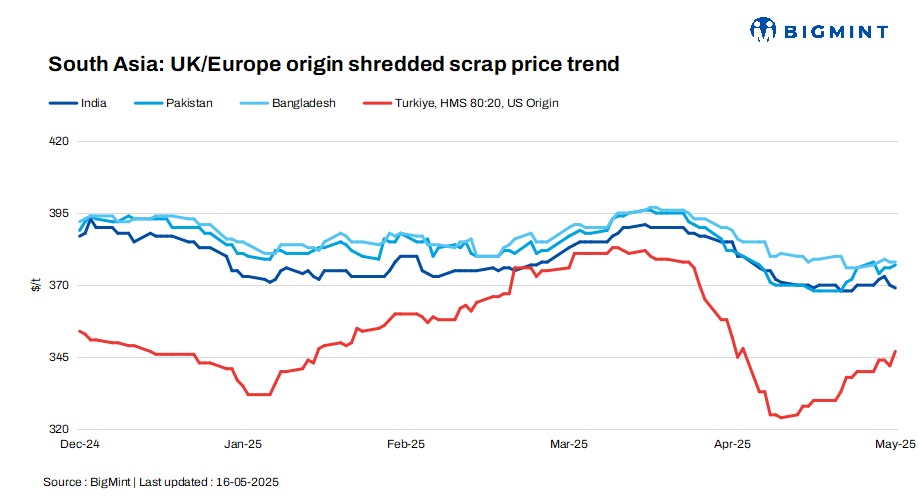

South Asia’s imported scrap markets presented a subdued picture, with India, Pakistan, and Bangladesh grappling with muted demand and cautious buying, though Turkiye saw renewed momentum.

In India, rising freights, weak domestic steel demand, and a shift towards alternative raw materials dampened scrap usage. Pakistan’s market stayed quiet as mills avoided bulk bookings ahead of Eid amid sluggish sales and adequate inventories. Bangladesh, too, remained under pressure due to the ongoing monsoon season and soft construction activity, despite no major letter of credit (LC) constraints.

In contrast, Turkiye showed signs of strength, buoyed by active mill restocking and optimism surrounding peace developments, pushing prices upward.

D-o-d, UK-origin shredded offers edged down by $1/t in India, inched up by $1/t in Pakistan, and remained stable in Bangladesh. US-origin bulk HMS 80:20 offers to Turkiye inched up by $5/t today.

Overview

India: India’s imported scrap market remained under pressure amid bearish sentiment driven by rising freight costs, weak domestic steel demand, and reduced material usage as buyers shifted towards more economical alternatives such as sponge iron and pellets. Despite some inquiries, most buyers remained hesitant amid unclear market direction and firm offers.

Shredded was offered at $365-375/t CFR Nhava Sheva, with bids at $360-365/t, while HMS 80:20 was quoted at $350-355/t CFR against bids at $345-350/t.

A trader commented, “We offered UK HMS at $350/t CFR Mundra but saw no firm interest; European turning at $335/t got only $325/t bids.”

Pakistan: Pakistan’s imported scrap market remained muted, weighed down by weak construction demand, sluggish steel sales, and tight rebar margins. Mills held off on fresh bookings due to sufficient inventories and an expected slowdown during Eid. Despite a slight uptick in global and Turkish prices, the local market sentiment stayed subdued.

Shredded offers from the UK, EU, and UAE were heard at $375-380/t CFR Port Qasim, but most buyers limited bids to $370-375/t, finding higher levels unworkable.

Bangladesh: Bangladesh’s imported scrap market remained sluggish, as the monsoon season and muted construction activity continued to weigh on demand. Mills showed little urgency for booking fresh cargoes, focusing instead on managing inventories amid subdued domestic steel sales.

Despite no major hurdles with LC openings, trade remained limited due to a persistent bid-offer gap. Australian shredded was offered at $375-380/t CFR Chattogram, while HMS 1 was heard at $360-365/t and HMS 80:20 at $350-355/t.

Sellers remained active, but cautious buyers held back, keeping overall market sentiment soft.

Turkiye: The Turkish imported scrap market strengthened, driven by robust restocking demand and a firm sell-side stance. Mills showed increased buying interest, with a US-origin deal reportedly concluded at $347/t CFR for HMS 80:20 and $367/t CFR for shredded and PNS scrap.

US-origin bulk HMS 80:20 offers were at $347/t CFR, up $5/t d-o-d. Sellers from the US and EU maintained firm offers at around $345-350/t CFR, with tradable levels mostly holding above $345/t.

Optimism also emerged around expected peace talks in Istanbul, further supporting bullish market sentiment and prompting expectations of continued demand from Turkish mills.

Price assessments

India: UK-origin shredded indicatives were assessed at $369/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $377/t CFR Qasim, up by $1/t d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $378/t CFR Chattogram, unchanged d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $347/t CFR Turkiye, up by $5/t d-o-d.

Leave a Reply