- Thermal coal inventories rise by over 5% w-o-w

- Sponge iron prices drop, weaken coal demand

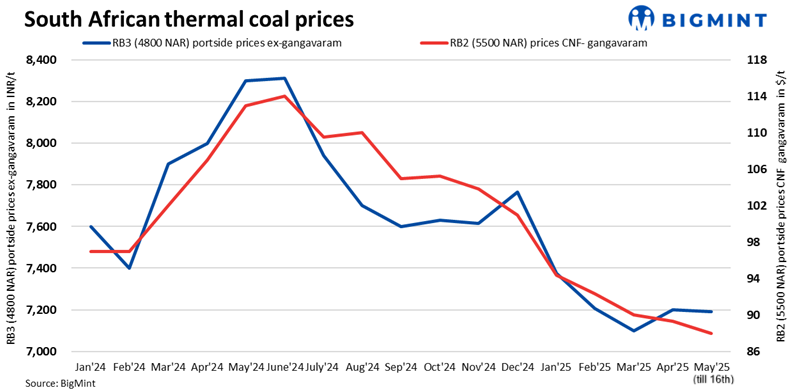

South African coal prices at Indian ports continued to weaken this week as demand stayed muted amid sufficient inventories and a soft index. As per BigMint’s latest assessment, RB2 (5500 NAR) fell by INR 50/t w-o-w to INR 8,250/t exw-Gangavaram, while RB3 (4800 NAR) declined by INR 50/t to INR 7,150/t.

Thermal coal inventories at Indian ports rose by over 5% to 15 million tonnes (mnt) in week 19 of CY’25, up from 14 mnt in the previous week.

Sponge iron prices under pressure

C-DRI prices dropped by INR 300/t w-o-w to INR 25,300/t from INR 25,600/t, while P-DRI ranged from INR 23,500–26,950/t across major markets. The decline was driven by limited participation, with buyers refraining from bulk purchases due to weak sentiment.

Export offers stable

South African RB2 export offers remained stable at $73.5/t FOB, while RB3 was unchanged at $61/t FOB as of 13 May.

Domestic coal prices fall w-o-w

Domestic coal prices edged down amid subdued demand and healthy supply. The 4500 GCV grade was assessed at INR 4,350/t, while the 5000 GCV grade stood at INR 4,800/t, exw-Bilaspur – both lower by INR 150/t w-o-w. SECL conducted two spot auctions on 6-7 May, allocating 784,350 t across six grades, with G11 comprising 52% of the total.

Outlook

While buyers are carrying sufficient stocks, as seen in the last 2-3 years of post-April stocking trends, the difference this year lies in the stable supply conditions. With weak demand and falling sponge iron prices, the South African coal market is likely to stay soft in the near term. Spot trades may only pick up towards the month-end if delivered costs decline or buying interest revives.

Leave a Reply