- Weakening rupee, Middle East conflict keep Indian buyers cautious

- Rising freights slow Turkish billet imports, limiting scrap alternatives

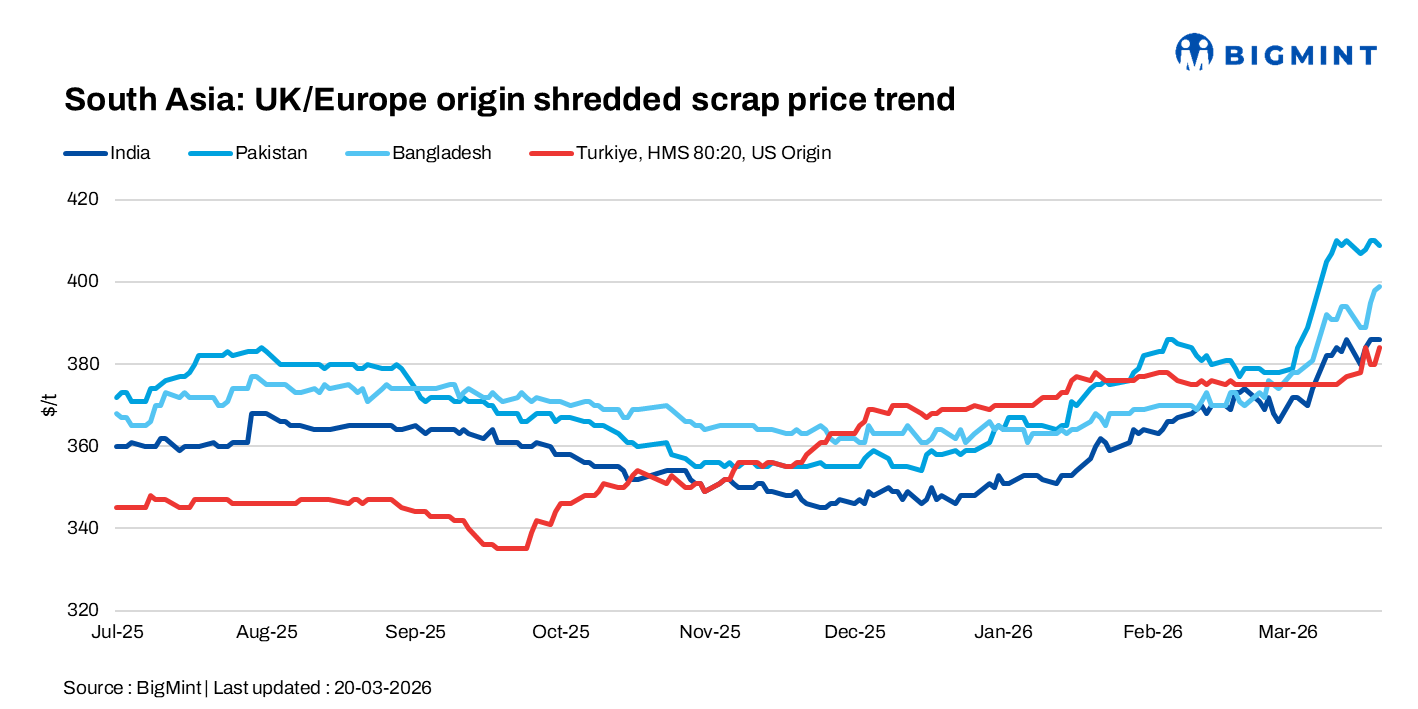

South Asia’s imported scrap markets remained cautious on 20 March. The Indian market was subdued as the rupee continued to depreciate, lifting landed costs of imports. Pakistan and Bangladesh markets also slowed as Eid arrived, Bangladesh under freight pressure, and Turkiye stable as rising costs supported sentiment but weak demand limited trading activity.

India: Imported scrap market sentiment in India remained stable d-o-d, with containerised shredded scrap prices largely unchanged on 20 March as buyers stayed cautious amid a weakening rupee and Middle East-related shipment concerns. Bids were heard at $365-367/t CFR Nhava Sheva, while tradable levels were indicated at $370-375/t.

Pakistan: UK-origin shredded was last heard near $410/t CFR Qasim, while overall sentiment remained weak with activity largely stalled amid ongoing Eid al-Fitr holidays. Trading is expected to normalise gradually in about a week.

Bangladesh: Imported scrap market sentiment in Bangladesh remained cautious, with mills keeping quotations open amid freight uncertainty. Higher shipping costs kept rates from Australia, Hong Kong, and Singapore firm. This pressured buyers, as finished steel prices remained comparatively weak, covering only basic margins. Hong Kong-origin PNS was heard at $405-410/t CFR Chattogram, with HMS (80:20) at $375-380/t. In the coming days, Eid al-Fitr holidays are expected to weigh on demand, limiting buying activity.

Turkiye: Deep-sea imported scrap prices in Turkiye firmed d-o-d on 20 March, with sentiment mixed as rising freight costs disrupted billet trade from China and Malaysia, limiting alternatives to scrap. Export rebar offers increased to $570-575/t FOB, with one deal heard at $570/t, while domestic levels stood at $575-585/t ex-works.

However, weak demand and tight margins, with break-even near $585/t, kept mills resisting scrap offers at $385-390/t (US) and $378-380/t (EU), resulting in limited deal activity. Further price direction will depend on mills’ ability to pass on higher costs to finished steel buyers.

Leave a Reply