- Higher freight costs raise landed scrap prices globally

- US scrap exports decline amid rising domestic demand

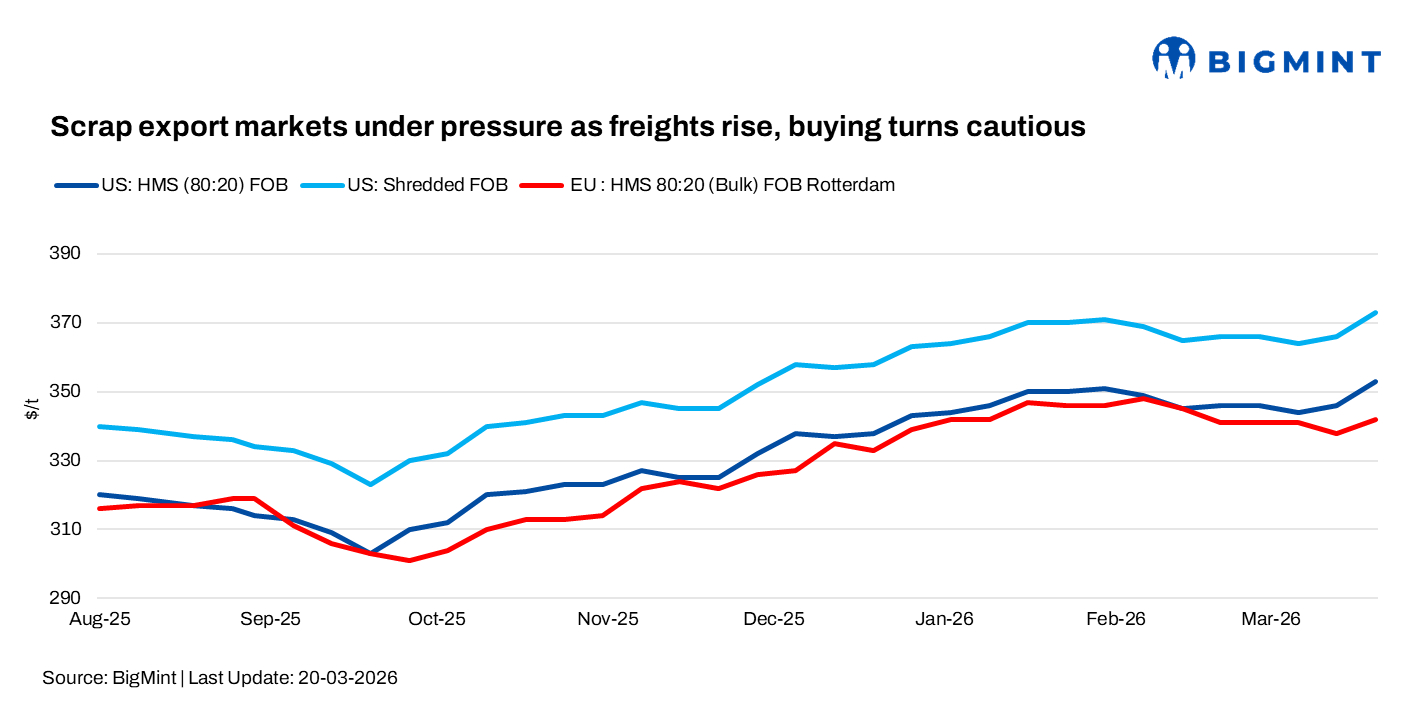

Global ferrous scrap export markets showed cautious sentiment during the week ending on 20 March, with prices largely stable across key regions. Weak export demand, rising freight and fuel costs, and uncertain downstream steel demand continued to influence trading activity, while most market participants adopted a wait-and-watch approach.

US

The US ferrous scrap market increased this week, supported by firmer sentiment from Turkiye amid rising freight rates. Export prices strengthened, with HMS 80:20 rising to $353/t from $346/t and shredded to $373/t from $368/t, although overall export activity remained limited.

With no major East Coast export sales reported, more material has remained in the domestic market, increasing availability. At the same time, improved weather conditions have boosted scrap flows, adding further supply-side pressure.

As a result, obsolete grades such as HMS and shredded are likely to face downward pressure in the April trade due to higher supply. In contrast, prime grades like busheling are expected to remain relatively firm, supported by tighter availability and steady mill demand.

Domestic prices remained largely stable, with busheling at $445-450/t DAP, shredded at $450/t, plate and structural at $430/t, and HMS near $400/t. However, higher bunker costs and weak export demand continue to weigh on overseas shipments.

Europe

The EU/UK scrap market remained stable to slightly firm this week, with domestic prices rising by Euro 5-10/t ($6-11/t) and standing at Euro 275-285/t ($317-329/t) supported by steady mill demand. However, export sentiment weakened amid softer import demand from Turkiye and sluggish finished steel markets. Scrap collection improved after winter, though overall generation remains below normal due to weak manufacturing activity.

FOB levels across regions are currently assessed around $310-320/t for shredded scrap and $270-290/t for HMS. Export activity remained limited despite buyer interest, as firm offers were scarce. A key factor has been the sharp rise in freight, with container costs increasing significantly, widening the spread between FOB and delivered prices and impacting trade viability. Freight rates have surged, with 20′ container costs rising from about $1,400/t to $2,100/t, increasing landed scrap prices.

For India, buying interest remained muted, with some volumes diverted towards Pakistan due to relatively stronger demand. Additionally, the current Eid al-Fitr holidays are expected to keep trading activity subdued over the next 7-8 days.

Brazil

Ferrous scrap prices remained stable this week as market participants assessed the impact of new federal tax rules introduced on 10 March. Negotiations stayed cautious with limited bids and offers. HMS 80:20 was assessed at BRL 848-850/t ($162-163/t) FOT, steel turnings at BRL 765-767/t ($147/t), and clean steel scrap at BRL 925-930/t ($177-178/t), all unchanged w-o-w.

Export prices were also steady, with HMS at $285/t FOB and shredded at $305/t FOB. Market sources said recyclers and steelmakers remain in a wait-and-see mode while evaluating how the revised tax structure will affect pricing and transaction flows.

Outlook

In the US, scrap prices are likely to remain under pressure due to weak export demand and rising domestic supply. In Europe, the market is expected to stay largely stable, with higher freight costs offsetting subdued buying interest. Mexico may see price consolidation with a slight downside bias, while Brazil’s market is likely to remain steady as participants assess the impact of new tax regulations.

Despite these regional variations, Turkish mills are expected to stay active in the import market, as limited domestic scrap availability continues to necessitate overseas procurement.

Leave a Reply