- Weakened rupee dampens Indian demand

- Weak construction sector affects Bangladesh market

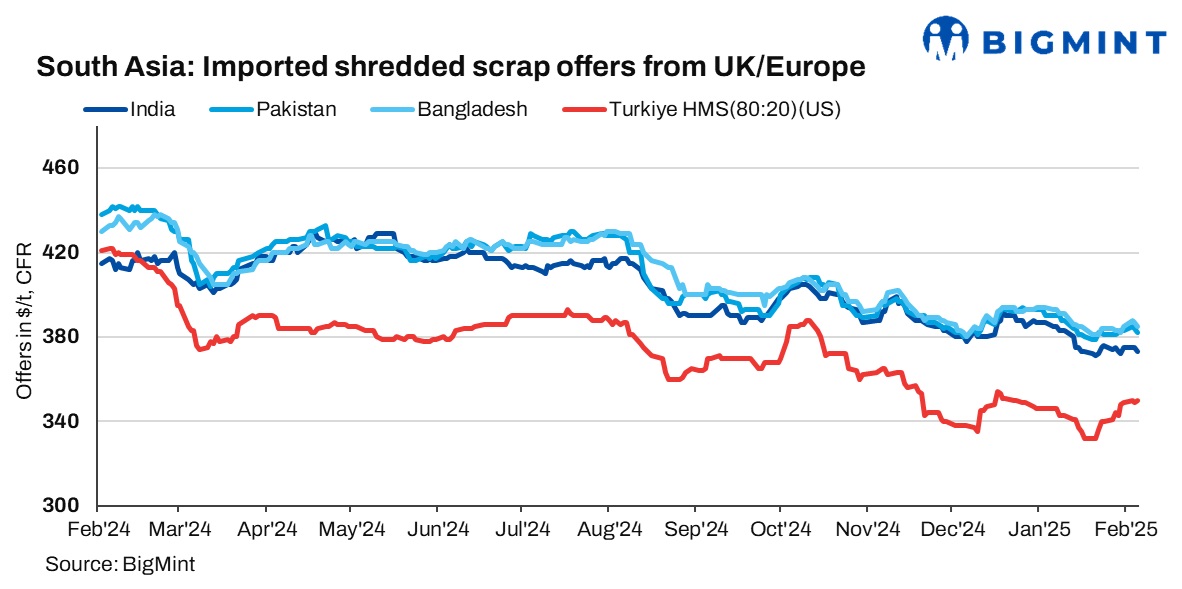

The South Asian imported scrap markets witnessed varied trends across countries, with sluggish demand and limited trade activity impacting prices. India’s market faced challenges due to a weakened rupee, making imports more expensive and dampening buyer sentiment. Pakistan’s market remained stable but slow, as weak construction demand and cash flow issues kept activity muted. Bangladesh saw reduced scrap purchases, driven by weak construction and falling rebar prices, while Turkiye’s market saw a slight uptick due to late bookings, though uncertainty prevailed amid geopolitical tensions.

Overview

India: India’s imported scrap market remained sluggish as the rupee weakened to 87 against the US dollar, dampening buyer sentiment and making imports costly. Shredded scrap was heard at $370-375/t CFR Nhava Sheva, with limited deals due to wide bid-offer gaps, while HMS (80:20) from the UK/Europe and West Africa was heard at $345-355/t CFR.

Suppliers preferred Pakistan for better prices, and strong US domestic demand restricted export offers. Traders believe a rupee recovery to 83-84 could boost deal activity.

Pakistan: Pakistan’s imported scrap market stayed stable but sluggish amid weak construction demand and cash flow constraints. UK-origin shredded was offered at $380-385/t CFR Qasim, with deals closing between $375-385/t, while UAE-origin HMS stood at $365/t CFR. Limited government projects and slow steel demand kept buyer interest low, though LC-backed mills maintained steady operations. Sellers faced pressure to offer discounts to sustain sales, and despite slight price upticks, the market outlook remains cautious.

Bangladesh: Bangladesh’s imported scrap market remained subdued due to weak construction activity and falling rebar prices, with major mills reducing rates by BDT 2,000 to BDT 88,000-89,000/t ex-Chattogram, while mills in Dhaka offered at BDT 80,000-85,000/t.

Import activity was limited, driven by need-based restocking ahead of Ramadan. Shredded scrap offers from Malaysia/Singapore are at $375-380/t CFR and PNS at $385/t CFR. Offers from Australia were at $375/t CFR for HMS (90:10) and $360/t CFR for HMS (80:20), though some LCs are still pending.

LC issues continue to restrict trade, while bulk shipments dominate over containers.

Local scrap prices stood at BDT 56,000-58,500/t for HMS and PNS, with shipyard scrap assessed at BDT 54,000-55,000/t. Mills are cautiously assessing offers, focusing on cost efficiency amid uncertain demand.

Turkiye: Turkiye’s imported scrap market saw a slight uptick as deep-sea scrap prices edged up, driven by late booking activity. US-origin bulk HMS (80:20) stood at $350/t CFR, up $1/t cents d-o-d. Confirmed deals included Baltic-origin HMS at $350/t CFR and UK-origin HMS at $345/t CFR, with bonus material at $365/t CFR.

Market sentiment remained cautious amid US-China trade tensions and uncertainty over Chinese billet offers post-Lunar New Year.

Traders reported limited activity, with mills hesitant due to high scrap costs and expectations of price corrections. EU recyclers faced rising collection costs, making competitive offers challenging despite a weaker euro.

Price assessments

India: UK-origin shredded indicatives were assessed at $373/t CFR Nhava Sheva, down by $2/t d-o-d.

Pakistan: UK-origin shredded indicatives were at $382/t CFR Qasim, down $2/t d-o-d.

Bangladesh: UK-origin shredded was assessed at $385/t CFR Chattogram, down by $2/t.

Turkiye: US-origin HMS (80:20) bulk scrap edged up by $1/t d-o-d to $350/t CFR Turkiye.

Leave a Reply