- India, Pakistan, UAE increase intake

- East Asian, European demand softens

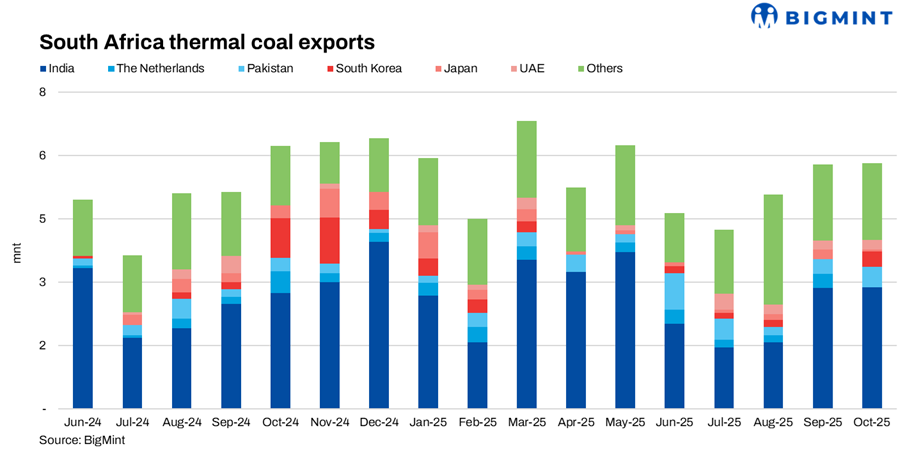

South Africa’s non-coking coal exports inched up 1% to 5.82 million tonnes (mnt) in October 2025 from 5.79 mnt in September. However, exports were down 7% from 6.23 mnt in October 2024. The slight monthly rise was led by continued firm demand from India, which remained the top importer.

South Asia sees mixed trends

India’s imports increased marginally to 2.89 mnt in October from 2.87 mnt in September, maintaining nearly 50% share of total exports. Pakistan’s intake rose to 0.48 mnt from 0.35 mnt, supported by stable industrial activity, while Bangladesh’s imports declined slightly to 0.12 mnt. UAE also saw a rise in imports to 0.23 mnt, reflecting consistent procurement by cement and power utilities.

East Asian imports decline

Japanese imports fell further to 0.05 mnt from 0.22 mnt, and Taiwan’s volumes declined to 0.17 mnt from 0.23 mnt, indicating softer demand from key Asian industrial buyers.

European demand softens

Shipments to Germany dropped sharply to 0.08 mnt in October from 0.24 mnt a month ago, while the Netherlands recorded no cargo movement after 0.32 mnt in September.

Market overview

In October, South African coal prices in India remained broadly steady, reflecting stable fundamentals and limited spot trading. On a CNF-India basis, RB2 averaged $86/t and RB3 $75/t, slightly below September levels of $87/t and $75.41/t, respectively. At Gangavaram, RB2 was assessed at INR 8,200/t and RB3 at INR 7,100/t, up marginally from INR 8,130/t and INR 7,043/t last month. Market sentiment stayed cautious, as Indian buyers maintained only need-based purchases while awaiting clarity on post-festive industrial demand and freight movement.

Outlook

South African non-coking coal exports are expected to stay firm through November, supported by consistent Indian demand amid moderate restocking and improving port activity after cyclone-related disruptions. However, weaker European buying and steady seaborne availability could keep prices range-bound in the near term, with buyers likely to remain selective in procurement.

Leave a Reply