- Higher sponge iron output in India boosts coal bookings

- Easing logistical bottlenecks support surge in shipments

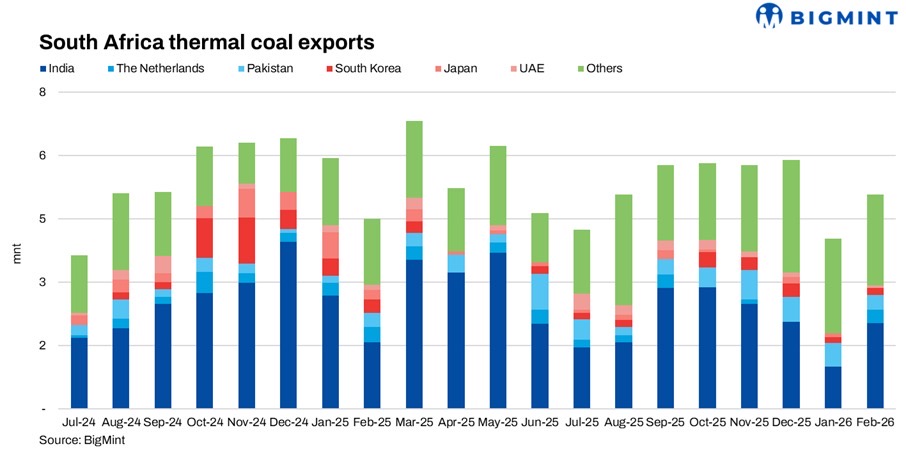

South African non-coking coal exports increased 26.3% m-o-m to 5.09 million tonnes (mnt) in February 2026 from 4.03 mnt in January. Volumes were higher by 13.1% y-o-y compared with 4.50 mnt in February 2025. The recovery in volumes indicates strong improvement after January’s 17-month low, primarily driven by a sharp rise in Indian demand.

Country-wise break-up

India emerged as the largest destination in February at 2.04 mnt, with shipments rising sharply by 102% m-o-m from 1.01 mnt in January and up 29% y-o-y from 1.58 mnt in February 2025.

Shipments to Pakistan declined to 0.34 mnt, down 39.3% m-o-m from 0.56 mnt and marginally higher by 3% y-o-y compared with 0.33 mnt last year.

South Korea imports stood at 0.17 mnt, increasing 21.4% m-o-m from 0.14 mnt, but down 63% y-o-y from 0.46 mnt.

Higher sponge iron output in India boosts coal bookings

On the demand side, India typically witnesses higher industrial activity in the last quarter of the financial year. Accordingly, sponge iron production increased from 5.2 mnt in December 2025 to 5.37 mnt in January 2026, prompting manufacturers to secure additional raw material. Anticipating this demand, buyers likely placed orders in December-January, when South African FOB RBCT levels were relatively stable around $76/t for RB2 (5,500 NAR) and $60-61/t for RB3 (4,800 NAR), making procurement viable despite cautious sentiment.

Sharp hike m-o-m follows low base due to seasonal constraints in Jan’26

The sharp rise in South African non-coking coal exports to India in February can be attributed to a mix of low base effect, seasonal demand recovery, and improved booking activity in prior months. January exports had dropped significantly due to Transnet’s logistics constraints, so February volumes (5.09 mnt) reflect both recovery and execution of delayed shipments.

Additionally, while Indian buyers remained selective during December due to weak downstream demand and elevated offers, domestic mid-CV coal availability tightened and auction participation strengthened. As sponge iron and industrial demand improved entering February, previously deferred purchases translated into higher imports. Improved vessel availability and easing logistical bottlenecks also supported shipment flows.

Overall, the February spike reflects a combination of restocking demand, seasonal consumption trends, and earlier booking decisions aligning with improved supply conditions.

Price overview

South African coal prices at Indian ports remained elevated throughout February, tracking firm export offers and tight grade-wise availability. Exw-Paradip 5,500 NAR increased to INR 9,700-10,600/t, while 4,800 NAR rose to INR 8,150-9,200/t. At Vizag, 5,500 NAR was reported up to INR 10,500/t and 4,800 NAR near INR 9,100/t.

FOB RBCT offers strengthened to $90-93/t, with CNF levels crossing $100/t, widening the gap between bid and offers. Availability remained constrained at key ports such as Gangavaram and Haldia, while inventories across grades stayed uneven despite overall stock movements.

Market activity remained limited and requirement-based, as buyers showed resistance to elevated prices and covered only near-term requirements amid pressure on downstream margins.

Outlook

Import demand is expected to moderate in March, as elevated prices and firm freight levels continue to weigh on buying interest. While improved South African export flows may ease supply concerns, high offers and cautious buyer sentiment are likely to keep trade subdued.

Leave a Reply