- Mill utilisation at 30%; liquidity constraints weigh on demand

- Post-Eid restocking, Chinese buyers’ return may lift sentiment

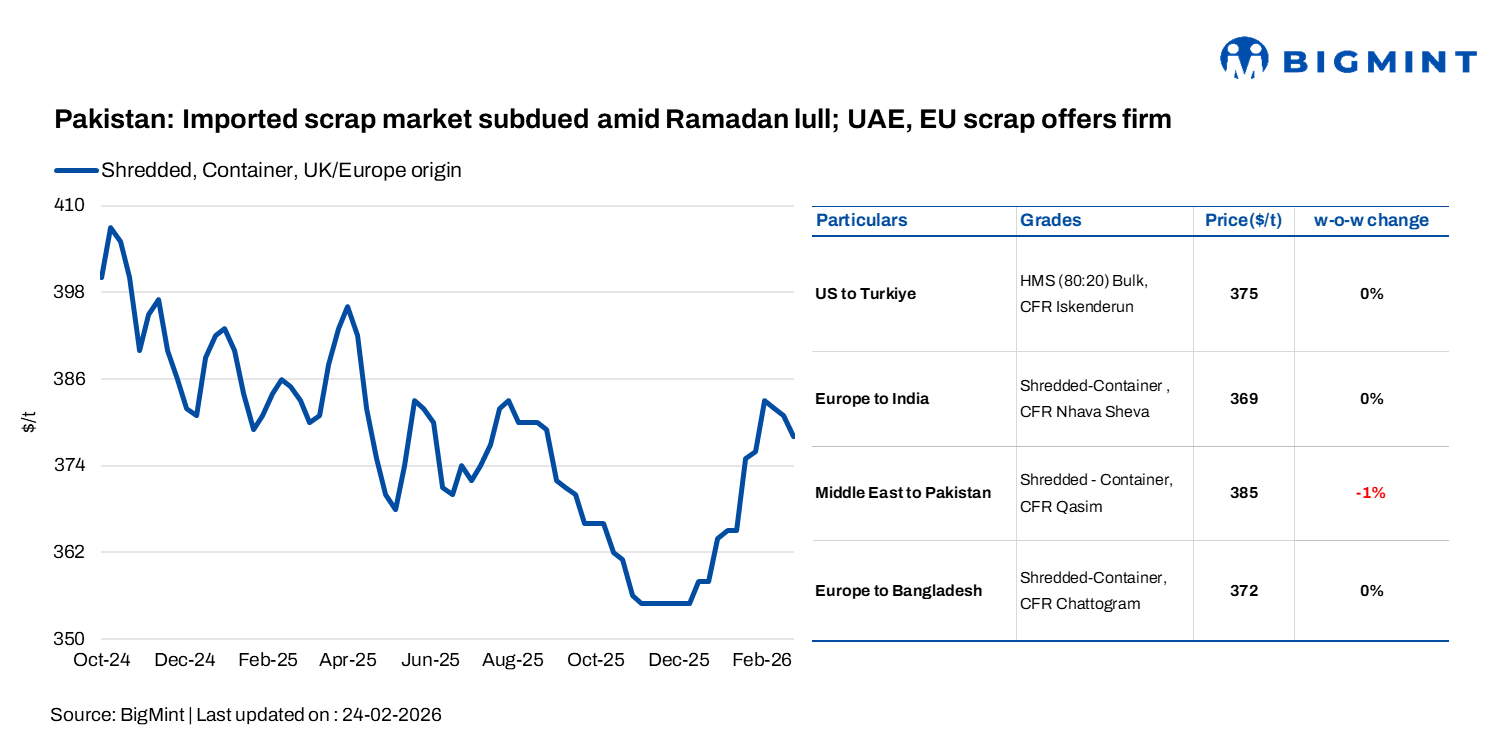

Pakistan’s imported ferrous scrap market remained largely inactive this week (18-24 February 2026), with sentiment at Port Qasim described as weak, and limited deals reported.

EU-origin shredded scrap was assessed at $378/t CFR Qasim on 24 February 2026, easing marginally by $3/t w-o-w. Buyers turned cautious after completing early-February restocking, while Ramadan-related slowdown and liquidity pressures further dampened trading activity.

UAE-origin shredded scrap offers were heard firm at $385/t CFR Qasim and above, while EU-origin shredded was quoted at around $380/t. However, buying indications were largely at $376-380/t throughout the week, reflecting cautious mill sentiment.

EU suppliers refrained from softening offers due to slow scrap collection rates across the region, which kept export availability tight. Meanwhile, in the UAE, Ramadan-led selective trading limited spot liquidity, but suppliers held offers firm.

Market comments

As per a major UAE-based trading house representative, UAE-origin shredded scrap was offered at $385-388/t CFR Qasim. Market sources reported shredded deals concluded at $375-378/t CFR throughout the week.

Fabrication scrap (loaded) was offered at $385/t CFR, while GI bundles were heard at $368/t CFR, both of UAE origin. UAE HMS was heard at $360-363/t CFR, down $6-8/t w-o-w.

According to a representative from a major global trading house, UK-origin shredded scrap is currently being offered at around $380/t CFR Qasim, but buyers are only willing to consider deals closer to $377/t. As a result, activity has remained muted. Traders also pointed out that UK-origin availability has tightened since Unimetal’s exit in the second half of 2025, with most volumes now moving directly to larger bulk buyers, leaving limited spot cargoes for smaller market participants.

According to a representative from a major global trading house, UK-origin shredded scrap is currently being offered at around $380/t CFR Qasim, but buyers are only willing to consider deals closer to $377/t. As a result, activity has remained muted. Traders also pointed out that UK-origin availability has tightened since Unimetal’s exit in the second half of 2025, with most volumes now moving directly to larger bulk buyers, leaving limited spot cargoes for smaller market participants.

Domestic market

Domestic scrap prices stood at PKR 136,000-138,000/t ($486-493/t). Rebar traded at PKR 225,000-226,000/t ($804-808/t), billets at PKR 195,000-196,000/t ($697-701/t), and Bala at PKR 185,000-188,000/t ($662-672/t).

Mill utilisation declined to 30% this week. A Karachi-based steelmaker noted, “Currently we are operating low, at 28-30% of our maximum capacity. We expect some revival in market activity by mid-March.”

Commercial-grade finished steel sales were stable but soft, with downward price negotiations, while graded products held firm. A Peshawar-based mill reported utilisation at around 30-32% with weak offtake.

Gadani ship-recycling: Despite Bangladesh regaining regional leadership, Gadani remained active, concluding several large bulkers with five vessels at anchorage. Steel plate prices held steady at $594/t, while the rupee strengthened against the dollar. Inflation and trade risks persist, but rising HKC certifications and steady arrivals are keeping market sentiment cautiously positive.

Outlook

Market activity during the current week is likely to remain subdued amid liquidity constraints, though post-Eid restocking and Chinese buyers (especially those based in Pakistan) returning from holidays may support a rebound next week. Proposed Chinese investments at Port Qasim, including shipbuilding and a steel mill project, could structurally boost Pakistan’s scrap and long steel market if materialised.

Leave a Reply