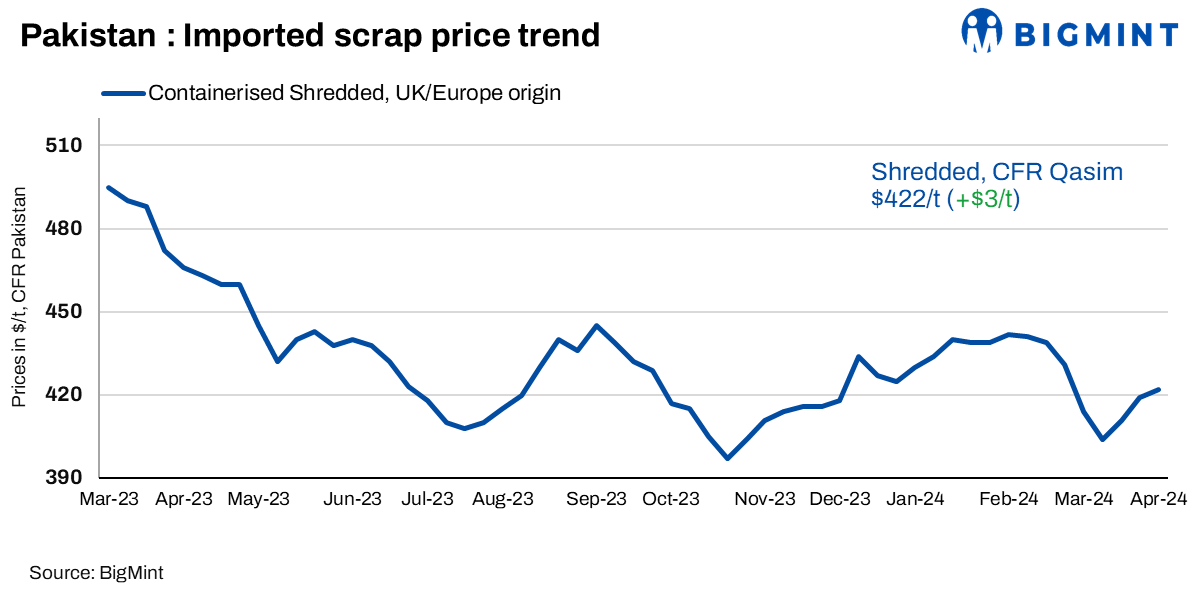

Imported ferrous scrap prices in Pakistan witnessed a slight uptick of $3/t compared to the previous week. This uptick is attributed to recent transactions at higher prices by Turkiye and firm offers from suppliers amidst decreased collection pace.

An official of a steel mill commented, “Pakistani buyers remained subdued amidst sluggish sentiment in the finished steel market, particularly during the upcoming Ramadan period. Several primary mills, such as Amreli, Naveena, Platinum, and Agha, are shut down, while others operate at reduced capacities of 30-40%. Additionally, fuel prices have surged, adding to market challenges.”

As per a major trading house from the UAE, inquiries from Pakistan are mostly at $415-418/t but recent offers of Pakistan remained higher than $425/t.

Notably, around 2,500-3,000 t of shredded scraps were heard to have been booked since last Tuesday from the UAE and Europe in the range of $418-420/t CFR Qasim.

Domestic market updates

In the domestic market, the demand for rebars has remained low towards the last week of March, majorly due to Ramadan observations. Rebar prices were reported at around PKR 254,000-256,000/t($914-921/t), with scrap at PKR 158,000-160,000/t($569-576/t) and billet at PKR 220,000-222,000/t($792-799/t). Production costs continued to rise due to high electricity and fuel tariffs.

An official representing a steel mill acknowledged, “Our mill has initiated maintenance activities, with operations set to resume on 15 April . As part of the maintenance, production will be halved, reducing output from approximately 12,000 tonnes (t) to 6,000 t. Additionally, impending Eid holidays add to the temporary slowdown. Slow payments further contributed to the subdued atmosphere in the market. Overall, the current state of affairs reflected a dull market scenario characterised by reduced production, holiday disruptions, and delayed payments.”

The World Bank projects Pakistan’s GDP growth at 1.8% for the current fiscal year due to subdued economic activity fuelled by persistent trade deficits and limited external financing. Inflation is expected to remain high at 26% in FY24, driven by increased domestic energy prices. The current account deficit is forecasted to remain low at 0.7% of GDP, but risks persist from heavy domestic borrowing and policy uncertainties. Urgent reforms are necessary for state-owned enterprises to mitigate fiscal risks. Despite averting an economic crisis with the IMF program in July 2023, Pakistan’s recovery has not sufficiently addressed poverty, with around 10 million people at risk of falling below the poverty line. Rising food prices disproportionately affect poor households, worsening inflation and inequality.

Outlook: Steel mills may continue to operate at reduced capacities, averaging between 30% to 40%. Insider’s demand analysis suggests a potential improvement can only be seen post-June 2024. However, with the upcoming holidays, market activity is expected to further decline, with prospects for short-term improvement anticipated after Eid.