- Portside stocks at Kandla and Tuna decline

- Weekly retail lifting volumes average over 107,000 t

More than 3.1 million tonnes (mnt) of US Northern Appalachian (NAPP) and Illinois Basin (ILB) coal are currently floating toward Indian ports, according to vessel manifests as of late April 2026. The incoming supply wave coincides with a third consecutive week of portside stock drawdowns at key west coast hubs, as retail lifting volumes remain robust and cement manufacturers accelerate fuel substitution away from costly petroleum coke (petcoke).

US coal supply pipeline and retail inventory trends

US NAPP coal (6,900-7,100 kcal/kg NAR) continues to arrive in India in substantial volumes. As of late April 2026, over 3.1 mnt of US-origin thermal coal were either at anchor or en route to Indian discharge ports. This volume is split between the retail segment (approximately 1.44 mnt) and the industrial segment (over 1.64 mnt), with arrivals scheduled through mid-June 2026.

Key discharge ports include Tuna (near Mundra) and Kandla on the west coast, as well as Gangavaram, Dhamra, Paradip, Dahej, Kakinada, and Karikal on the east and south coasts.

Portside inventory trends: At the key west coast hubs of Kandla and Tuna, combined stocks of US NAPP coal stood at 314,037 tonnes as of April 27, 2026. This marks the third consecutive week of stock drawdowns, following inventory levels of 362,024 tonnes on April 20 and 404,942 tonnes on April 13.

Retail lifting volumes: Weekly retail lifting has remained robust over the past three weeks. In the week ended April 27, retail lifting totalled 98,051 tonnes. The week ended April 20 recorded lifting of 120,704 tonnes, while the week ended April 13 recorded lifting of 103,252 tonnes. The three-week average lifting stands at approximately 107,300 tonnes per week, indicating sustained physical offtake from portside warehouses.

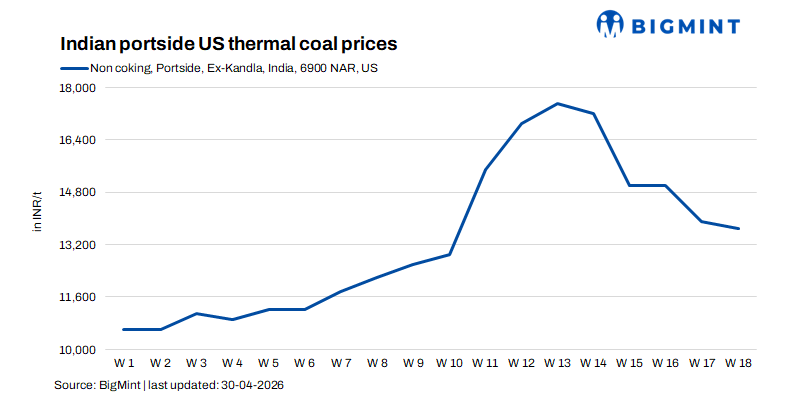

On pricing, FOB Baltimore 6,900 NAR coal was quoted at about $93-94/t, while CFR India West $138/t (with current freight from Baltimore to WCI at ~$43-44/t). Market sources indicated that US NAPP coal was being offered to Indian cement plants at an estimated $135-140/t CFR India for spot bookings in the week ended April 27. However, the cement companies are holding out for lower prices. Recently in a tender a cement company on West Coast received offers as low as $133/t CFR but did not conclude as it was holding out for prices to reach $130/t

Competing petcoke loses ground to US coal

The driver of sustained retail lifting and industrial interest in US NAPP coal is the widening price disadvantage of its primary competing fuel: petroleum coke. CFR India 6.5% sulphur petcoke was assessed at $158/t on April 15. On a heat-adjusted basis, CFR Turkey 6.5% sulphur petcoke traded at a 12% premium to delivered coal in mid-April, a sharp reversal from the 22% discount average seen in the same period of 2024.

A market participant noted that cement producers had increasingly shifted toward thermal coal procurement recently as petcoke premiums had become unsustainable.

Indian cement makers, the largest end-users of imported fuels, have responded by sharply reducing petcoke intake. This reduction in petcoke demand has directly benefited US NAPP coal. Cement plants have reconfigured their fuel mix calculations, and at a sustained delivered price of $135-140/t CFR, US NAPP has become the marginal fuel of choice for the sector.

Retail traders have also played a significant role in absorbing incoming volumes. The consistent lifting activity at Kandla and Tuna – averaging over 107,000 tonnes per week over the past three weeks – indicates that smaller buyers and traders are actively replenishing inventories despite firm offer levels.

A trading source noted that buyers had forward visibility on US NAPP arrivals through June, which allowed them to plan purchases but also to resist aggressive spot offers from sellers holding high-cost inventory.

Supply overhang and monsoon outlook

Looking ahead to May and June, US NAPP coal faces a supply-side test. The incoming vessel wave of over 3.1 mnt is expected to significantly boost portside availability. Should retail offtake and industrial demand fail to keep pace – particularly as cement plants may begin destocking ahead of monsoon rains, which typically hamper construction activity on the west coast from June – spot prices for US NAPP could face downward pressure.

However, the floor for US NAPP prices remains supported by petcoke dynamics. Unless petcoke prices correct substantially, US NAPP will likely retain its marginal fuel advantage. A trader source noted that cement producers would continue favoring US thermal coal as long as delivered NAPP prices remained below $145/t CFR and petcoke held above $155/t.

On the cement demand side, the outlook remains robust, supporting sustained US NAPP consumption. Industry data indicates that cement production volumes in the financial year ending March 2026 grew 8.6% to 491.4 mnt, with forecasts of 7-8% growth in the current fiscal year supported by housing and infrastructure spending.

US NAPP coal has established a commanding presence in India’s fuel market, with over 3.1 mnt en route – the largest inbound volume in recent months – and portside stocks drawing down for three consecutive weeks. Retail lifting volumes remain healthy, averaging over 107,000 tonnes per week, and cement manufacturers continue to favor US coal over costly petcoke. The transatlantic trade link is set to sustain through the monsoon season, reinforced by competitive delivered pricing and sustained industrial offtake.

Leave a Reply