- China’s low-CV thermal coal prices rise amid tightening supply

- Market remains uncertain; demand and supply both weak

Mysteel Global: Chinese spot thermal coal market faces ongoing uncertainty as both bearish and bullish factors continue to interplay. However, neither side has gained enough momentum to dominate, resulting in diverging views on the market direction.

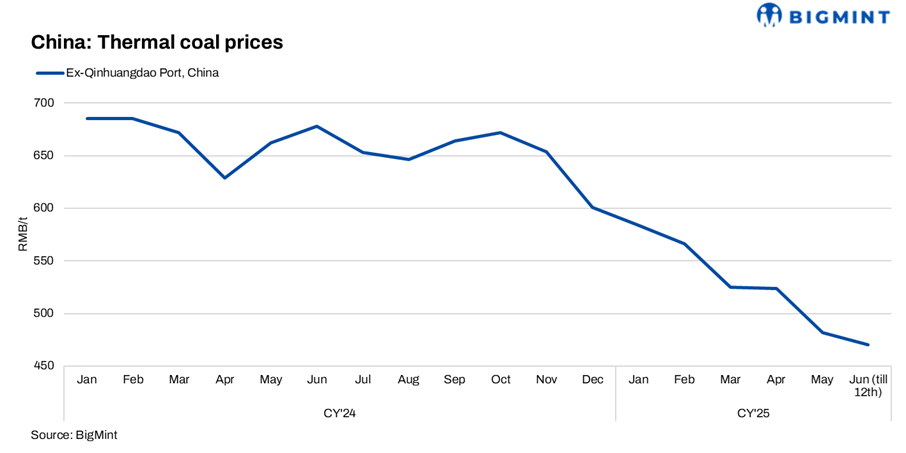

On Wednesday, Mysteel’s assessment of 4,500 kcal/kg NAR thermal coal gained Yuan 1/tonne ($0.14/t) on day to reach Yuan 472/t, FOB northern ports and including 13% VAT. This marked the second consecutive day of gains for the low-calorific value (CV) grade. By contrast, prices for 5,000 kcal/kg and 5,500 kcal/kg NAR grades stayed unchanged on day at Yuan 534/t and Yuan 617/t, respectively.

The rationale for the rise in low-CV coal prices lies in the fact that supply of this grade has become increasingly tight, while demand has slightly ratcheted up, prompting sellers to adopt a firmer pricing stance, Mysteel Global has learned.

The tightening supply came on the back of a decline in the rail coal inflows from producing hubs, as shipping coal to northern ports has been financially unaffordable for most independent sellers, even though they could enjoy a rail freight discount of up to Yuan 30/t depending on the rail volume.

A seller at northern ports said that his all-in cost for 5,000 kcal/kg NAR coal originating from Shanxi, North China, stood at over Yuan 560/t, roughly Yuan 30/t above prevailing spot prices, forcing him to scale back inbound shipments despite the incentive of volume-based freight discount.

Amid the reduced rail shipments, coal stockpiles at northern ports continued to fall. On Wednesday, the eight northern ports monitored by Mysteel held 27 million tonnes in inventory, down 0.3% from the previous day, extending a destocking trend that began in mid-May.

The inventory drawdown, regarded as evidence of easing long-standing oversupply, has bolstered market sentiment. Some participants believe this could encourage buyers to step up proactive procurement ahead of the July-August peak demand season.

However, by far, the demand hasn’t improved substantially, contributing to a market pattern where demand and supply of the fuel both stayed weak.

Yesterday, some power utilities closed tenders for late June deliveries of domestic coal, with prices submitted by traders lower than the current prevailing prices. For example, a trader said his bid for 5,500 kcal/kg NAR was at a price that net back to Yuan 610/t FOB northern ports, suggesting an increasingly bearish outlook on the market.

“Coastal power plants’ coal consumption remains limited and is creeping up slowly since renewables have crowded out coal-fired generation,” said a South China-based trader. “Additionally, the rainy season in South China dampens household air-conditioning demand.”

As of Wednesday, China’s six major coastal power groups held stocks worth 19 days’ generation on average, hinting at ample inventories that allow them not to restock immediately.

Looking ahead, participants said they will continue to monitor the pace of inventory drawdown at northern ports and the weather conditions across South and East China, which remain key indicators for gauging the market direction.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply