- Demand growth after 2015 disaster did not meet expectations

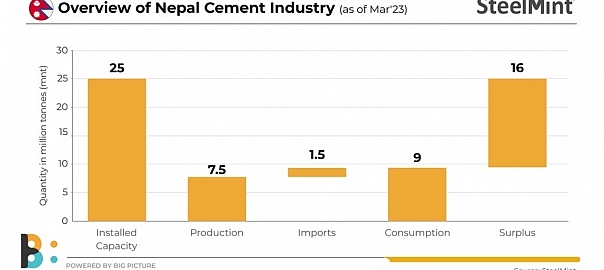

- Cement supply 3 times higher than demand

- Firm and industry-friendly govt policies required

- Export opportunities can make up for losses of cement makers

Cement sector is one of the major contributors in the growth story of Nepalese industry. It is also said to be playing a pivotal role in the future development of the economy.

However, the present scenario is such that this industry is facing several issues and among them, the key one is the demand-supply imbalance.

After the 2015 earthquake in Nepal, several cement manufacturing units were established in anticipation that demand will be boosted in the reconstruction works. However, contrarily, not much happened in terms of demand growth.

Currently, there are around 65 cement manufacturing plants (24 clinker and 41 grinding plants) in the Himalayan nation with a current installed capacity of 25 million tonnes (mnt) per year whereas consumption is just 10 mnt/year. The per capita cement consumption is around 300 kg/year.

“The Nepalese cement industry has become self-sufficient in catering to domestic demand. In fact, supply is three times higher than its demand in the country,” said Rajesh Agrawal, Managing Director, Arghakhachi Cement, during his presentation at SteelMint Events’ 2nd Nepal Trade Summit 2023, held in Kathmandu on 1-2 March.

Government support much needed to push demand

Dhruba Thapa, President, Cement Manufacturers Association (CMA), said “There is lack of a firm government policy for the cement industry.”

Emphasising on the government’s role in the growth of this industry, he further said that a firm and rigid long-term policy and infrastructure development projects to boost cement demand in the country would help manufacturers to deal with their losses.

He also talked about the national single window system, launched in 2021, that is yet to be implemented. This is a web interface that facilitates official procedures for imports and exports through an online system and helps make information available on a harmonised code system on various products and tax-related issues.

Export opportunities to benefit cement makers

Due to supply exceeding demand, there is a pressing need to find new export markets for selling the surplus cement of around 15 mnt.

Domestic producers have started exporting cement from last year (2022) which is a positive and supporting factor for this industry.

The Nepalese cement makers are finding the southern neighbour, India, as a potential market for exports given its geographical proximity. Other potential markets are China and Bangladesh.

“Currently, the government is providing 8% cash incentive for exports if the minimum export volume is worth NPR 500 million per annum per unit. This incentive makes it feasible to export cement and clinker to the Indian market despite high production costs,” Agrawal said in his presentation.

LC3 – a better option

Limestone calcined clay cement (LC3) is a new variant that is based on a blend of limestone and calcined clay. LC3 can reduce carbon dioxide (CO2) emissions by up to 40%. This is cost effective and does not require capital-intensive modifications to existing cement plants,Agrawal said.

He also emphasised on the advantages of switching to LC3 in Nepal. According to him, producing LC3 will reduce imports worth over a billion. This will further help in reducing trade deficit.

As Nepal does not have any primary source of slag (primary steel plant) and fly ash (thermal plant) production (or byproduct), it is easier to move towards production of LC3, he suggested.

Way ahead

“If cement producers could get more opportunities to export and the government would support this industry with new initiatives to boost demand, the per capita cement consumption would likely increase to 450-600 kg by 2025,” said Rajesh Agrawal while giving an outlook on the Nepalese cement industry.

Nevertheless, the cement players are positive about the industry’s future in the medium to long term.

Leave a Reply