- Middle East conflict disrupts supply routes, pushing global pet coke prices higher

- Buyers pause purchases as market volatility and supply uncertainty intensify

The global petroleum coke market has entered a period of disruption following the outbreak of war between the US/Israel and Iran. The conflict has quickly changed market sentiment and pushed prices higher across several regions. Market participants say uncertainty over supply, rising freight costs and stronger crude prices have combined to create a sudden shock across the petroleum coke trade.

One of the main concerns is supply from the Middle East. Major exporters such as Saudi Arabia and Oman regularly ship large volumes of petroleum coke to Asian markets. However, the Strait of Hormuz has become a high-risk shipping route because of the conflict. This has made it more difficult for vessels to move cargoes from Gulf refineries to buyers in India and China. As a result, traders and buyers are increasingly concerned about the reliability of supply from the region.

Freight costs have also increased sharply. Shipowners are demanding higher war-risk premiums, while bunker fuel prices have risen alongside crude oil. Some vessel operators are also avoiding the Gulf region because of security risks. Freight from the US Gulf to India has climbed to around $53–54 per tonne, significantly increasing the delivered cost of petroleum coke cargoes into Asia.

Crude oil prices have strengthened since the conflict began. Because petroleum coke is produced as a by-product of refining heavy crude, higher crude prices increase refinery feedstock costs and raise the overall price floor for petroleum coke. These factors have created a volatile market environment where sellers are cautious about offering cargoes and buyers are hesitant to commit to purchases.

US refiners gain stronger market position

Refiners in the US Gulf Coast are currently in a strong position as supply from other regions becomes uncertain. High-sulphur petroleum coke exported from the US Gulf has recently traded around $89–94 per tonne FOB. Cargoes with lower sulphur content and higher calorific value typically command higher prices depending on quality.

Recent February market data shows Gulf Coast green coke prices across several quality ranges. Material with above 50 HGI has traded between $80 and $94 per tonne, while coke below 50 HGI has traded between $79 and $92 per tonne. Cargoes containing around 4.5% sulphur have traded between $88 and $94 per tonne, while higher sulphur material above 6% has been heard between $79 and $85 per tonne.

The market for calciner feedstock has also strengthened. The March PACE index for Gulf Coast calciner feedstock is around $195 per tonne. This compares with about $164 per tonne in the third quarter of 2025 and roughly $131 per tonne in early 2025, highlighting strong demand for higher-quality feedstock used in calcining.

Despite rising prices, many US refiners are reluctant to lock in cargo sales at fixed levels. Many petroleum coke contracts are linked to monthly index pricing, and producers worry that early sales could look too low if the market continues to rise.

Petroleum coke price overview by grade and region

Low-sulphur and calcined coke markets remain firm

Low-sulphur petroleum coke markets have also shown firm pricing. On the US West Coast, cargoes containing more than 2% sulphur have recently traded between $88 and $144 per tonne, while material with sulphur levels below 2% has traded between $138 and $149 per tonne.

Anode-grade calcined petroleum coke markets remain supported as well. Demand from the aluminium sector and limited availability of suitable feedstock continue to support these markets in both the US and Europe.

Indian prices rise sharply as freight increases

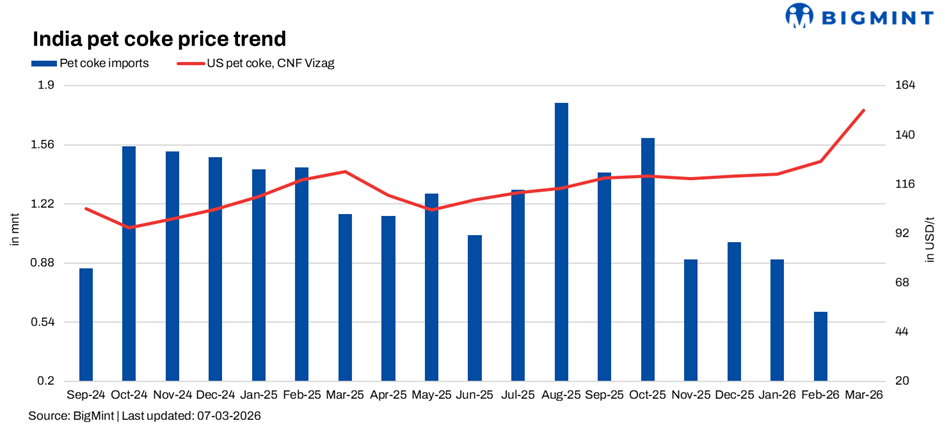

India has seen the most visible price increase in recent days. On February 27, offers for imported petroleum coke were generally heard between $124 and $130 per tonne CNF India.

By March 6, prices had risen sharply as freight costs and supply concerns intensified. Market indications now place US cargoes delivered to India’s east coast between $145 and $150 per tonne CNF, with some offers heard around $148 per tonne and higher indications between $152 and $155 per tonne.

At these levels many cement producers have paused purchases as they assess how long the price increase may last.

Market outlook

The direction of the petroleum coke market will depend largely on how the conflict in the Middle East develops. If shipping through the Strait of Hormuz remains restricted, freight costs are likely to stay elevated and Middle Eastern exports could remain limited. In that case, prices for seaborne petroleum coke may continue rising as buyers compete for available cargoes from the United States and other suppliers.

If shipping risks ease and freight rates fall, prices could stabilise as supply flows gradually return to normal. For now, the market focus has shifted from finding the lowest price to securing reliable supply, with sellers cautious, traders managing risk and buyers waiting for clearer signals before returning to the market.

Leave a Reply