Met coal, PCI markets stalled amid weak demand and oversupply

Met coke holds firm on tight supply despite overall bearish sentiment

The international metallurgical coal, coke, and Pulverized Coal Injection (PCI) markets entered a state of suspended animation in the week ending April 10, caught between a fragile geopolitical ceasefire, a pronounced lack of demand from major steel-producing nations, and a persistent overhang of unsold cargoes.

Premium hard coking coal at a standstill

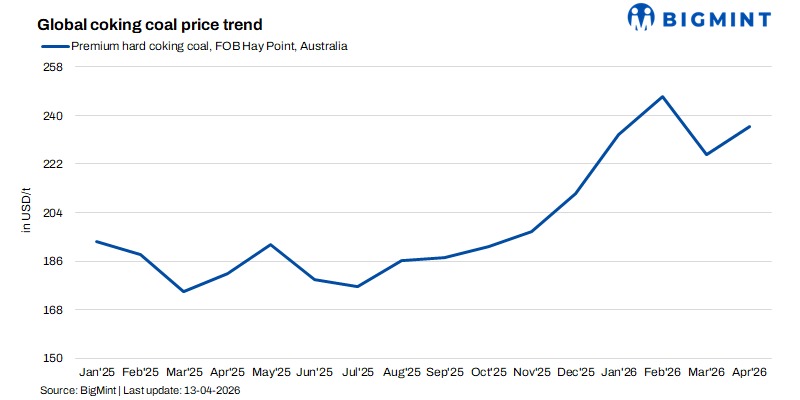

The premium hard coking coal (HCC) market effectively ground to a halt. After weeks of volatility driven by supply concerns, the narrative pivoted sharply to bearish fundamentals. Sources described a “stalemate situation” in which there was no sell-side pressure, a complete absence of firm offers, and buying interest that had all but evaporated.

India, a key demand driver, was conspicuously absent. End-users there adopted a wait-and-see mode, watching freight rates and the FOB Australia index trend downward. One Indian steelmaker suggested a fair market value for premium coal was significantly below prevailing offers, indicating a wide gap between buyer and seller expectations.

Sentiment soured further following a two-week ceasefire between the US and Iran announced April 8. The news removed much of the geopolitical risk premium that had supported prices, turning the market more bearish overnight. Traders reported that multiple April and May loading cargoes remained unsold, yet no buyers were willing to step in.

Low-vol HCC and PCI under pressure

Weakness extended down the quality curve. Low-volatile HCC prices fell further, weighed down by an oversupply of cargoes and limited demand from China, where the Dalian Commodity Exchange had fallen sharply. Tradable levels for May-loading cargoes edged lower across the board.

The PCI market was similarly sluggish. A deal for Russian-origin Mid-Tier PCI was heard at a significant discount, though even at those levels, buying interest remained tepid. Sellers noted that Chinese buyers, in particular, had lost confidence in bidding for seaborne cargoes amid falling domestic steel margins.

Atlantic market disconnect

In the Atlantic basin, a sharp disconnect emerged between buyers and sellers. Official assessments for US low-volatile HCC held steady, but buyers pointed to trades for discounted, off-specification cargoes at much lower levels as the “true market”. Producers of benchmark coals dismissed these views as “buyer talk”, creating a standoff that kept transaction volumes minimal.

Met coke finds support

In a contrasting trend, the met coke market showed resilience, supported by tightening Indonesian supply. Suppliers raised offers for June-loading cargoes due to higher input costs and limited availability. As Indonesian supply tightened, some demand shifted toward Chinese coke, which edged higher on improved buying interest, including inquiries from Turkey. However, some Indian end-users described current prices as “elevated” and chose to wait.

Steel industry weakness

The primary driver of demand-side malaise is deteriorating steel mill profitability, particularly in China. Mill margins showed signs of weakening, prompting many mills to pivot toward lower-grade iron ore and cheaper alternatives, directly reducing appetite for premium coking coal and PCI. In India, domestic rebar prices fell, and buyers remained reluctant to secure expensive imported coal. Turkish rebar activity remained muted amid a lull in demand.

Outlook

Looking forward, the met coal, coke, and PCI markets face a challenging near term. The immediate outlook is for continued price weakness, as the overhang of unsold April and May-loading cargoes will take time to clear. Without a significant catalyst-such as a sharp rebound in Chinese steel margins or a sudden supply disruption-buyers are expected to remain on the sidelines.

The ceasefire, if it holds, will likely allow freight rates to normalise further, removing another layer of support for delivered prices. However, any renewed escalation in the Middle East could quickly reverse this dynamic, reintroducing risk premiums. Indian demand may pick up in the next 15 to 30 days as inventories draw down, but this recovery is expected to be gradual and price-sensitive.

Longer-term, the market will depend heavily on Chinese steel export performance and the pace of global industrial activity. For now, the most probable scenario is one of rangebound trading with a downside bias, as sellers compete to offload cargoes and buyers hold out for lower entry points. Met coke may remain the outperformer given supply constraints, but it is not immune to the broader bearish sentiment.

Leave a Reply