Petroleum coke prices showed a mixed but generally firm trend during the transition from December 2025 into early January 2026. U.S. export prices strengthened, particularly for premium low-sulfur grades, while some key import markets saw modest softening or stability.

- U.S. Gulf Coast (USGC): FOB prices for 4.5% sulfur material rose to around $79-80/metric ton, while 6.5% sulfur material reached $72-74/mt.

- U.S. West Coast (USWC): Low-sulfur (2.0% S) coke saw a sharp jump, climbing to around $140-158/mt, marking a nine-month high.

Import Markets

- Turkey: CFR prices held relatively steady near $103-108/mt.

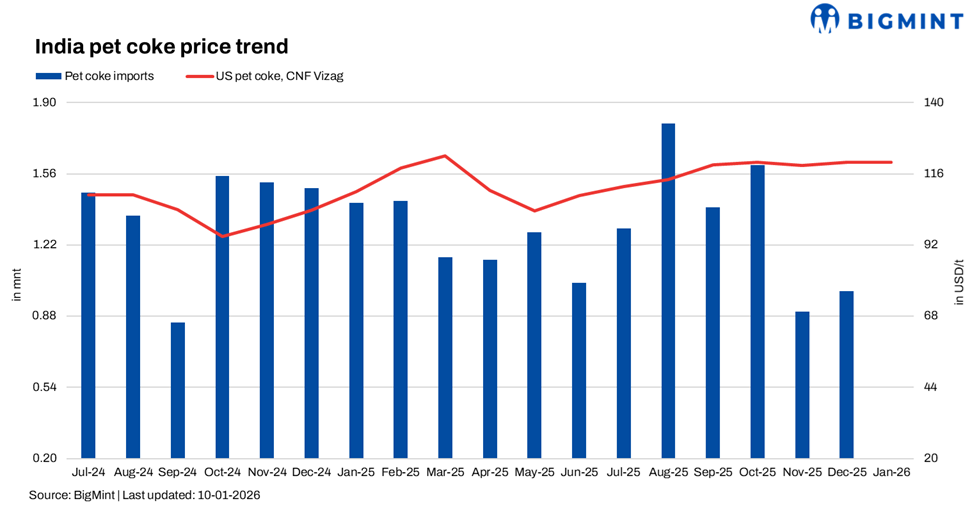

- India: CFR 6.5% sulfur coke eased slightly to $111-117/mt.

- China: Prices diverged-high-sulfur grades softened, while low-sulfur grades gained $10/mt or more.

Underlying Market Factors

Several regional and global factors drove these movements:

- Lower Freight Rates: A significant drop in dry bulk shipping costs from the U.S. to key destinations like India and Turkey allowed U.S. producers to raise FOB prices while keeping delivered costs stable or even lower for buyers.

- Strong Chinese Pre-Holiday Demand: Ahead of the Lunar New Year, Chinese buyers showed strong interest in low-sulfur pet coke, pulling up U.S. West Coast offers and reducing sellers’ willingness to discount material for other markets.

- Geopolitical Tension: A U.S. military operation in Venezuela-a major coke exporter-in early January introduced supply uncertainty. While near-term trade flows were not immediately disrupted, the event supported sentiment for U.S. origin material.

Regional Demand Patterns

- Atlantic Basin: Many European and Turkish buyers remained on the sidelines after year-end holidays, waiting for clearer price direction before securing Q1 volumes.

- India: Construction activity began to recover post-holidays, but competitively priced high-calorific thermal coal limited pet coke’s price upside. Domestic Indian refiners raised offers in anticipation of stronger quarterly demand.

- Weather Disruptions: Heavy rains and port delays in Australia’s coal export terminals tightened global solid fuel supply sentiment, indirectly supporting alternative fuels like pet coke.

Near-Term Supply and Demand Expectations

Near-Term U.S. Price Support: U.S. FOB prices are expected to remain firm due to lower freight costs and consistent export interest. The Venezuela-related geopolitical premium may persist in sentiment.

Recovery in Atlantic Demand: Buying activity in Europe, Turkey, and Africa is likely to increase through late January and February as cement producers secure feedstock for the spring construction season.

China’s Role: Post-Lunar New Year demand will be critical. If Chinese buying slows, upward pressure on low-sulfur USWC material could ease.

India’s Seasonal Lift: The final quarter of India’s financial year (January-March) typically brings higher construction and cement output, supporting coke import demand. However, competition from thermal coal will continue to cap significant price rallies.

Balanced but Firm Trend: Overall, the market is expected to balance strong Chinese demand for specific grades against a gradual recovery in Atlantic buying and fuel-switching in price-sensitive regions. U.S. export prices and premium low-sulfur grades should remain well-supported, while standard high-sulfur material may trade sideways until import activity picks up pace.

Leave a Reply