- MCX futures dip amid bearish global sentiment, softening domestic demand

- Orion Minerals secures up to $250 mn in Glencore funding for Prieska project

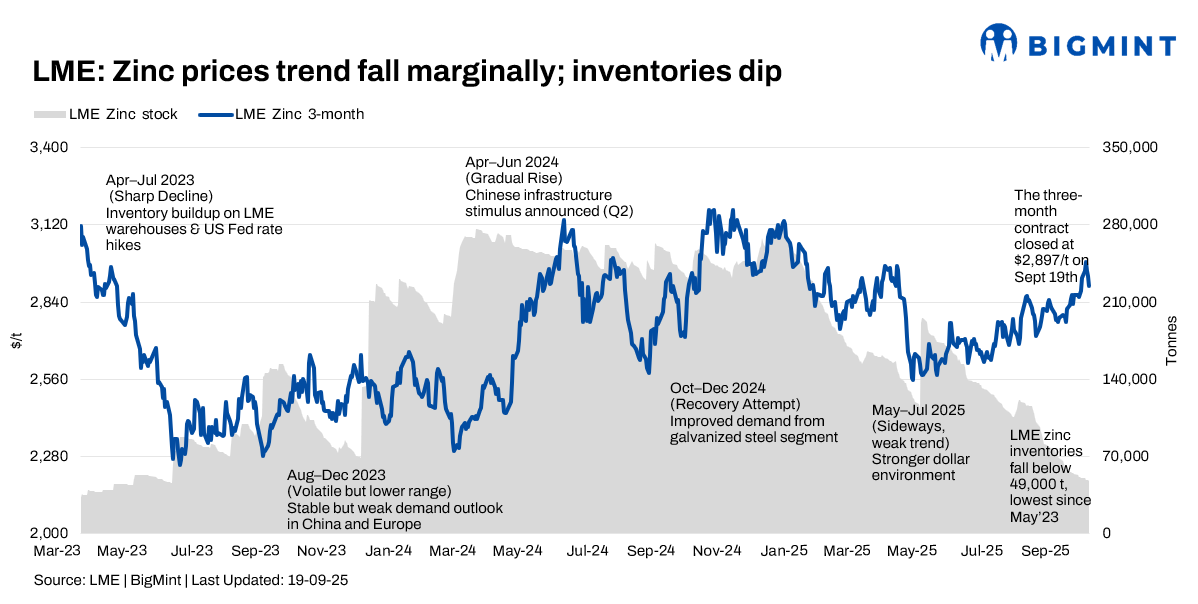

The London Metal Exchange (LME) zinc market experienced volatility, with prices ending the week slightly lower, as hawkish signals from the US Federal Reserve dampened market sentiment, despite a largely expected rate cut. This was balanced by the continued decline in LME inventories, which reached a 28-month low, and a weaker US dollar. The market ultimately navigated a week of conflicting signals and macroeconomic concerns.

Price trends & inventories

LME zinc cash-settlement prices fell 1.7% w-o-w, to $2,920.50/tonne (t) on 19 September since opening the week at $2,979.00/t on 15 September. The three-month LME zinc contract mirrored this pattern, down 1.8% w-o-w at $2,920.50/t on 19 September from $2,951.00/t on 15 September. The downtrend was primarily influenced by the US Fed’s less-dovish-than-anticipated monetary policy stance, which put short-term pressure on non-ferrous metal prices.

LME zinc inventories continued their declining trend during the week, reaching 48,825 t by 18 September from 50,150 t on 15 September. By 19 September, stocks had fallen to 48,800 t, marking a significant drop of 2.7% w-o-w. This continued destocking, reaching a 28-month low, indicates a tightening global supply of readily available zinc and helped contain a more significant price decline.

Market influences

US Federal Reserve: The US Fed cut interest rates by 25 basis points as expected but adopted a less dovish tone than anticipated. This hawkish rhetoric put downward pressure on zinc and other non-ferrous metals, particularly later in the week.

SHFE/LME ratio: The SHFE/LME zinc price ratio pulled back to around 7.5 and fluctuated, with the zinc ingot import window remaining closed. This disparity between overseas and domestic markets influenced price movements.

Demand: Downstream consumption in China continued to show signs of weakness, influencing domestic prices. Overseas, stable demand was noted in some sectors, but overall activity remained volatile.

Supply: Continued declines in LME inventories signalled tightening supply, offering support to LME zinc prices despite the macroeconomic pressures.

MCX zinc trends (15-19 September)

MCX zinc prices experienced volatility during the week, influenced by global sentiment and domestic factors. MCX zinc futures traded lower towards the end of the week. Prices increased from INR 279,900/t on 15 September to INR 283,150/t on 17 September and then softened to INR 278,450/t on 19 September. The downtrend was influenced by bearish global sentiment and a slight softening of domestic demand. Analysts cited reduced speculator exposure and slackened physical market demand as weighing on zinc prices.

Orion Minerals secures up to $250 million funding from Glencore for Prieska copper-zinc project

Australia’s Orion Minerals has signed a non-binding term sheet with Glencore for $200-$250 million to advance its Prieska copper-zinc project in South Africa. The deal includes a five- to ten-year offtake agreement for 100% of concentrates. Funding, disbursed in two tranches, will support early works and first production, subject to Glencore’s due diligence.

Outlook

The near-term zinc outlook remains cautious. While declining LME inventories and a softer US dollar provided some support, persistent oversupply concerns in China and global macroeconomic uncertainties are expected to keep prices volatile. Demand trends in both China and India and global economic dynamics, including further US Fed policy guidance, will provide further market direction.

Leave a Reply