- Structural deficit likely over coming years

- China’s 45 mnt cap limits supply growth

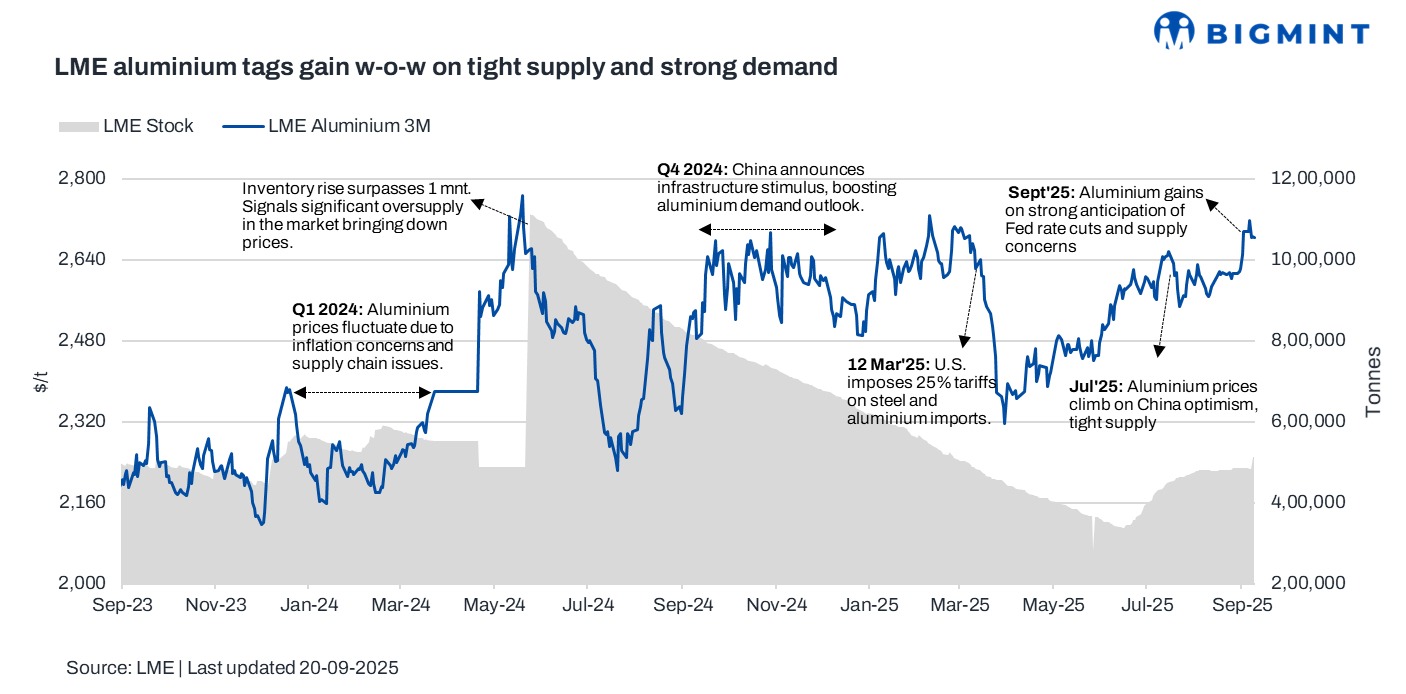

London Metal Exchange (LME) aluminium prices gained during week 38 of CY’25 (15-19 September 2025).

Aluminium prices worldwide are surging due to a rare global supply squeeze, rising demand, and US import tariffs under President Donald Trump.

The price rally is attributed to a combination of constrained global supply and robust demand. China’s long-standing production cap of 45 million tonnes (mnt), originally introduced in 2017 to combat industrial overcapacity, has now significantly altered the global supply balance. As China nears its cap, it is on track to become a net importer of aluminium, which is a dramatic shift for a historically oversupplied industry.

Pricing, inventory trends

LME aluminium prices averaged $2,693/tonne (t) in week 38, increasing by $55/t w-o-w and reflecting a 2% rise from week 37 (8-12 September). Prices opened the week at $2,695/t, hit $2,700/t levels mid-week, and closed slightly lower at $2,685/t.

Meanwhile, aluminium stocks at LME warehouses edged up 2.2% w-o-w, to 496,125 t in week 38 from 485,275 t in week 37.

Outlook

Prices are expected to remain range-bound in the upcoming weeks with a minor rise. The global aluminium market is heading towards potential deficits after years of surplus. China’s output growth has stalled due to capacity limits, with exports declining and imports rising. A structural shift towards higher aluminium prices is expected over the next five years.

Leave a Reply