- Profit-taking, cautious sentiment drag LME prices lower

- HZL, RIICO advance plans for world’s first Zinc Park

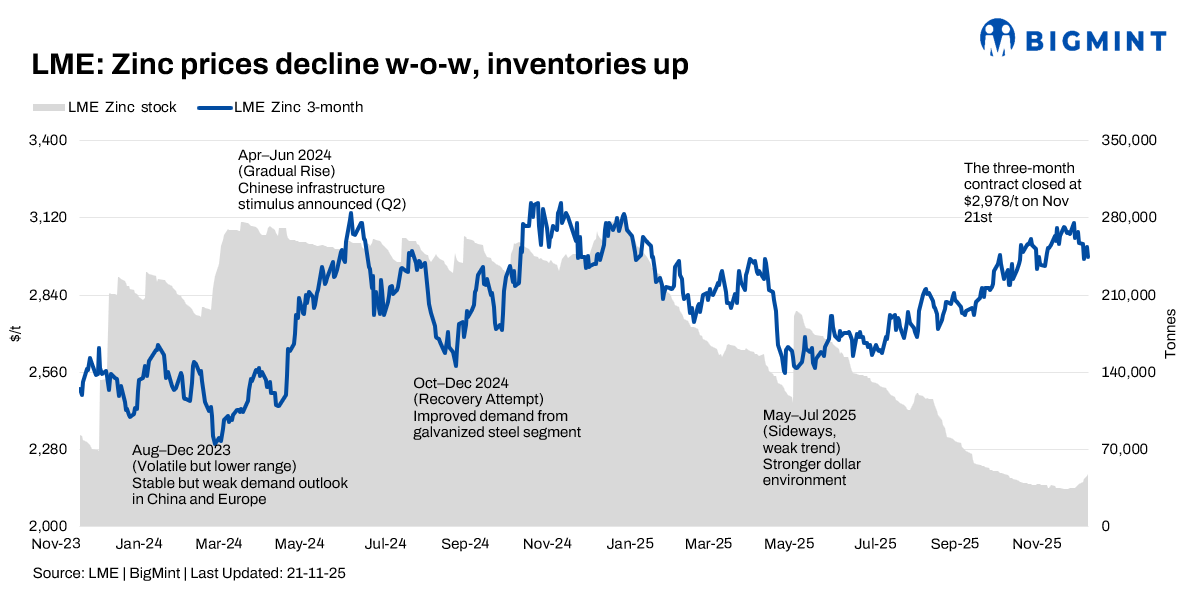

The London Metal Exchange (LME) zinc market experienced a volatile week over 17-21 November 2025, ending with a marginal decline despite strong fundamentals and significant inventory build-up. Prices were influenced by conflicting macroeconomic signals, a slowdown in 2026 contract negotiations due to steep backwardation, and signs of weaker demand from China, where exports are expected to rise.

Price trends

LME zinc prices showed a downward trend, opening around $3,231/tonne (t) and gradually declining to close near $2,992/t by 21 November. The market pulled back from an earlier eleven-month high near $3,300/t as investors reacted to broader base metal corrections and concerns about slowing demand growth, particularly from infrastructure and data centre sectors. Zinc futures in November hovered around $3,000/t, marking about a 1-2% decline from early November highs, reflecting some profit-taking and cautious sentiment amid uncertain global economic data.

The three-month contract also moved in the negative direction, drifting from $3,024/t to $2,978/t, a 1.52% decline.

Inventory analysis

LME zinc stocks increased by 18.3% from 39,975 t on 17 November to 47,325 t by 21 November. This inventory rise happened amid mixed market signals, with zinc supply tightening in other regions.

MCX zinc trends (17-21 November)

On the MCX, the November contract showed some short-term volatility during the week, touching approximately INR 302,100/t on 17 November. However, prices eased later to close near INR 306,250/t by 21 November, representing an increase of about 1.37% from the start of the week.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices started the week near RMB 22,800/tonne (t), with the contract experiencing a moderate 3.5% decline throughout the week to close around CNY 22,000/t by 21 November. SHFE trends were influenced by the tightening of domestic zinc concentrate supply amid increased exports by Chinese smelters, balanced against cautious demand sentiment in the Chinese market. The SHFE zinc price movements closely mirror global trends but are tempered by local supply considerations and policy factors.

Hindustan Zinc, RIICO advance plans for world’s first Zinc Park

Hindustan Zinc Limited (HZL) and RIICO have pushed forward plans for developing the world’s first Zinc Park through a stakeholder consultation held in Jaipur. The proposed park aims to create an integrated ecosystem for zinc, lead, silver, and allied industries, offering plug-and-play industrial land, renewable power, R&D facilities, and support for downstream manufacturing. The initiative is expected to boost value addition, attract global investment, and strengthen India’s position in the non-ferrous metals value chain.

Outlook

Zinc markets across LME, MCX, and SHFE are currently navigating price corrections after sharp rallies earlier in November. Key factors currently influencing the market include supply constraints, inventory fluctuations, and cautious demand outlooks in key industrial sectors. Future movements will depend on the balance between ongoing supply tightness, export dynamics, and global macroeconomic conditions affecting base metals demand.

Leave a Reply