- Supply recovery supports market optimism

- Year-end stockpiling limited across sectors

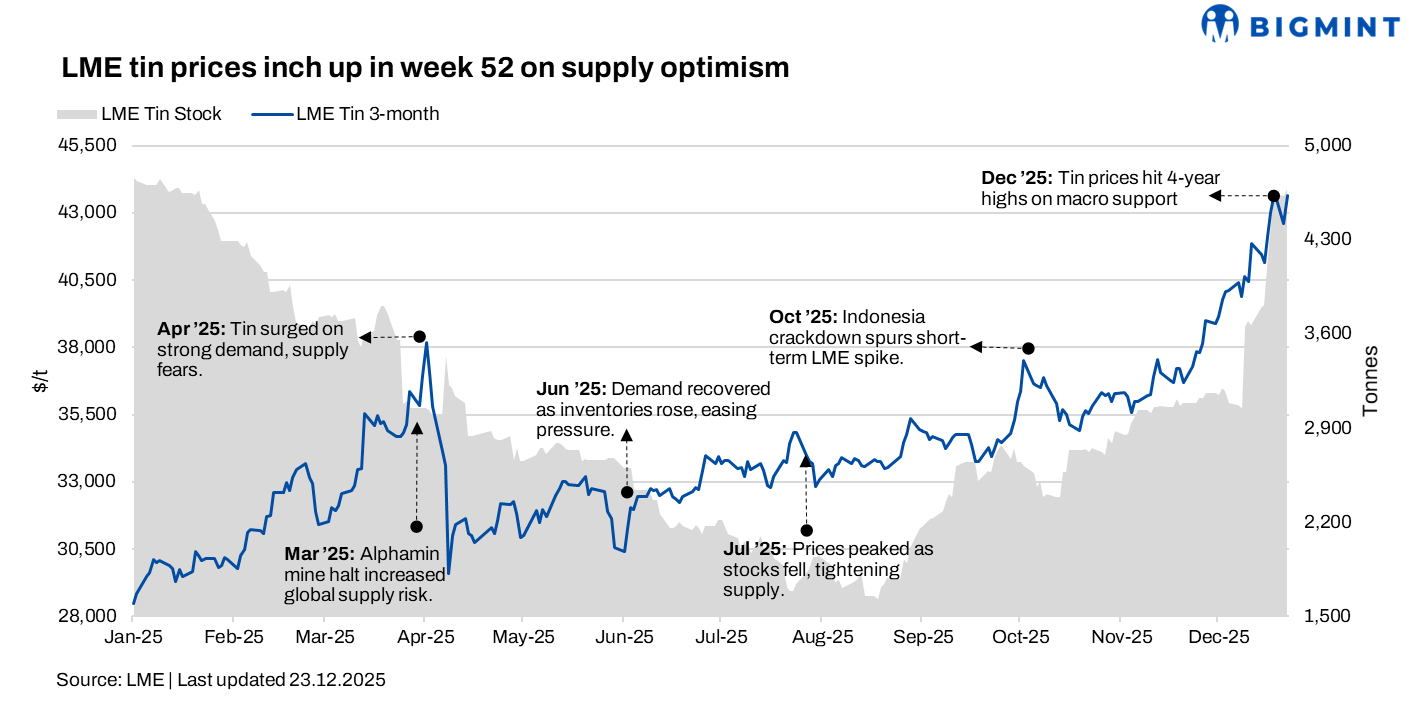

Tin prices on the London Metal Exchange (LME) rose slightly w-o-w in the week ended 26 December (week 52), continuing to hover near four-year highs. The LME remained closed for two days due to Christmas. Downstream demand stayed steady with limited transactions, while higher November imports, particularly from Myanmar, helped ease domestic supply tightness and supported cautious market optimism.

Pricing, inventory trends

LME tin prices averaged $43,137/tonne (t) in the week ended 26 December, marking an $1,687/t or 4% rise w-o-w from the previous week. The week began with prices at $42,625/t and then closed higher at $43,650/t.

Meanwhile, tin inventories at LME-registered warehouses rose 9% to 4,650 t from 4,174 t in the previous week.

Factors affecting prices

The London Metal Exchange (LME) was closed for the past two days. Downstream players largely maintained a cautious, wait-and-see stance yesterday, with inquiries slightly rising but overall transactions remaining limited. Year-end demand from downstream sectors remained steady, with companies generally maintaining normal operations and no significant stockpiling observed.

According to the latest data from the General Administration of Customs, China imported 15,099 t of tin ore and concentrates in November (equivalent to approximately 5,578 t in metal content), marking a slight decline of 0.67% y-o-y but an increase of 12.73% m-o-m. Imports from Myanmar totaled 7,190 t (approximately 1,636 t in metal content), up sharply by 92.16% y-o-y and 89.94% m-o-m. Imports from other countries, excluding Myanmar, reached 7,909 t (around 3,941 t in metal content), down 17.29% y-o-y and 3.58% m-o-m.

The November rise in tin concentrate imports helped slightly ease domestic raw material tightness. Cumulative imports from January to November reached about 118,100 t in physical content, down 1.88% y-o-y. Notably, imports of tin ore from Myanmar surged in November, with metal content also increasing m-o-m, signaling a gradual recovery in production.

Meanwhile, LME tin prices edged up slightly w-o-w, reflecting the market’s cautious optimism amid improving supply conditions.

Outlook

Tin prices are expected to remain supported near multi-year highs as downstream demand stays steady and supply tightness eases gradually with higher imports from Myanmar. Limited year-end stockpiling and cautious trading sentiment may cap sharp gains, while any disruptions in supply or changes in global demand could create short-term volatility in the market.

Leave a Reply