- Prices supported by limited mine supply growth and structural market tightness.

- Supply-side tightness to drive prices in 2026

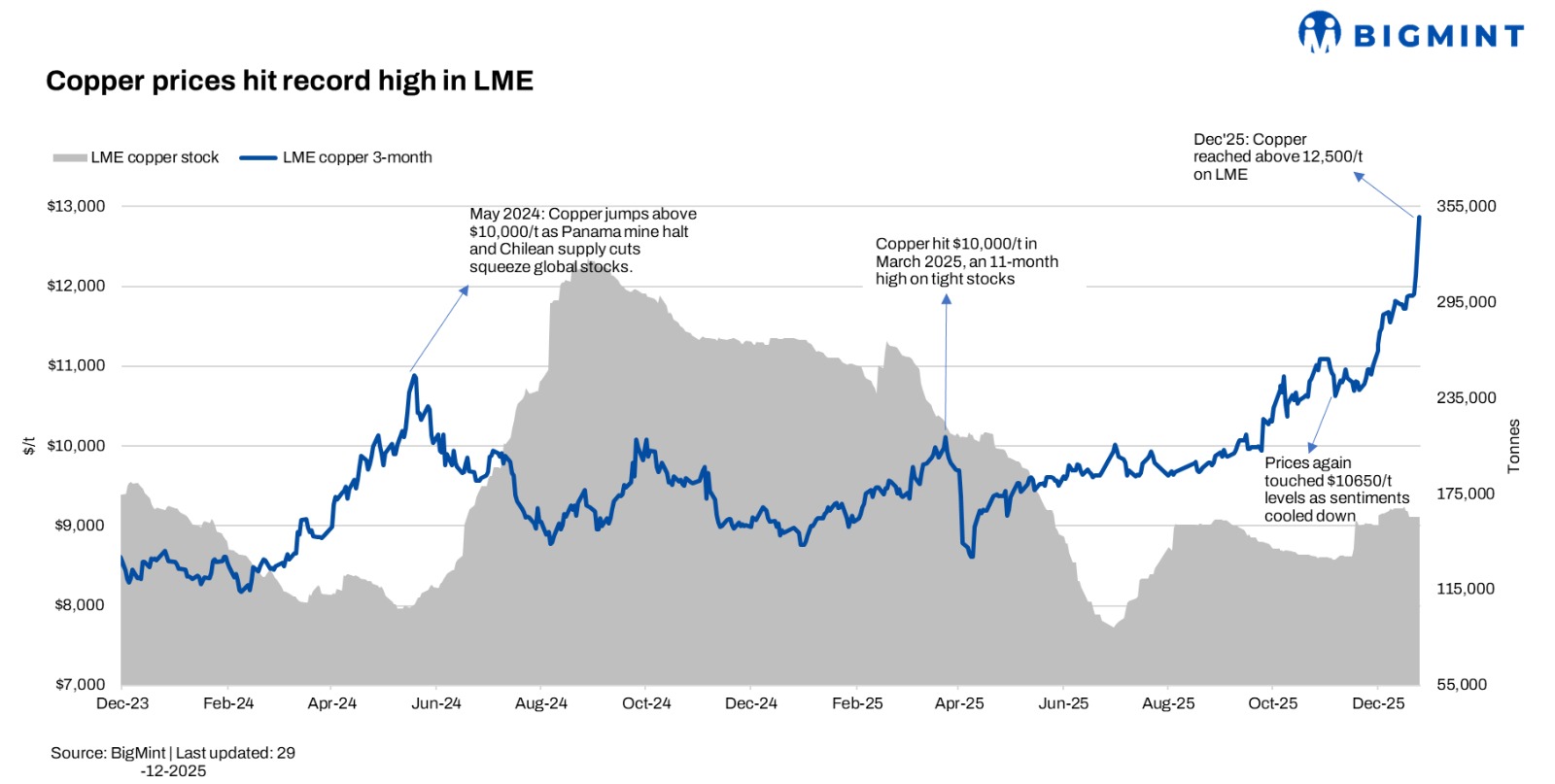

Benchmark copper prices on the London Metal Exchange rose 2.2% to $12,130/t from $11,870/t, however currently it has crossed $12,800/t mark, supported by limited mine supply growth and structural market tightness. The upside was primarily driven by the global supply outlook, which remains tight despite planned mine expansions. According to industry estimates, global copper mine production is expected to rise by around 700,000 t in 2026, supported by new capacity additions and project restarts. However, effective supply growth is likely to be significantly lower—closer to 300,000 t—after factoring in disruptions, ramp-up delays, and declining ore grades. Market participants estimate an average disruption rate of around 5–6%, which continues to cap realised output.

Mine capacity additions in 2026 are projected at approximately 730,000 t/y, sharply lower than the 1.2 mnt/y added in 2025, highlighting a slowdown in new supply entering the market. At the same time, the prolonged shutdown of key assets, including Cobre Panama (331,000 t output in 2023), continues to limit global availability and reinforces supply-side tightness.

On the demand front, copper consumption remains supported by structural trends. Global refined copper demand is projected to grow by around 2% y-o-y in 2026, underpinned by electrification, renewable energy investments, electric vehicle penetration, and grid expansion. Additional support is coming from rising investments in AI and data centres, which are copper-intensive due to high power density, cabling, and cooling requirements.

Macroeconomic factors also aided prices, as improved risk appetite and a softer US dollar encouraged investor participation in industrial metals. Copper continues to attract interest as a strategic metal linked to the global energy transition and digital infrastructure growth.

However, physical market sentiment remains cautious. Elevated LME prices have increased import parity costs, particularly in Asia, prompting buyers to limit fresh procurement and rely on near-term inventories. Seasonal slowdowns in downstream demand have further restrained spot buying.

Leave a Reply