- US-China dialogue improved overall risk sentiment this week.

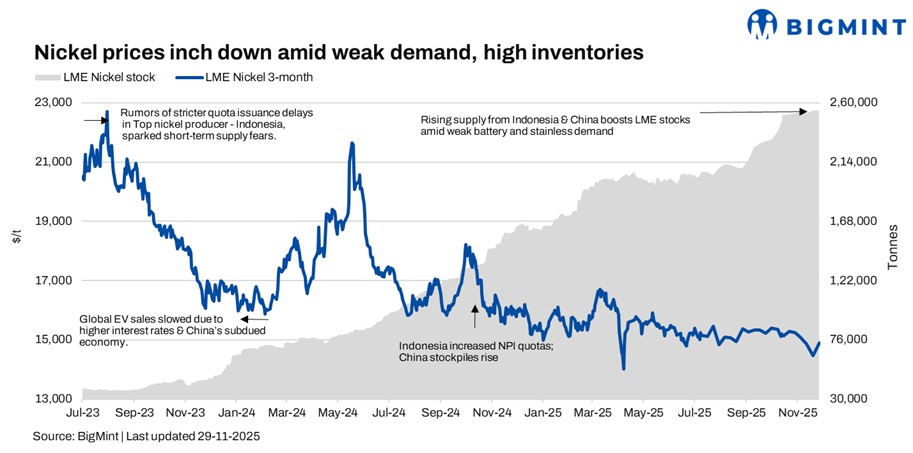

- LME nickel stocks rose slightly, signalling continued oversupply.

Nickel prices on the London Metal Exchange (LME) edged higher in the week ended 28 Nov, with the benchmark three‑month contract closing at $14,880/t on Friday, compared with $14,475/t last week. LME nickel stocks were broadly steady, rising slightly to around 254,760 t, from 253,950 t a week earlier, signaling that the market remains oversupplied despite the mild price rebound.

Market updates

Major Indonesian nickel plant cuts output on waste constraints

A major Indonesia nickel plant, PT QMB New Energy Materials, has reduced production after its tailings storage facility at the Morowali Industrial Park neared full capacity, forcing at least a two‑week cutback. The situation underscores mounting environmental and waste‑management challenges around HPAL projects in Indonesia, following earlier landslide‑related disruptions and ongoing local scrutiny of nickel industry impacts.

Fed rate cut hopes vs weak fundamentals

A recent US-China leaders call improved risk sentiment, while growing expectations of a December Fed rate cut weakened the dollar and spurred short‑covering in LME and SHFE nickel. At the same time, preparations for China’s upcoming Politburo and Central Economic Work Conference, a 5.5% drop in October industrial profits, and rising LME inventories kept fundamentals soft, leaving nickel prices only modestly higher.

Outlook

Nickel prices are expected to remain weak and range-bound in the near term, with limited upside. Growing supply from Indonesia and China, rising LME inventories, and soft demand especially from the stainless steel sector continue to weigh on sentiment. While temporary support may come from possible supply disruptions and a softer Fed stance, any price rebound is likely to stay capped and fragile amid abundant stocks and weak Chinese industrial indicators.

Leave a Reply