- SHFE, MCX trends remain volatile

- Greta Minerals to support India’s EV ambitions

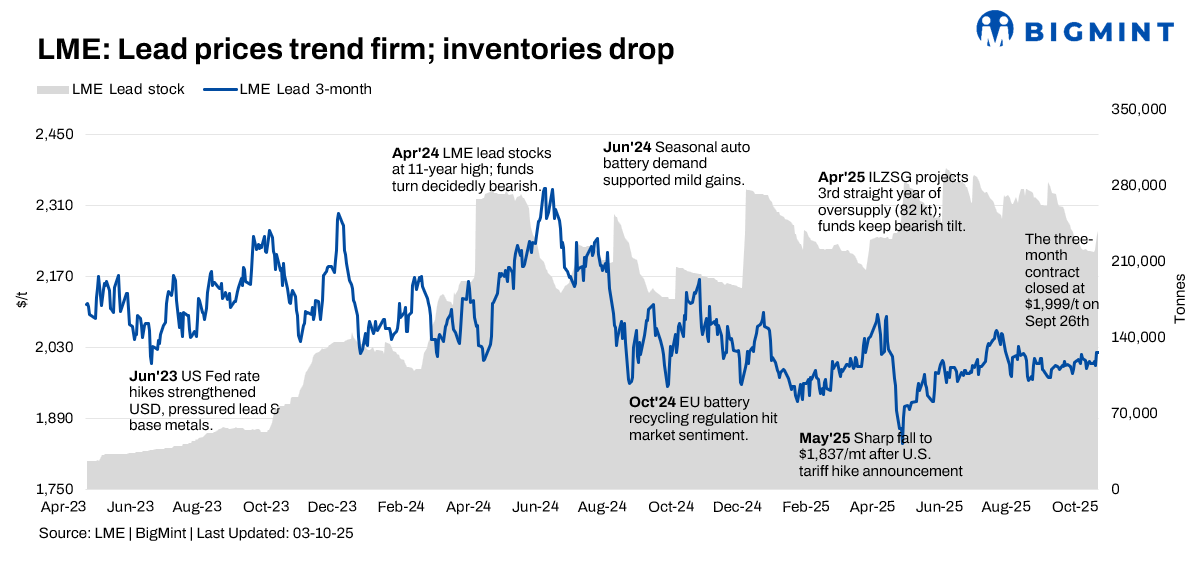

The lead market experienced a week of mixed signals and slight volatility during week 39 (29 September-3 October, 2025). While LME prices fluctuated, they ultimately moved within a tight range, influenced by divergent trends in global and Chinese inventories, as well as evolving macroeconomic and demand factors.

Price trends

LME lead cash-settlement prices showed some fluctuation during the week, ending slightly lower. Prices stood at $1,957/t on 29 September and were reported at a similar level on 30 September. The three-month contract ended the week at similar level as against last week and stood at $2,020/t.

LME lead inventories declined during the week, reaching a seven-month low. Stocks on the exchange fell from 219,425 t on 26 September to 218,825 t by 29 September. The overall trend of declining LME inventory suggests a tightening of readily available global supply. In contrast, Chinese inventory trends were less clear, with some reports suggesting continued declines due to maintenance at secondary smelters, while production was also being adjusted.

MCX lead trends

Domestic lead futures reflected moderate bullishness. The October expiry contract opened at INR 182,350/t on 29 September and closed at INR 183,900/t on 3 October, up 0.85% w-o-w. Indian prices followed global cues while being influenced by rupee fluctuations and modest demand recovery from the battery manufacturing sector.

SHFE lead trend

SHFE lead prices experienced volatility through the week. The most-traded SHFE lead 2511 contract hovered near RMB 16,940/t on 30 September, maintaining a narrow range. Domestic factors such as adjustments in production schedules and variable downstream consumption patterns shaped weekly price movement.

Greta Minerals doubles WA exploration area

Greta Minerals has expanded its exploration footprint in Western Australia from 700 sq km to nearly 1,550 sq km, targeting lithium-rich zones at its Gecko North project. Early soil sampling has identified lithium, gold, and caesium anomalies. The company’s expansion supports India’s strategy to secure critical minerals, particularly lithium, strengthening supply partnerships between India and Australia for the EV and battery manufacturing sectors.

Outlook

The near-term lead market outlook remains cautious. While continued inventory declines support prices, muted consumption and uncertain macroeconomic indicators could cap gains. With Chinese holidays and contract rollovers introducing short-term volatility, market participants will monitor LME and Chinese stock trends, as well as demand signals from battery and automotive sectors, for price direction in the coming weeks.

Leave a Reply