- Market remains cautious during year-end positioning

- China cuts tariff on battery black mass imports starting 1 Jan

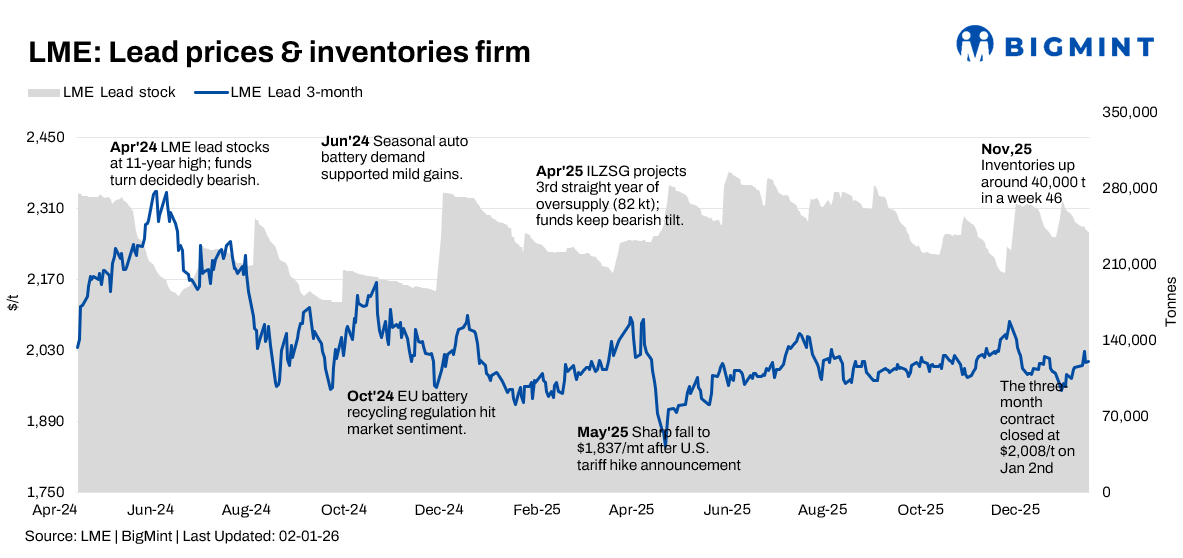

The London Metal Exchange (LME) lead market showed mild firmness during 29 December 2025-2 January 2026, with prices edging higher despite thin holiday trades. Stable exchange inventories and comfortable global supply fundamentals capped upside momentum, while light dip-buying offset softer signals from battery-sector demand.

Price trends

LME lead cash prices opened at around $1,955/t on 29 December, traded at a level of around $1,980/t on 30 December, and closed at approximately $1,968/t by 2 January, posting a modest 0.6% weekly gain. The three-month contract rose from roughly $2,002/t to $2,008.5/t, up 0.45% w-o-w, stabilising in the $1,980-2,010/t range.

Inventory

LME lead stocks remained ample and broadly stable, declining from 255,950 t on 22 December to 244,275 t by 29 December (down 4.5% w-o-w). Despite the drawdown, inventories remain well above historical averages. Combined registered and off-warrant stocks exceed 400,000 t, indicating structural oversupply, even as Chinese social inventories tightened due to temporary smelter maintenance.

MCX lead trends (29 Dec-2 Jan)

On the MCX, the 30 January 2026 lead contract traded at INR 182,550/t on 29 December and edged up to INR 182,900/t by 2 January, gaining 0.2% over the week. Prices remained range-bound between INR 182,000-184,000/t. Trading volumes thinned due to the holiday period, though steady battery replacement demand provided near-term support.

SHFE lead trend

On the SHFE, the February 2026 (2602) lead contract fell 2.22% w-o-w to CNY 17,255/t from CNY 17,645/t, ending a six-session rally. While smelter production halts offered cost-side support, subdued battery demand and a neutral SHFE-LME arbitrage environment capped further recovery.

China cuts tariff on battery black mass imports

China has reduced import tariffs on lithium-ion battery black mass, from 6.5% to 3%, effective 1 January. The move aims to support the domestic battery recycling sector by lowering feedstock costs and improving material availability. However, the immediate impact may be limited, as some supplier countries already benefit from preferential duties. The policy builds on earlier measures to address recycling overcapacity and reduce reliance on primary mined resources.

Outlook

Lead markets consolidated during the period, with LME prices gaining 0.4-0.5% despite SHFE weakness and persistently high inventories near 260,000 t. Near-term price direction will hinge on battery restocking activity, Chinese export flows, and the pace of LME inventory draws. Absent supply-side disruptions and structural oversupply are expected to cap upside potential.

Leave a Reply