- High inventories, mine operational challenges support LME prices

- Major producer cuts 2026 output forecast reinforcing supply concerns

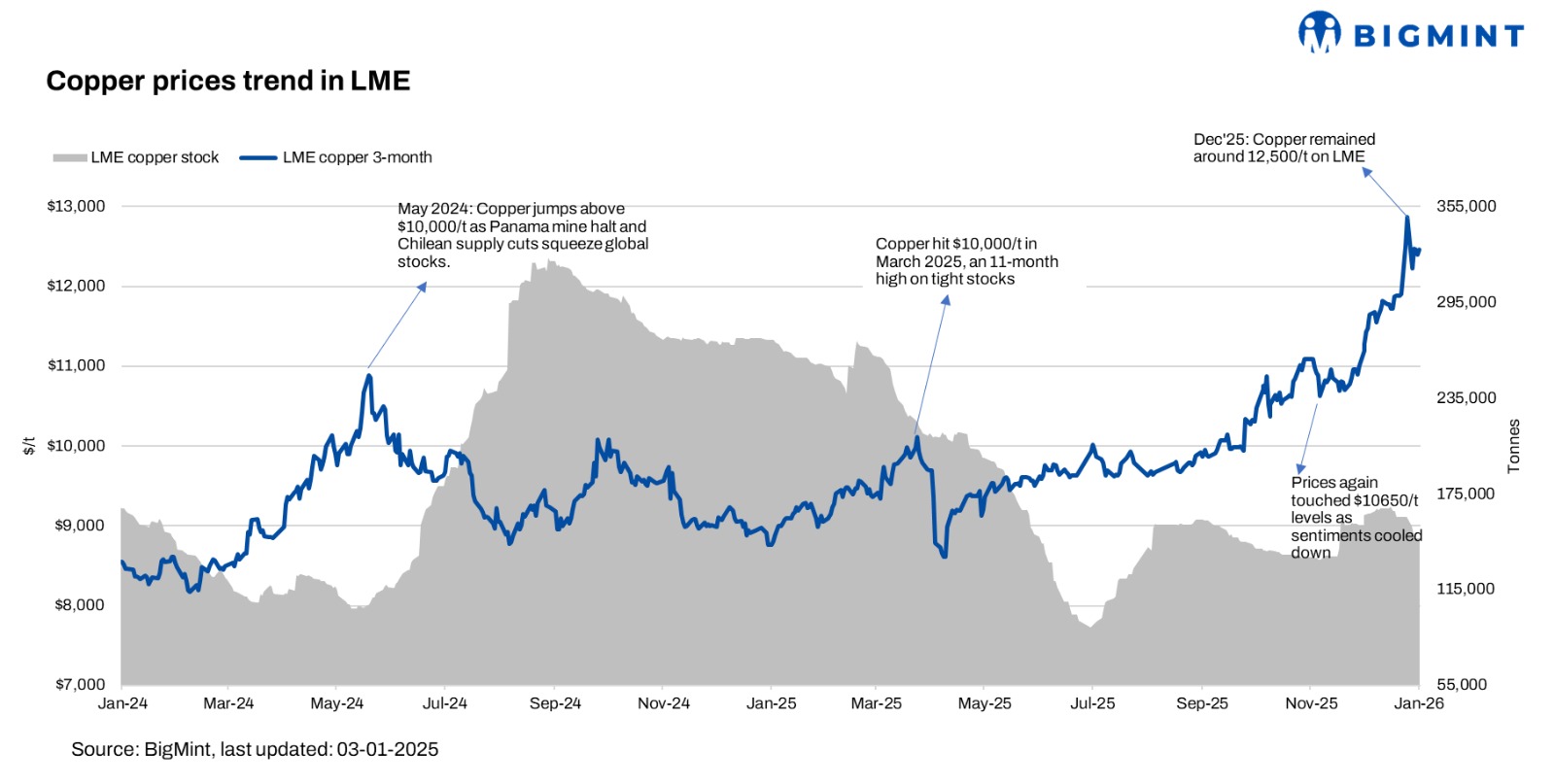

LME copper prices extended gains into the first week of January, with the three-month contract rising 3.5% w-o-w, climbing from $12,040/t on 26 December 2025 to $12,460/t on 2 January. This builds on the strong rally witnessed through late 2025 and reflects continued market focus on structural supply constraints amid resilient demand cues.

LME prices over the past month has been supported by multiple factors. Exchange inventories remain relatively tight compared with historical norms, limiting prompt availability and reducing the buffer against spot tightness. Additionally, several major mines and expansions have faced persistent operational challenges – including water shortages, lower ore grades and regulatory hurdles – which have weighed on global mine output growth. Recent company guidance from a top producer saw a near- 10% reduction in its 2026 copper production forecast, highlighting ongoing supply risks.

End-users in key consuming regions, including India and Asia, have reduced immediate restocking due to elevated price levels that have outpaced physical demand growth.

With many Western suppliers on year-end holidays, import flows into major consuming regions were relatively muted in the final week of December. However, some high-grade scrap and semi-finished material from Africa was reported traded, highlighting selective activity in the physical market. Meanwhile, policy developments and the recent withdrawal of certain quality control orders in major markets have started to improve sentiment around future import availability.

Global copper concentrate deficit to persist in 2026

Copper concentrate supply is expected to remain structurally tight in 2026, as smelter demand continues to outpace mine supply, despite a slowdown in new smelting capacity additions. Global copper demand is forecast to continue growing in 2026, with refined copper consumption projected to increase by around 2.1% y-o-y, following an expansion of approximately 3% in 2025 as industrial activity and electrification trends sustain usage growth.

At the same time, global refined copper production is expected to rise only modestly, with output forecast to increase by about 0.9% in 2026 after a stronger 3.4% rise in 2025, according to the latest estimates from the International Copper Study Group (ICSG). This imbalance (higher consumption growth relative to supply expansion) contributes to expectations of a supply deficit of around 150,000 t in 2026, turning the market from a projected surplus in 2025 to deficit this year.

Leave a Reply