- Ex-mill prices in central India hold firm

- East coast trade selective, west coast sees export momentum

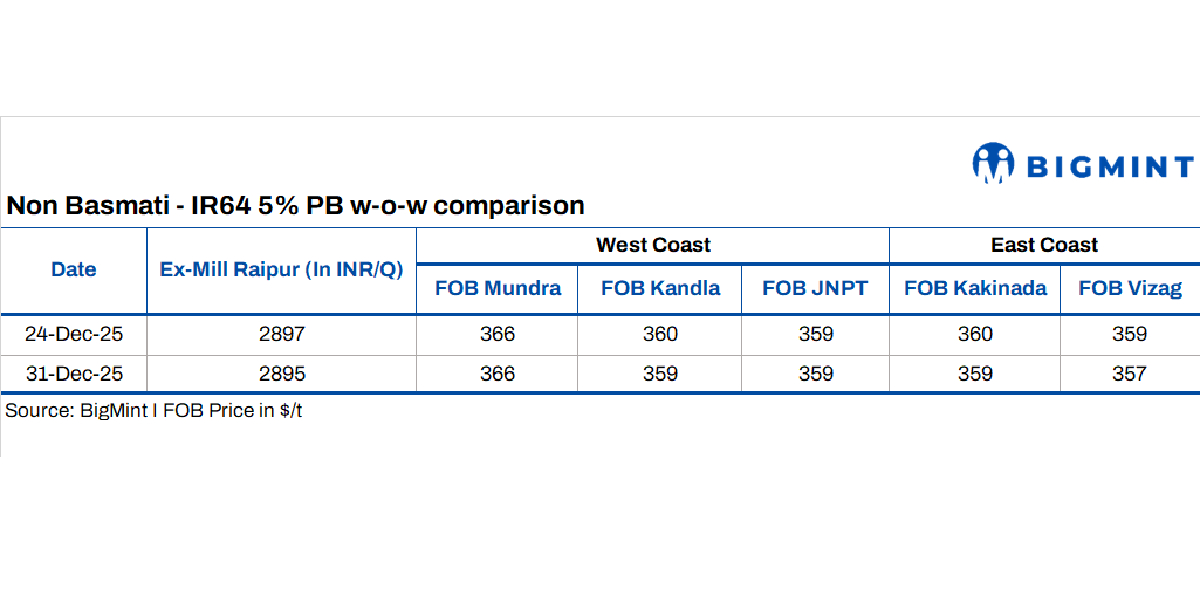

Ex-mill rice prices in Raipur were largely stable in the week ended 31 December 2025, easing marginally by 0.07% w-o-w to INR 2,895 per quintal, compared with INR 2,897 a week earlier. The market continues to grapple with slow paddy circulation, which has limited mills’ ability to scale up trade despite steady underlying demand.

Market participants said most states have already completed paddy procurement for further processing, while Chhattisgarh remains an outlier. Delays in state-level policy execution—particularly around open market sale scheme (OMSS) operations and minimum support price- (MSP)-linked disbursement—have pushed paddy distribution to mills toward late January. As a result, spot availability remains thin, discouraging aggressive selling by millers.

According to Agmarknet data updated toward the end of December, Chhattisgarh recorded 2.75 million tonnes (mnt) of paddy arrivals in December 2025. Balod led arrivals at 121,043 t were followed by Bastar, Mungeli, Balodabazar and Rajnandgaon. Traders expect smoother paddy distribution in January to gradually improve rice availability, keeping prices broadly range-bound in the near term.

Selective port activity, freight inflation cap competitiveness

East coast FOB prices softened modestly w-o-w, reflecting improving supply visibility but constrained execution. FOB Kakinada slipped 0.28% to $359.t while FOB Vizag fell 0.56% to $357/t. Kakinada remained the most active east coast port during the week, driven largely by Andhra Pradesh-based trade.

However, participants cautioned that Andhra Pradesh alone cannot meet large buyer requirements, particularly for vessel parcels of 15,000-20,000 t, as state enforcement against Public Distribution System (PDS) diversion and central policy sensitivities continue to regulate export flows. No meaningful loading was reported from the Chhattisgarh belt, where slow paddy distribution has curtailed milling activity.

Logistics costs have emerged as a fresh pressure point. Road freight rates have risen sharply due to truck shortages, as vehicles are diverted for maize movement. Freight from Raipur to Vizag increased to INR 160 per quintal from INR 140, while Raipur-Kakinada rates climbed to INR 210 per quintal from INR 190, eroding east coast price competitiveness despite marginally softer FOB values.

West coast ports: Prices firm on demand pull

West coast FOB prices were largely steady, underpinned by stronger export execution and tighter supply dynamics. FOB Mundra held unchanged at $366/t, while FOB Kandla edged down 0.28% to $359/t. FOB JNPT remained flat at $359/t.

Traders attributed the firmness at Mundra to reduced kharif output following weather-related crop damage, particularly in select non-basmati varieties, which has tightened domestic availability. This has coincided with steady demand from South India and the Middle East, while geopolitical disruptions along key shipping routes have encouraged inventory building.

The west coast continues to benefit from relatively faster evacuation and smoother port operations, supporting India’s export flows to Africa and West Asia. In contrast, infrastructure and supply-side bottlenecks on the east coast have limited its ability to capitalise on demand despite competitive pricing.

Raipur IR64 PB trades stay thin in late Dec’25

During the last week of December, a total of five export deals were concluded for IR64 parboiled rice from Raipur. These included 1,385 t of IR64 5% PB and 270 t of IR64 10% PB, cumulatively accounting for 1,655 t. The shipments were primarily destined for Benin (West Africa), with dispatches routed via Kakinada and Vizag ports.

Despite firm price levels, the relatively small parcel sizes indicate that only minute, need-based trades are currently taking place from the Raipur belt, reflecting cautious exporter participation and limited spot market liquidity rather than broad-based buying interest.

Outlook

With supply gradually improving and prices showing only marginal w-o-w adjustments, the rice market is entering 2026 on a stable footing. Participants expect ex-mill prices to remain supported until paddy distribution accelerates meaningfully in Chhattisgarh. Export competitiveness will hinge on freight normalisation and policy clarity, particularly for east coast flows, while west coast ports are likely to retain their execution advantage in the near term.

Leave a Reply