- Gulf conflict threatens European aluminium supply

- Indonesia approves plan to impose export taxes on nickel

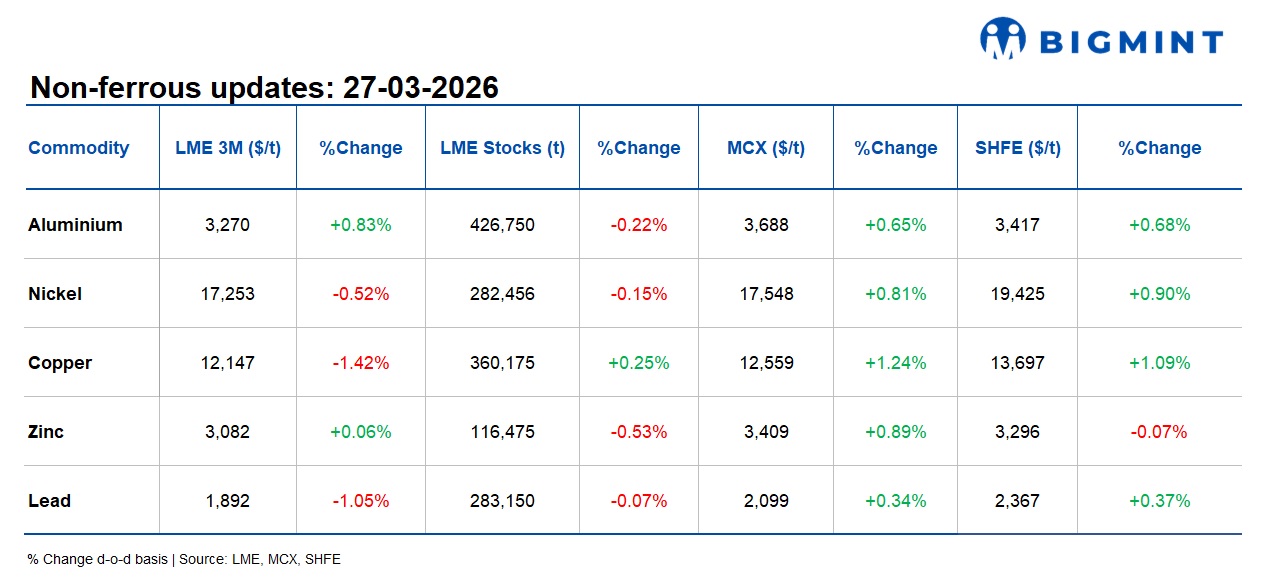

Base metals on the London Metal Exchange (LME) traded mixed d-o-d as of close of trading on 26 March, indicating divergent market sentiment across metals. Aluminium edged up 0.83% to $3,270/t, while zinc remained largely stable with a marginal gain of 0.06% to $3,082/t. In contrast, copper declined 1.42% to $12,147/t, nickel fell 0.52% to $17,253/t, and lead dropped 1.05% to $1,892/t.

On the inventory side, trends were also mixed. Copper stocks increased 0.25% to 360,175 t, indicating slightly improved availability. Aluminium inventories declined 0.22% to 426,750 t, while nickel stocks fell 0.15% to 282,456 t. Zinc inventories dropped 0.53% to 116,475 t, and lead stocks decreased 0.07% to 283,150 t, pointing toward a mild drawdown across most base metals.

Domestic market overview

India’s non-ferrous scrap market remained positive, indicating improving domestic buying sentiment. Aluminium tense scrap (loose), ex-Delhi, increased by INR 7,000/t (2.8%) to INR 254,000/t from INR 247,500/t, while ex-Chennai prices also strengthened by INR 5,000/t or 2% to INR 252,000/t from INR 248,000/t.

Similarly, prices of copper armature scrap (Cu 99%), ex-Delhi, rose INR 15,000/t or 1.4% to INR 1,115,000/t from INR 1,100,000/t, reflecting steady demand and firm market fundamentals.

Other updates

EU’s duties on Chinese converter foil set to expire

The EU will allow anti-dumping duties on Chinese aluminium converter foil to expire on 9 December 2026, unless a sunset review is initiated. The duties, ranging from 15.4% to 28.5%, have been in place since 2021 on foil under CN code ex 7607 11 19, covering thickness of 0.021-0.045 mm used in packaging and industrial applications.

Post-expiry, the removal of duties may reduce import costs and increase Chinese supply in the EU market, potentially intensifying competition for domestic producers.

Gulf conflict threatens European aluminium imports

Spain’s aluminium supply chain is under pressure, with over 30% of imports at risk due to the ongoing Gulf conflict, disrupting flows from key producers such as Qatar (Qatalum) and Bahrain (Alba). Production disruptions and logistical constraints through the Strait of Hormuz have tightened global availability, impacting raw material security.

The Spanish aluminium sector, valued at around EUR 4.4 billion and employing around 17,000 people, remains significantly exposed, with the Gulf accounting for a notable share of primary metal supply. Rising freight costs, insurance premiums, and shipment delays are further elevating input costs for downstream industries such as automotive and construction.

The situation presents a dual risk of cost escalation and production disruption, potentially weakening competitiveness against global suppliers amid an already tight aluminium market.

Alcoa targets full capacity ramp-up at Spain smelter by 2026

Alcoa is targeting a full restart of its San Ciprián aluminium smelter in Spain by mid-2026, following delays caused by high power costs and operational disruptions, including a major outage in 2025.

The smelter, with a nameplate capacity of around 228,000 t/year (equivalent to 5% of European output), was curtailed in 2021 and is undergoing a phased restart supported by a joint venture with Ignis Equity Holdings.

Despite progress, Alcoa expects financial pressure during the restart phase, with projected losses of up to $110 million, before achieving stable operations.

The restart is expected to tighten regional supply dynamics, supporting European aluminium availability while partially offsetting import dependence.

Nickel prices gain on Indonesia policy shift, supply concerns

LME nickel prices moved higher, closing near $17,400/t on 25 March, following Indonesia’s approval of a plan to impose export taxes on nickel and coal shipments, raising concerns over tightening global supply.

The proposed policy, expected to be implemented as early as April, has strengthened market sentiment, as traders anticipate reduced export availability from the world’s largest nickel producer.

The move is driven by fiscal pressures, rising energy costs, and Indonesia’s strategy to promote domestic value addition, which could lead to increased price volatility and a structural shift in global nickel trade flows in the near term

Oil market shows temporary relief amid ongoing Gulf tension

The US has extended the pause on potential strikes on Iran’s energy infrastructure by 10 days (until early April), signalling continued diplomatic efforts despite ongoing conflict in the region.

Following the announcement, oil prices eased, reflecting short-term relief in market sentiment amid expectations of reduced immediate supply disruption. However, the situation remains volatile as military activity continues across Iran, Israel, and neighbouring regions, with the Strait of Hormuz — a critical route for around 20% of global oil trade — still under pressure.

Overall, the development indicates a temporary easing in supply-side risk, though persistent geopolitical tensions continue to pose significant uncertainty for global energy markets and trade flows.

Guinea, EGA move toward resolution of bauxite asset dispute

Guinea and Emirates Global Aluminium (EGA) are nearing a settlement to resolve their bauxite asset dispute, following the government’s seizure of EGA’s mining operations in 2025. The proposed deal is likely to involve financial compensation linked to bauxite supply, aligning with Guinea’s push for greater control and downstream value addition.

If concluded, the agreement could stabilise bauxite supply and ease legal uncertainty, though it also highlights rising resource nationalism risks in key aluminium-producing regions.

Leave a Reply