- NAPP coal demand gains amid elevated pet coke prices

- Price pressure likely as supply growth to outpace demand

The Indian west coast is bracing for a wave of American coal. Over the next two months, more than 2.1 million tonnes (mnt) of high-calorific value (CV) Northern Appalachian (NAPP) coal are scheduled to arrive at ports like Kandla and Tuna, according to vessel line-up data.

This influx arrives at a time of extreme volatility in global energy markets, driven by the ongoing conflict in the Middle East and its chokehold on the Strait of Hormuz. While the material is eagerly awaited due to a shortage of high-quality fuel, it presents a complex puzzle for Indian cement makers and traders.

The tale of two fuels: US NAPP vs petcoke

For Indian cement manufacturers, the two primary fuels of choice are US-origin high-CV NAPP coal, with a net calorific value (NCV) of 6,900 kcal/kg, and petroleum coke (pet coke), typically the 6.5% sulphur grade from the US Gulf, which offers a higher NCV of 7,500 kcal/kg. A key distinction lies in their application: while pet coke is confined to use in cement kilns due to its high sulphur content, US NAPP coal offers greater flexibility, serving both kilns and captive power plants (CPPs).

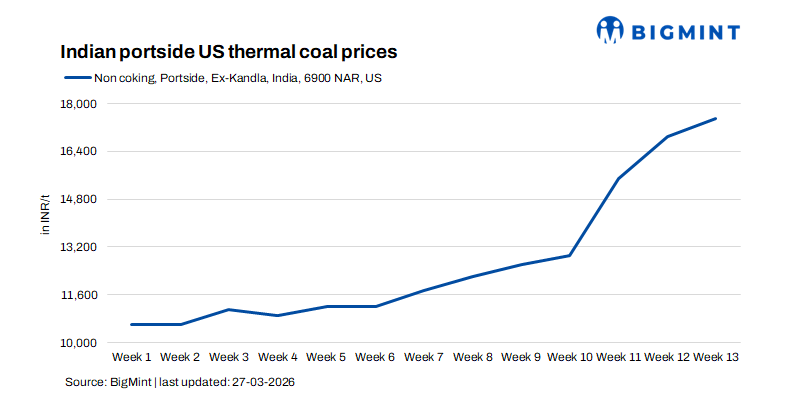

The recent rally in pet coke prices has dramatically reshaped this competitive landscape. Prices of 6.5% sulphur pet coke on a CFR India basis have surged to a three-year high, reaching $158/t in late March. According to BigMint’s assessment, portside prices of US thermal coal (6,900 NAR) in India rose by INR 600/t w-o-w to INR 17,500/t. Market indications suggested offers reaching up to INR 18,500/t, while a trade for approximately 3,000 t was reportedly concluded at INR 17,800/t, reflecting the strengthening price sentiment.

This spike is fuelled by rising US Gulf freights and constrained supply, exacerbated by refinery outages and limited cargoes from the Middle East due to the Hormuz crisis.

In this context, US NAPP coal has emerged as a compelling alternative. A June-loading Capesize cargo of NAPP 6,900 kcal/kg coal was sold to an Indian cement firm at $150/t CFR west coast India. With pet coke prices at similar or higher levels, the coal offers distinct advantages. While some cement plants still require a proportion of coke in their kiln fuel mix, the narrowing price gap is shifting this balance. The vessel list shows major cement producers such as Ultratech and Ramco are among the recipients of the incoming NAPP cargoes, underscoring their pivot towards coal to manage fuel costs amidst soaring pet coke offers.

From shortage to surplus

The central question now is whether the Indian market can absorb the massive 1.34 mnt of NAPP coal designated for the “retail” sector without a significant price correction.

Multiple market participants reported a “shortage” or “no stock” of US coal at Kandla in mid-to-late March, but this could be attributed to vessel arrival schedules rather than fundamental demand. With over a million tonnes of retail cargo scheduled to hit the west coast in the coming weeks, the current portside shortage is about to turn into a glut.

More telling is the commentary on market sentiment. One trader noted that “reduced loading activity at ports and subdued industrial demand limited trading momentum… transactions continued at thin or negligible margins.” This points to a classic pre-correction scenario where buyers are hesitant, and traders are struggling to pass on high costs.

The fate of the floating vessels

Will the massive floating vessels be “snapped up” by the cement industry? The short answer is likely no, at least not at current price levels.

Cement makers, with the luxury of domestic coal alternatives and a strategic view on inventory, are in a strong bargaining position. They have already secured some volumes for their immediate needs, as seen in the dedicated “Industry” vessel list. For the retail cargoes, the cement industry is more likely to act as opportunistic buyers. They will wait for the physical market to saturate — when vessels arrive in quick succession and port silos are full — and then step in to purchase at distressed prices.

The outlook is one of impending pressure. With a massive retail pipeline set to discharge into a market showing signs of demand fatigue and margin compression, the most probable scenario is a market correction. Prices are likely to soften in April and May as buyers hold the upper hand, forcing traders to liquidate positions.

Leave a Reply