- Weak lending data from China dampens sentiment

- Investment inflows into LME aluminium contracts increase

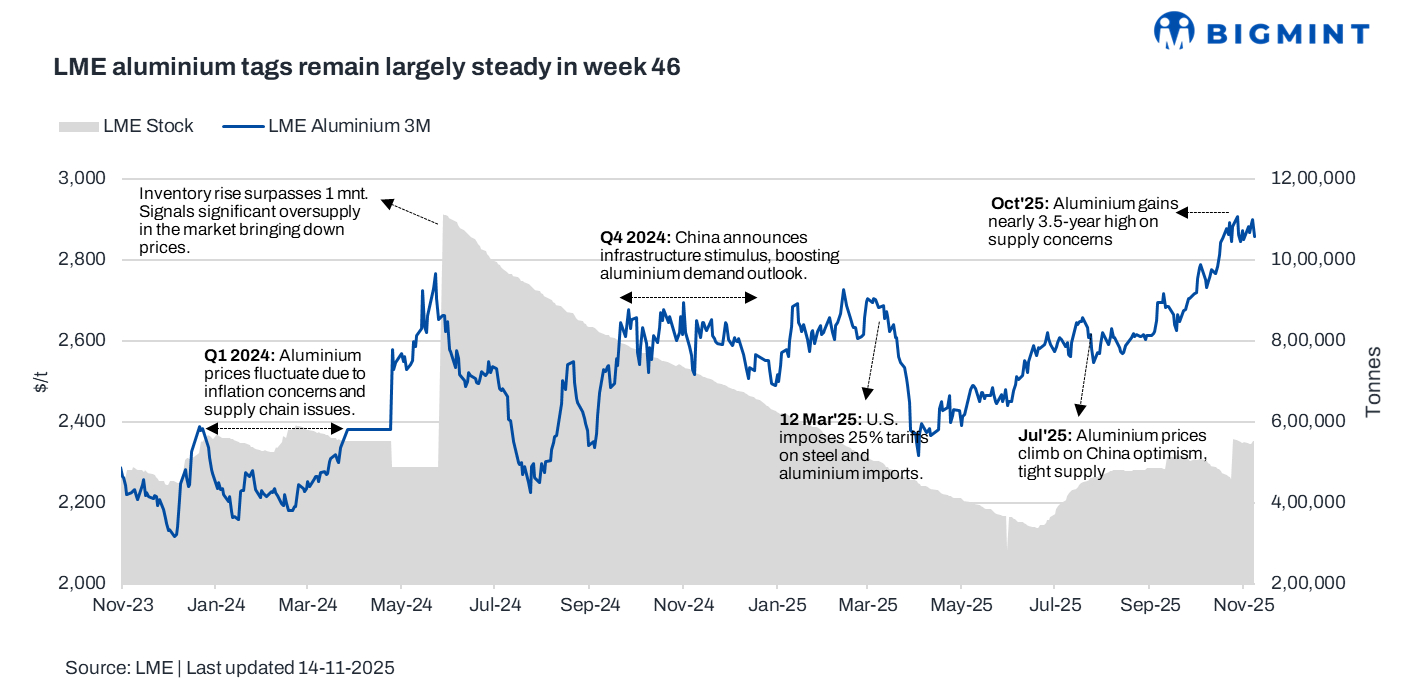

LME aluminium prices stood rangebound during week 46 of CY’25 (10-14 November), keeping up the firm trend on persistent supply concerns. The firm prices were supported by production disruptions, slower capacity growth in China, and resilient global demand indicators.

Pricing, inventory trends

LME aluminium prices averaged $2,879/tonne (t) in week 46, marking a $12/t or 0.4% rise w-o-w from week 45 (03-07 November). The week began with prices at $2,883/t, which inched up to around $2,900/t mid-week and closed at $2,857/t.

Supporting the price, LME aluminium inventories witness outflows for the week at 548,420 t from 551,040 t in week 45.

What impacted the prices for the week?

Prices remained steady throughout the week, primarily driven by ongoing supply concerns. However, a significant uptrend was absent as traders took profits following weaker-than-expected lending data from China. Bank lending in October dropped sharply, highlighting persistent softness in credit demand and dampening sentiment across industrial metals.

Despite this, the downside was limited due to continued supply tightness, supported by China’s renewed efforts to stabilize growth, the U.S. nearing the restoration of full government operations, and ongoing production disruptions at various smelters worldwide.

Market support was also bolstered by expectations of improving demand and constrained output growth in China, which remains limited by its aluminium capacity cap of 45 mnt. Investment inflows into LME aluminium contracts have strengthened, reflecting growing optimism that years of oversupply may be coming to an end.

SHFE aluminium inventories dipped by 0.2%, further reinforcing the tightening supply narrative. Production disruptions continued to exert upward pressure, with Iceland’s Grundartangi smelter suspending a potline, Alcoa announcing the closure of its Kwinana alumina refinery, and Century Aluminium cutting two-thirds of output at its Iceland smelter.

Looking ahead

The outlook for LME aluminium remains firm, supported by ongoing supply concerns and production disruptions, particularly in China and key smelters worldwide. While weak lending data from China may dampen short-term sentiment, tightening inventories and constrained output growth, coupled with strong global demand, suggest that aluminium prices will remain supported in the near term, with potential for gradual price increases.

Leave a Reply