- Chinese smelter constraints limited output growth

- Near-term price sentiment remains broadly supportive

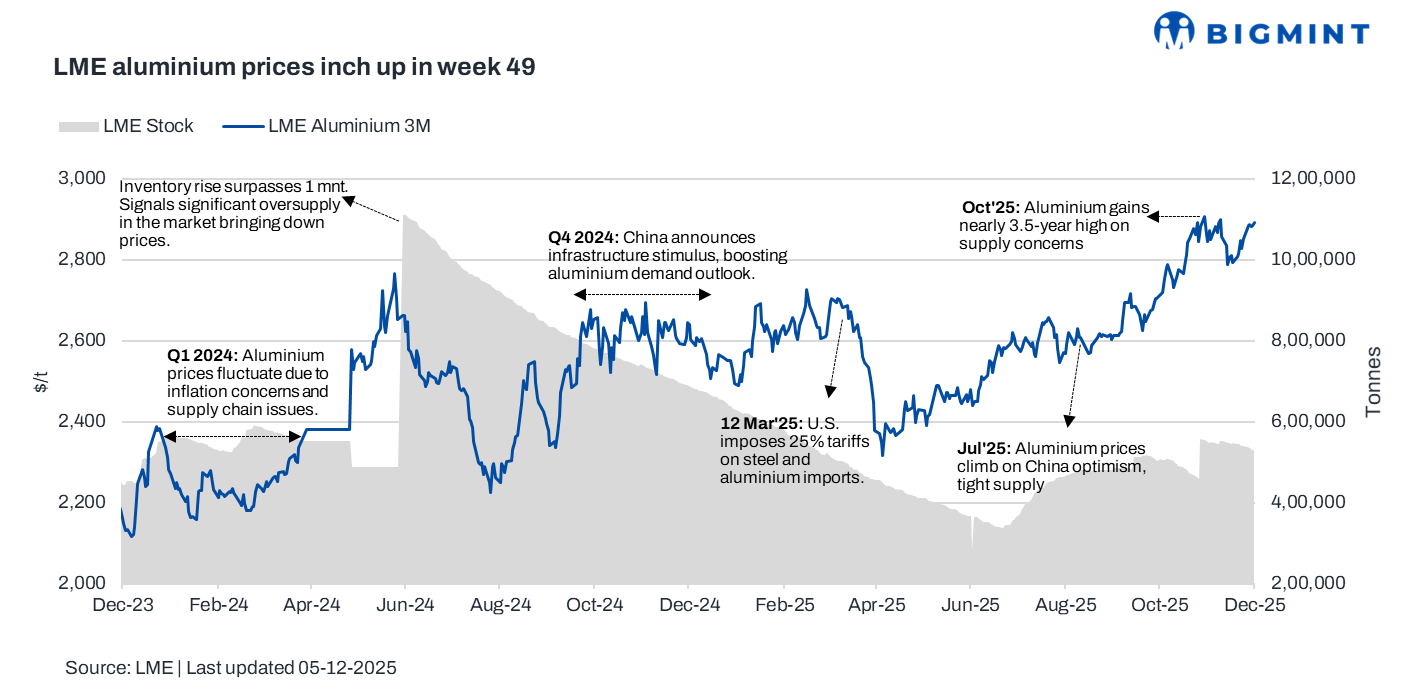

Aluminium prices on the London Metal Exchange (LME) edged higher w-o-w in the week ended 5 December. Prices rose as tightening supply met strengthening demand. Capacity constraints at Chinese smelters, falling inventories, and global production disruptions restricted availability, while China’s robust import appetite and solid export flows signalled improving consumption, collectively lifting market sentiment and supporting price gains.

Pricing, inventory trends

LME aluminium prices averaged $2,888/tonne (t) in the week ended 5 December, marking a $57/t or 2% gain w-o-w from the previous week. The week began with prices at $2,884/t, which then rose to around $2,888/t mid-week. Prices closed at $2,893/t on 05 December.

Meanwhile, LME aluminium inventories witnessed minor outflows, with stocks down by 1.7% at 533,280 t against 542,300 t in the previous week.

What impacted prices?

Aluminium prices gained as tightening supply conditions coincided with firming demand signals. Chinese smelters neared their government-mandated capacity ceilings, limiting prospects for additional output, while SHFE inventories dropped sharply, reinforcing the supply-tightness narrative.

Global production growth remained tepid, with October’s primary output up only 0.6% y-o-y reaching 6.29 mnt, and disruptions–from Iceland’s Grundartangi smelter issues to Alcoa’s Kwinana refinery closure and Century Aluminium’s cuts–further constrained availability. At the same time, demand indicators strengthened: China’s imports of unwrought aluminium and products continued to rise, supported by strong September and October inflows, and export volumes earlier in the year signalled solid global order books. This combination of restricted supply and improving consumption underpinned the price gains.

Outlook

Looking ahead, aluminium prices are likely to stay supported trading in a narrow range of $2,860-2,890/t as supply constraints persist and demand from China remains steady in the week beginning 8 December . While it is expected a mild surplus next year, market participants expect the sentiment to remain firm, with manufacturing and construction activity offering continued upside risk to prices.

Leave a Reply